Global| Dec 11 2007

Global| Dec 11 2007Federal Funds Rate Lowered to 4.25%

by:Tom Moeller

|in:Economy in Brief

Summary

In a widely expected move, the target interest rate for Federal funds was lowered twenty five basis points to 4.25% at today's meeting of the Federal Open Market Committee. Voting against the decision was Eric S. Rosengren who [...]

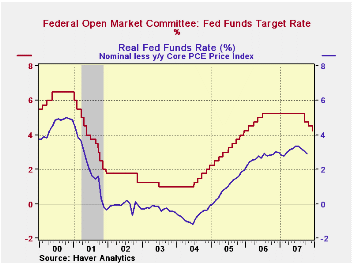

In a widely expected move, the target interest rate for Federal funds was lowered twenty five basis points to 4.25% at today's meeting of the Federal Open Market Committee.

Voting against the decision was Eric S. Rosengren who preferred a 50 basis point cut.

The discount rate also was reduced twenty five basis points to 4.75%.

The Fed's rationale for today's move was that recent data indicated a slowing in the rate of expansion due to "intensification of the housing correction and some softening in business and consumer spending." Moreover, strains on financial markets were viewed to have increased.

Regarding price inflation, the FOMC judged "that some inflation risks remain, and it will continue to monitor inflation developments carefully."

For the complete text of the Fed's latest press release please follow this link.

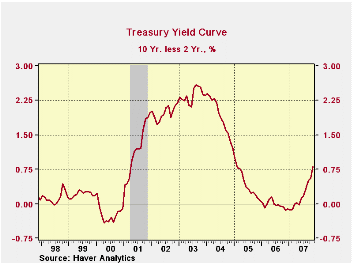

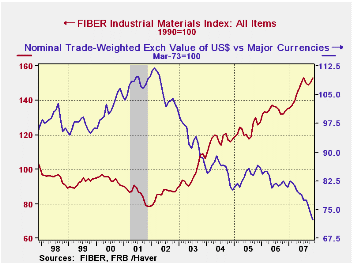

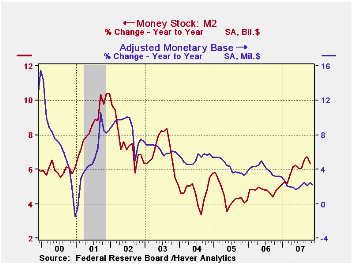

Other indicators of the current stance of U.S. monetary policy portray one of general ease. -- Easy - The yield curve already has steepened due to the decline in short term interest rates. This liquidity measure is not, however, near the most liquid of stances possible. -- Easy - The dollar's foreign exchange value is signaling an easy posture, down by roughly one-third since its 2002 high. -- Easy - Commodity prices are another signal of ease, nearly doubling since a 2002 low. -- Mixed - A mixed message is coming from the money supply measures. Growth in M2 has accelerated to a not too fast 6.3% rate of growth while growth in the monetary base has drifted lower to 2.2%. -- Tight - While down, the level of the "real" Fed funds rate still is high.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief