Global| Feb 24 2016

Global| Feb 24 2016French Household Confidence Backs Off After a Run of Gains, Currently at a Six-Month Low

Summary

The INSEE household confidence indicator for France fell to 95 in February from 97 in January. The index was last lower six months ago. The index had recouped a lot of its losses by May 2015. The current set back takes it to the [...]

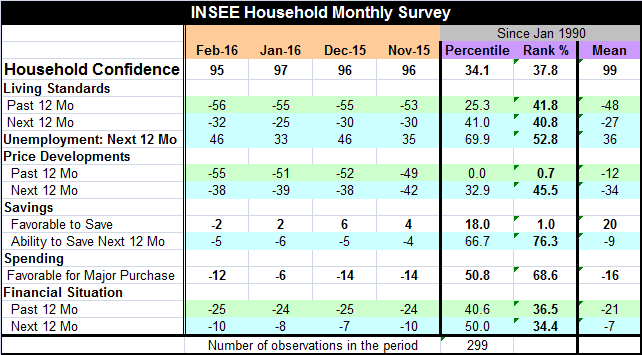

The INSEE household confidence indicator for France fell to 95 in February from 97 in January. The index was last lower six months ago. The index had recouped a lot of its losses by May 2015. The current set back takes it to the lowest portion of its six-month range, still on a higher plateau compared to earlier in the expansion. But at the current level, the index still sits only in the 37th percentile of its historic queue of data, well below the midpoint (which resides at a rank value of 50). The perch on which it sits is precarious and not very strong in historic profile.

The INSEE household confidence indicator for France fell to 95 in February from 97 in January. The index was last lower six months ago. The index had recouped a lot of its losses by May 2015. The current set back takes it to the lowest portion of its six-month range, still on a higher plateau compared to earlier in the expansion. But at the current level, the index still sits only in the 37th percentile of its historic queue of data, well below the midpoint (which resides at a rank value of 50). The perch on which it sits is precarious and not very strong in historic profile.

French assessments of living standards and unemployment expectations were casualties on the month and all have deteriorated. Past living standards fell by one point; the assessment of the future fell sharply to -32 from -25, while unemployment expectations jumped to 46 from 33. The month-to-month unemployment jump has only been greater 8% of the time historically. The living standard gauges both past and future have standings near their respective 41st percentiles while unemployment expectations stand above their median at their 52nd percentile. We are moving into an era where people are having above average fears of unemployment and where their living standards are eroding and their financial situations are thought to be shaky. This will not continue to support anything but anemic spending.

Prices saw expectations improve slightly and saw some deterioration in past trends. Still, past trends are extraordinarily poor, weaker only 0.7% of the time- almost never weaker. And expectations are weaker only 45% of the time, even at this poor price level, as the topical reading is below its historic median.

The response to the query is it `favorable to make a purchase' fell by six points from -6 to -12 to post a 68th percentile reading. This is still one of the most positive responses in the whole survey but make no mistake about it, it is slipping and its underpinning is being undermined.

Meanwhile, the assessment by respondents about their financial situation eroded for past and future assessments with the past standing ranking in its 36th percentile and its expected standing for the next 12 months at its 34th percentile. Both of them are near the one one-third position of their historic queue of data and that is not a very favorable level.

On balance, there is still a lot of slippage in this report, but not much in the way of severe slippage. There is substantial giveback for expected living standards, a considerable drop off in the assessment of the `favorable to make a major purchase' indicator as well as a strong step up for expected unemployment. But most worrisome is that the household confidence indicator shows some sign of falling off this plateau of readings it has been on for six months and a bit longer. At this level, it already is substandard. Any further drop could indicate more serious backtracking for the consumer that could more significantly undermine the economy.

Germany already has been posting weaker readings on its ZEW and IFO surveys. Today, Italy reported a drop-off in industrial orders based mostly on flagging domestic order strength. But over the past year, it is Italian domestic orders that are advancing and foreign orders that are falling. Trends may be shifting here, but there is little evidence that they are shifting for the better. In the U.K., a retail survey was weaker. Evidence from around the EMU and the world continues to show a great deal of weakness and further backtracking. Singapore did report a 6.2% growth rate in Q4, but that was only marginally higher than Q3. Taiwan reported sharply weaker export orders and Hong Kong is cutting some taxes to try to gain some stimulus. Small business confidence improved slightly in Japan in February. There are some improvements out there, but they are too few and too far between and on variables or in places that are just not significant enough to be reassuring. And then there are the reports of outright weakness that seem to be on the reports that we weigh and value most.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief