Global| Feb 19 2015

Global| Feb 19 2015Forget April, Deflation in Paris, Chaos in Greece; Deflation Runs the Table on Early EMU HICP Reporters

Summary

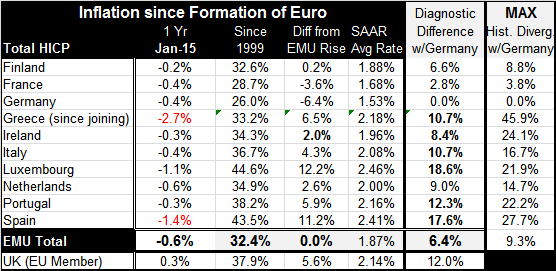

Inflation is gone. Deflation has come. It's no Saturday Night Live `land shark' skit and it's too late to just not open the door. Year over year prices are lower by 2.7% in Greece and by 1.4% in Spain: these are real drops. Finland [...]

Inflation is gone. Deflation has come. It's no Saturday Night Live `land shark' skit and it's too late to just not open the door. Year over year prices are lower by 2.7% in Greece and by 1.4% in Spain: these are real drops. Finland reports a bare-bones 0.2% drop with relatively small drops of 0.3% in Ireland and Portugal. But prices are falling everywhere. It's raining deflation or, put another way, deflation reigns.

Inflation is gone. Deflation has come. It's no Saturday Night Live `land shark' skit and it's too late to just not open the door. Year over year prices are lower by 2.7% in Greece and by 1.4% in Spain: these are real drops. Finland reports a bare-bones 0.2% drop with relatively small drops of 0.3% in Ireland and Portugal. But prices are falling everywhere. It's raining deflation or, put another way, deflation reigns.

When we look at history, only two countries have prices rising by less than the EMU weighted average from the start: those are France and Germany. France just reported its inflation today. Despite other problems with competitiveness, a 35-hour work week, and with fiscal control, France has been able to keep its HICP in line more or less with Germany. The French have been the best of all EMU members in not letting Germany's prices put them behind the eight ball. Of the ten countries in the table, (nine excluding Germany) five still have a price divergence with German of 10 percentage points or more. A plunging price level and a ravaged economy have brought Greece to 10 percentage points of Germany from a maximum divergence of 45 percentage points at its worst. Greece is now tied with Italy as far as its divergence with Germany is concerned. The most divergent countries now are Luxembourg (a financial center) at 18.6% and Spain at 17.6%. Of course, what this table really underscores is how divergent Germany has been, but then Germany is the reason that the ECB has been able to hit its inflation objective consistently.

Even factoring in this period of price sluggishness and deflation, six countries in the table have averaged inflation of 2% or better during their membership in the EMU. That's above what is allowed for the region as a whole.

And this brings us to the sad case of Greece. Greece has put forth its plan for an extension of its existing adjustment program. While some news agencies call Greek concessions `considerable', it seems to me on close reading that the Greek concessions are at this point vague at best.

Another `Big Wink' with Greece?

Of course, Greece's new leaders must have something to bring home to justify their election promises. They need wiggle room. And the rest of the EMU knows that, and so should be vigilant on vagueness. The question is if Europe will tolerate another BIG WINK whereby Greece's deal is extended and it is portrayed as Greece continuing to toe the line, when in fact Greece will be allowed some considerable modification.

The Germans have been quick to speak and, as we have been projecting, they reject the Greek deal outright.

At the same time, the European Central Bank is preparing an emergency funding program for Greek banks. It looks like the back door is still open. The way is not shut.

This brings us to our principal and enduring argument that Germany will not tolerate any significant deviation from the existing Greek plan. What the Greek leaders get to `bring home' is bupkis - news of a grim reality out there. Our premise is that Germany has now witnessed how the rest of the EMU can gang up to force open the big EMU piggy-bank called the ECB and that has been done by QE. In this the German have lost a major safeguard that was of critical importance to it in forming the EMU. This has put Germany in an altogether different and truly inflexible state of mind.

Remember the ECB was to be modelled on the Bundesbank. It was even located in Frankfurt, Germany. There was only one pillar of monetary policy: the inflation objective. And now the ECB is open not just for LTRO business and other asset backed lending but for QE. And QE is sure to cost money. The Germans took the unusual step of insisting that QE be in the province of the local central banks, de-mutualizing risk, by not using the ECB balance sheet to protect it.

It should be plain to see what is happening. Germany is getting very concerned about the sanctity of the ECB and fact that it is under attack on abroad front NOT JUST BY GREECE. QE is an attempted raid on ECB resources. Germany is backing away from EMU and the ECB.

And Greece is a small country. If there is someplace where the Germans are to make a stand it must be here. A special deal for Greece will entice Italy, Spain and Portugal too. A hard line or a Grexit would force serious thought among other EMU members to say nothing of the political and market pressures that would develop. However, a union that survived that likely is one that might really survive. If the test is not here and now, then Europe is surely going to slip into more and more accommodation with its members.

Most simply assume Germany will be forced to rollover on this. I do not. The Germans cannot be forced to compromise and stay in the EMU. The EU Commission is already a lost cause of stewardship, having been coopted by member states and is unable to bring the hard line to fiscal excess when it arises. As we are seeing with Greece, when financial stress hits, the ECB is drawn further into the lending web as it has again with emergency lending to Greek banks. All excesses lead to `a run' on ECB resources. Enough!

Greece, after all its price level progress, has done it all too fast and too painfully. As close as it is to getting its price competiveness in line, it has done so at a horrific cost to social stability. This is something the Germans could never foresee and still seem to be oblivious to. But it's real. There is no doubt that Germany is the reason that this is all happening. It has a misunderstanding that finance everywhere should work and does work as it has in Germany. It is very conservative with fiscal and monetary policy. It is also inflexible as the iron fist ensures progress. And the German people share these values. But outside Germany the rules are different. The expectations are different. The social compact is different. People's expectations and demands of government are different. And so in the end maybe Greece is just too different to survive in the EMU?

The message from Germany seems clear enough. It is this: NO! We gave you a bailout and you gave us a plan. Now stick to your word. Greece wants a rest because the pain has been so great. But Germany sees a deal as a deal and is very interested in sending this message across the euroland. It needs to make it clear that the ECB will be defended and that countries need to adopt fiscally more sound policies instead of expecting a monetary policy bailout when the going gets tough. The euro-piggy bank needs to be off the table. So this is a test case of German strength. It is why I think Grexit is on the table for real. Germany would far rather see Greece out on its ear than in on a cushy deal that will keeps hopes of financial deviancy alive in Greece a well as elsewhere. Germany wants NO PART of a deal that will result in Greek celebrations in the street and more effigies of German politicians or historic figures burned in public. They are welcome to do that when they leave, however. This is where the Bundesbank fights its battle to protect the integrity of the ECB. I think the battle is fully engaged and that Greece is hanging by a thread and all but bound and gagged by its own internationally naive election tricks. Greece sought to force Europe's hand. Instead, it has exposed its isolation and is forcing its own confrontation with reality. Greece has no leverage anymore. It can leave. That way is not shut either.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief