Global| Nov 10 2015

Global| Nov 10 2015French and Italian IP Show Fledgling Recovery

Summary

France and Italy are the second and third largest economies, respectively, in the EMU. Their recent trends in industrial output make a good summary of what is going on in the EMU as a whole. Neither is particularly strong and yet both [...]

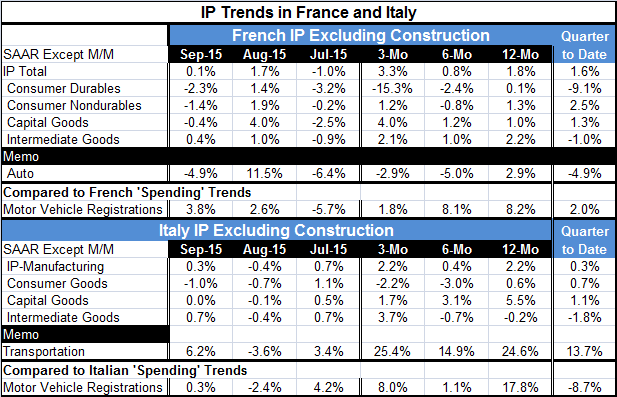

France and Italy are the second and third largest economies, respectively, in the EMU. Their recent trends in industrial output make a good summary of what is going on in the EMU as a whole. Neither is particularly strong and yet both are managing increases in output. Both Italy and France have two IP increases in the last two months; for France there are two increases in a row. Both show an IP increase in September and both show an IP increase of about 2% year-over-year (1.8% for France and 2.2% for Italy). Both show some recent weakness in IP growth in their respective consumer sectors.

France and Italy are the second and third largest economies, respectively, in the EMU. Their recent trends in industrial output make a good summary of what is going on in the EMU as a whole. Neither is particularly strong and yet both are managing increases in output. Both Italy and France have two IP increases in the last two months; for France there are two increases in a row. Both show an IP increase in September and both show an IP increase of about 2% year-over-year (1.8% for France and 2.2% for Italy). Both show some recent weakness in IP growth in their respective consumer sectors.

The way that each of them get to these metrics is still quite different, however.

In Italy, consumer goods output is falling in September and is falling at a -2.2% annual rate over three months. Intermediate goods output is up strongly over three months (3.7% pace) and capital goods output is up at a mild 1.7% pace. On trend consumer goods output is decaying along with capital goods output trends, but intermediate goods output is accelerating. Transportation equipment output is very strong and steady.

For France, output for consumer goods durables and nondurables is falling in September, like in Italy. Over three months consumer durables output is falling fast. But capital goods output is strong, up at a 4% pace over three months and is steadily accelerating - the opposite trend from Italy's. Intermediate goods output is up at a 2.1% pace over three months and its trend is steady. France's motor vehicle output, while weakening over three months, had been firm over six months and 12 months.

In the quarter to date, both French and Italian output is increasing. France has a sharp decline in consumer goods output in the quarter while in Italy consumer goods output is up slightly. Both show a mild increase in capital goods output in Q3. Both show a mild drop in intermediate goods output in Q3. In France, auto output is falling in Q3 as vehicle registrations by the public were up at just a 2% pace. In Italy, transportation goods output is up at a robust 13.7% pace in Q3 despite a decline in motor vehicle registrations at a -8.7% pace in Q3.

Each country shows some strength and some weakness, but overall output and its trends are mild with too many negative growth rates to be very reassuring.

New Risks?

The new trend to watch in town is probably the election in Portugal. While Greece has been in the news for not making the necessary changes to warrant the next tranche of funds from the EU, Portugal is about to make a political shift that could make the problems in Greece look small. Left wing anti-austerity parties are set to oust the sitting minority center-right government. There is a parliamentary vote scheduled. If a Socialist-led government is formed, the leftists have declared that they will put an end to the policies of austerity. That is something to watch in the EMU. It could have broad repercussions for growth and stability in the union. It is potentially more of a risk that David Cameron's saber rattling over the changes he seeks to keep the U.K. in the EMU grid. Cameron can be negotiated with. It is not clear that is the case with a new Portuguese government.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief