Global| Jan 27 2010

Global| Jan 27 2010French Biz And Household Sectors Continue Process Of Repair

Summary

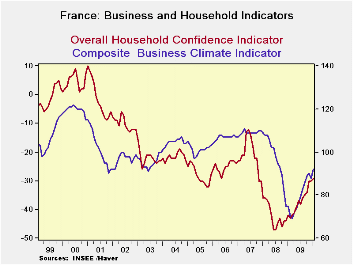

Despite great strides made in the improvement in business and household confidence since the pit of the recession, levels of confidence for business and households remain at levels that are below par. Both series, while still [...]

Despite great strides made in the improvement in business and household confidence since the pit of the recession, levels of confidence for business and households remain at levels that are below par. Both series, while still climbing, are showing signs of slowing the pace of that advance.

The industry climate reading stands in the 43rd percentile of its range well below the mid point and at an index of 92 it stands well below the mean value of 100 as well. The only reading that stands above its mean is the RECENT trend for production. Unfortunately the likely trend is at the 47th percentile of its range, below the midpoint and at a reading of -7 it is below its mean reading of +5. The orders trends are improving but they have a very long way to go just to get back to neutral.

The story for the household sector is much the same as for business, except weaker. At -29 the confidence reading for households is below neutral and in fact is much weaker than that standing short of the one-third mark of its range. The mean reading stands at -19 but confidence reads -29 in January.

While the strongest reading from the consumer is a positive reading on the household’s current financial standing (a reading in the 81st percentile of its range) the next highest reading is a 77th percentile reading on the prospect for unemployment. These two readings are diametrically opposed. French consumers fear unemployment yet see that they are in a relatively strong current financial situation, even as the economy is putting its worst days behind it. This is surely a prescription for the consumer to keep his wallet locked up tightly.

Responses show that living standards are thought to have improved and to be improving. Yet these readings are low in their respective ranges and well short of historic median values.

Savings is one of the bright spots. While standing in the 59th and 65th percentiles both the responses for ‘favorable to save’ and ‘ability to save’ are near or above historic median values.

Spending, a key parameter for getting recovery in gear is still rated as subpar. Households’ response to the question ‘is it a favorable time to spend?’ resides just short of the 40th range percentile and at a raw reading of -19 that is short of its median value of -14.

In short the business sector and the consumer sector see ongoing progress

| INSEE Industry Survey | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Since Jan 1990 | Since Jan 1990 | |||||||||

| Jan 10 |

Dec 09 |

Nov 09 |

Oct 09 |

Percentile | Rank | Max | Min | Range | Mean | |

| Climate | 92 | 88 | 90 | 89 | 43.4 | 186 | 122 | 69 | 53 | 100 |

| Production | ||||||||||

| Recent Trend | -4 | -10 | -8 | -8 | 59.3 | 111 | 44 | -74 | 118 | -8 |

| Likely trend | -7 | -5 | -1 | -1 | 47.1 | 211 | 30 | -40 | 70 | 5 |

| Orders/Demand | ||||||||||

| Orders&Demand | -45 | -52 | -52 | -52 | 22.2 | 215 | 25 | -65 | 90 | -17 |

| Fgn Orders&Demand | -45 | -54 | -46 | -49 | 25.5 | 215 | 31 | -71 | 102 | -13 |

| Prices | ||||||||||

| Likely Sales Price Trend | -11 | -18 | -13 | -9 | 25.5 | 205 | 24 | -23 | 47 | 0 |

The consumer is still not solidly underpinned by the notion that government has stabilized the economic environment. Even though consumers are feeling relatively financially settled they are fearful of the future and therefore are not very prone to spend. Spending proclivity is lagging behind improvements in financial well being. This is an issue for policymakers. It is not necessarily a call out for any new program but for leadership to take steps to reassure an economically frightened public that is better off than it suspects and whose fear could become a catalyst for backsliding.

As for business its progress is steady and there is no concern about inflation. But even as current conditions have improved, here again we see reluctance to extrapolate ongoing improvement into the future. The orders data manifest this result with still weak (although improving) readings for orders and demand that seem to get a greater weight than their improving trend. What is lacking in France is confidence and more certainty about the future.

That predicament may also be a statement about the e-Zone in which France is firmly embedded. The whole of the e-zone is still struggling with several states still battling horrific issues. In this environment the euro, the strap that binds Europe together may be more of a corset that restrains optimism since the healthy countries are more afraid of being pulled down by or made to assist those that are struggling. Europe seems to have been able to cobble together an economic structure that has doe it more harm than good. The area is bound together by a common currency that protects the imprudent from the consequences of their own actions. Fiscal transgression is not easily exported since fiscal accounts are kept separate. There is no sharing of the public expenditure pot in Europe except for certain consolidated government funding. Still there is a stigma. And you may recall how the Latin American Debt crisis brought down all of Latin America despite there being no common currency and no shared fiscal responsibility of any type – just proximity and shared culture. Europe is walking a very shaking tightrope and has not figured out yet how to remedy its problems. France is but an example.

| INSEE Household Monthly Survey | |||||||

|---|---|---|---|---|---|---|---|

| Since Jan 1990 | |||||||

| Jan 10 |

Dec 09 |

Nov 09 |

Oct 09 |

Percentile | Rank % | Mean | |

| Household Confidence | -29 | -30 | -30 | -34 | 31.6 | 21.6 | -19 |

| Living Standards | |||||||

| past 12 Mos | -62 | -65 | -65 | -70 | 18.4 | 16.2 | -40 |

| Next 12-Mos | -34 | -36 | -35 | -39 | 33.3 | 24.9 | -21 |

| Unemployment: Next 12 | 64 | 62 | 63 | 65 | 77.7 | 88.4 | 33 |

| Price Developments | |||||||

| Past 12Mo | -22 | -25 | -27 | -28 | 28.9 | 55.2 | -16 |

| Next 12-Mos | -37 | -42 | -46 | -45 | 24.7 | 53.1 | -35 |

| Savings | |||||||

| Favorable to save | 21 | 12 | 13 | 8 | 59.1 | 46.1 | 22 |

| Ability to save Next 12 | -4 | -6 | -7 | -11 | 65.5 | 83.8 | -9 |

| Spending | |||||||

| Favorable for major purchase | -19 | -20 | -19 | -24 | 39.7 | 40.2 | -14 |

| Financial Situation | |||||||

| Current | 20 | 18 | 17 | 13 | 81.0 | 97.5 | 12 |

| Past 12 MOs | -21 | -21 | -22 | -25 | 48.4 | 29.0 | -17 |

| Next 12-Mos | -10 | -10 | -8 | -12 | 40.0 | 15.8 | -2 |

| Number of observations in the period = 241 | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief