Global| Mar 12 2008

Global| Mar 12 2008French Inflation Begins to Level Off in February

Summary

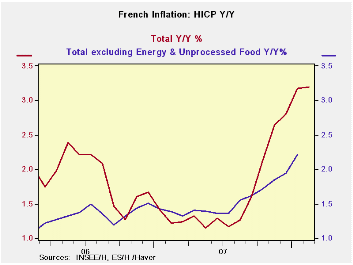

French headline inflation began to level off in February of 2008. The 12-month rate that rose to 3.2% in January from 2.8% in December held steady at that 3.2% pace in February. The ECB has a ceiling objective only for the inflation’s [...]

French headline inflation began to level off in February of 2008. The 12-month rate that rose to 3.2% in January from 2.8% in December held steady at that 3.2% pace in February. The ECB has a ceiling objective only for the inflation’s headline. At 3.2% France’s own pace is well above that 2% ceiling. Still it is something that year/year acceleration has stopped, for now. The core inflation reading is not available but the HICP core rate edged above the 2% mark last month.

As to the various inflation categories we can turn to France’s domestic inflation measure that has slightly different ingredients form the HICP. France’s overall inflation on that measure is up by 2.9% year/year the same as it was last month. The French domestic core inflation rate is at 2.1% in February up from 2% in January. Inflation overall, at 2.9%, is higher than it was 12 months ago (1.1%). Not surprisingly the diffusion condition based that result is high at 72.7%.

This diffusion reading is a US ISM type measure that counts all inflation accelerating categories in the CPI as a value of ‘one.’ If inflation is steady period to period it counts as 0.5. The category results are totaled and taken as a percentage of the total number of categories. Roughly this means that above 50% inflation is accelerating and below 50% inflation is decelerating. For the year ago comparison we find that inflation accelerated year/year in 72% of the categories. And that seems bad. But over six months, although the inflation rate was higher-still at a 3.6% pace, inflation diffusion was only 36%. Over three months inflation is at 3% and diffusion is at 27%. So inflation is not accelerating on a broader patch, but rather on a narrower one, if at all.

The overall inflation rate, while still high, has come down. You can see it in the core domestic French rate that is 2.1% year/year, 2.3% over 6 months and 1.9% over 3 months. Inflation is not getting out of hand in France despite the ugly headlines. Food costs are a problem, surging and steadily accelerating over the past year until those costs are up at an 8% pace over the most recent three months. In addition, energy prices have been rising and spot oil is still higher than it was in January and February on average.

Inflation is still a ‘threat’ but the detailed trends from France suggest that the ECB and the strong euro are helping to keep inflation from spreading. France has the fourth best record in EMU on keeping core inflation in check from 2000 to date. Finland has the best record, Germany the second best for that period. Greece has the worst record followed by Ireland and Spain.

| France HICP and CPI details | |||||||

|---|---|---|---|---|---|---|---|

| Mo/Mo % | Saar % | Yr/Yr | |||||

| Feb-08 | Jan-08 | Dec-07 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| HICP Total | 0.0% | 0.3% | 0.4% | 3.0% | 4.1% | 3.2% | 1.2% |

| Core | #N/A | 0.3% | 0.3% | #N/A | #N/A | #N/A | 1.4% |

| CPI | |||||||

| All | 0.0% | 0.4% | 0.3% | 3.0% | 3.6% | 2.9% | 1.1% |

| CPI ex Food & Energy | 0.1% | 0.2% | 0.2% | 1.9% | 2.3% | 2.1% | 1.2% |

| Food | 0.2% | 1.2% | 0.6% | 8.0% | 7.2% | 5.1% | 0.7% |

| Alcohol | 0.3% | 0.1% | 0.1% | 1.9% | 2.5% | 4.7% | 0.7% |

| Clothing & Shoes | -0.2% | -0.7% | 0.1% | -2.8% | -0.8% | 0.6% | 0.8% |

| Rent &Utilities | 0.2% | 0.5% | 0.6% | 4.9% | 6.7% | 4.6% | 3.3% |

| Health Care | 0.0% | 0.1% | -0.1% | 0.2% | 0.3% | 0.3% | 0.2% |

| Transport | 0.1% | 0.1% | 1.0% | 5.1% | 8.2% | 5.8% | 1.0% |

| Communication | -1.4% | -0.4% | -0.3% | -8.0% | -3.1% | -2.1% | -1.8% |

| Recreation & Culture | -0.2% | 0.0% | -0.3% | -2.1% | -1.7% | -1.3% | -2.0% |

| Education | 0.2% | 0.5% | 0.2% | 3.6% | 3.6% | 3.0% | 2.5% |

| Restaurant & Hotel | 0.2% | 0.4% | 0.3% | 3.3% | 0.8% | 2.8% | 2.5% |

| Other | 0.0% | 0.0% | 0.2% | 0.7% | 1.6% | 1.8% | 2.4% |

| Diffusion Type | 27.3% | 36.4% | 72.7% | ||||

| Compared to | 6-mo | 12-mo | Yr-Ago | ||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief