Global| Jun 26 2014

Global| Jun 26 2014French Household Confidence Picks Up but by Very Little

Summary

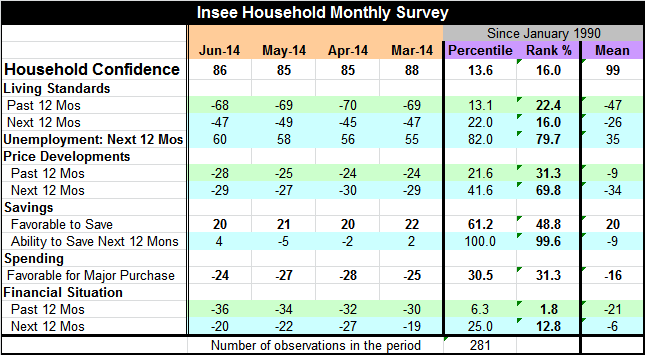

Household confidence in France improved to 86 in June from 85 in May. However, it is still below its level of 88 in March 2014. The index level sits in the lower 16th percentile of its historic queue of data. This tells us that it has [...]

Household confidence in France improved to 86 in June from 85 in May. However, it is still below its level of 88 in March 2014. The index level sits in the lower 16th percentile of its historic queue of data. This tells us that it has been weaker only 16% of the time and makes this an extremely weak readings, despite the small rise on the month.

Household confidence in France improved to 86 in June from 85 in May. However, it is still below its level of 88 in March 2014. The index level sits in the lower 16th percentile of its historic queue of data. This tells us that it has been weaker only 16% of the time and makes this an extremely weak readings, despite the small rise on the month.

France is one country in the euro area that has not been giving off contradictory signals. Its confidence is weak; its PMI values are weak; its GDP is weak; and the outlook for this year has just been weakened. France no longer expects to hit its previously established growth targets.

According to the survey, the French assessment of the living standards for the past 12 months is in the 22nd percentile of its historic rank, while the outlook for the next 12 months is in the 16th percentile of its historic queue. This means that things that have been very bad in the next 12 months are expected to get worse in the course of the next 12 months. The prospect for unemployment index rose to 60 in June, substantially higher than its 55 level back in March 2014. It sits in its 79th percentile, marking unemployment as a real possibility in the minds of those who respond to the survey.

Despite the weakness in these indicators, price developments for the past 12 months and the next 12 months are much higher than one might expect. For the past 12 months price developments are assessed as in the 31st percentile of their historic queue while the reading for the next 12 months is in the 69th percentile. Thus, despite the weakness in the economy and the perceived risk of unemployment, price pressures are seen as growing in the next 12 months.

The spending environment improved to a level of -24 in June from -27 in May. The percentile rank of that reading is in the lower one third of its historic queue. That's a weak reading in absolute terms, but a reading that appears `strong' compared to the rest of the readings in the survey.

The financial situation in the past 12 months deteriorated to an index level of -36 from -34. This reading marks a bottom 1.8 percentile standing in its historic queue. This means that the French respondents think that the financial situation in the last 12 months was worse less than 2% of the time. Looking to the next 12 months, the assessment actually improves slightly to -20 from -22; that value is a standing in a 12.8 percentile of its historic queue. That means a financial situation is expected to get better in the next 12 months than it was in the last 12 months, but it is still expected to be extremely bad as it is only worse about 12% of the time.

The survey by Insee of various French households reveals a very frustrated and concerned consumer. The current confidence levels are extremely low. The fear of unemployment is high. The environment for spending is still poor. In the financial situation which has been terrible is expected to stay pretty bad in the future. At the same time, the French authorities have cut their outlook for growth and France's policy, as currently set, is barely keeping to the standards of debt-to-GDP it has agreed-upon. What that means is that there's no further wiggle room for policy in France to be more stimulative and still meeting its euro area requirements. France is literally between a rock and a hard place with its economy in a very soft place.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief