Global| Aug 12 2009

Global| Aug 12 2009FOMC Leaves Rates Unchanged; Notes Financial Market Improvement & Retail Spending Stabilization

by:Tom Moeller

|in:Economy in Brief

Summary

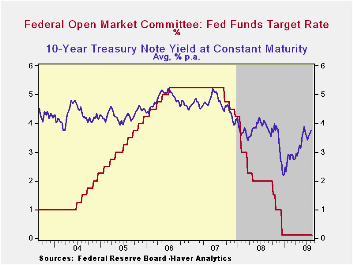

In an anticipated and unanimous vote, the Federal Open Market Committee today left the Federal funds rate in a "range from 0 to 1/4 percent." The discount rate also was left unchanged at 0.5%. The Fed funds rate remained the lowest [...]

In an anticipated and unanimous vote, the Federal Open Market Committee today left the Federal funds rate in a "range from 0 to 1/4 percent." The discount rate also was left unchanged at 0.5%. The Fed funds rate remained the lowest ever.

The Fed indicated that "Conditions in financial markets have improved further in recent weeks. Household spending has continued to show signs of stabilizing but remains constrained by ongoing job losses, sluggish income growth, lower housing wealth, and tight credit.

Again, much of the commentary on the economy was similar to the last two meetings and concluded that "Although economic activity is likely to remain weak for a time, the Committee continues to anticipate that policy actions to stabilize financial markets and institutions, fiscal and monetary stimulus, and market forces will contribute to a gradual resumption of sustainable economic growth in a context of price stability."

Regarding inflation the FOMC statement acknowledged the rise in energy & other commodity prices, but concluded that substantial economic slack will leave inflation "subdued for some time."

In its effort to promote economic liquidity, the Fed used

similar language as in June, "... to provide support to mortgage

lending and housing markets and to improve overall conditions in

private credit markets, the Federal Reserve will purchase a total of up

to $1.25 trillion of agency mortgage-backed securities and up to $200

billion of agency debt by the end of the year. In addition, the Federal

Reserve will buy up to $300 billion of Treasury securities."

New was the indication that "the Committee has decided to gradually slow the pace of these transactions and anticipates that the full amount will be purchased by the end of October."

For the complete text of the Fed's latest press release please follow this link.

The Haver databases USECON, WEEKLY and DAILY contain the figures from the Federal Reserve Board.

The Shadow Banking System: Implications for Financial Regulation from the Federal Reserve Bank of New York can be found here.

What Do We Know (And Not Know) About Potential Output? from the Federal Reserve Bank of St. Louis is available here.

| Current | Last | December | 2008 | 2007 | 2006 | |

|---|---|---|---|---|---|---|

| Federal Funds Rate, % (Target) | 0.00 - 0.25 | 0.00 - 0.25 | 0.16 | 1.93 | 5.02 | 4.96 |

| Discount Rate, % | 0.50 | 0.50 | 0.50 | 2.39 | 5.86 | 5.96 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief