Global| Oct 28 2004

Global| Oct 28 2004French Industry Noticeably More Optimistic, Unlike Neighbors

Summary

Unlike other major European countries discussed here in the last few days, industry leaders in France are increasingly optimistic. The overall Business Climate Index, a composite of their assessment of trends in production and orders, [...]

Unlike other major European countries discussed here in the last few days, industry leaders in France are increasingly optimistic. The overall Business Climate Index, a composite of their assessment of trends in production and orders, reached 108 in October, its highest since March 2001. Similarly, expectations for the trend in production going forward had a positive/negative balance of +16 for October, the most favorable reading since February 2001.

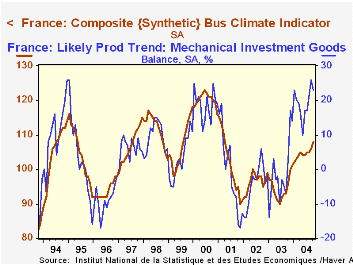

Several market segments are participating in the apparent business improvement. Markets for consumer goods have gained the most in the most recent months, as the percent balance indicator has jumped from -2 in July to +17 in October. However, this sector tends to be volatile, so such a pattern may not be sustained. Intermediate materials have moved less dramatically in the short-run, but generally experience smoother, longer-lasting swings. Currently, that segment's balance indicator stands at +16, unchanged in the month, but in a generally favorable position since the middle of last year. Mechanical business equipment actually eased a bit in October to +23 from September's +26, but it had improved more and stayed higher in previous months.

We find this good performance a bit perplexing. The two major macroeconomic forces today, the euro exchange rate and oil prices are international in scope, affecting every major economy. Possibly French industry is experiencing the evolution of a favorable push due to the flattening of the euro that began in March. One of the industries showing a pick-up is mineral products, suggesting that France may be able to benefit more than its neighbors from rising petroleum prices. These suggestions are just conjecture, however, and it remains to be seen how long this attractive business sentiment will be sustained.

| Seasonally Adjusted, % Balance (except as noted) | Oct 2004 | Sept 2004 | Aug 2004 | Oct 2003 |

2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|---|

| Business Climate Index | 108 | 106 | 105 | 96 | 95 | 97 | 102 |

| Likely Production Trend | 16 | 14 | 11 | 5 | 1 | 5 | 5 |

| Selected Type of Goods: | |||||||

| Consumer Goods | 17 | 6 | 2 | -6 | 1 | 5 | 13 |

| Intermediate Goods | 16 | 16 | 11 | 7 | -4 | 2 | -5 |

| Mechanical Investment Goods | 23 | 26 | 21 | 3 | -1 | -4 | -1 |

| Electronic Investment Goods | 5 | 2 | 10 | 0 | 5 | -9 | 4 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief