Global| Sep 20 2005

Global| Sep 20 2005Fed Funds Rate Increased to 3.75%

by:Tom Moeller

|in:Economy in Brief

Summary

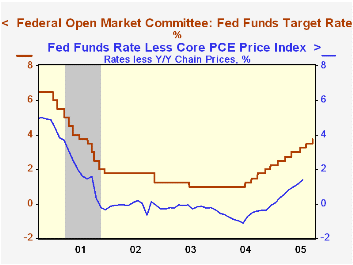

The Federal Open Market Committee increased the target rate for federal funds 25 basis points to 3.75%. The discount rate also was raised 25 basis points to 4.75%. This latest increase is the eleventh since June of 2004. The action [...]

The Federal Open Market Committee increased the target rate for federal funds 25 basis points to 3.75%. The discount rate also was raised 25 basis points to 4.75%. This latest increase is the eleventh since June of 2004.

The action was generally expected, though some analysts suggested the Fed would opt for no change in rates given the economic uncertainties generated by Hurricane Katrina.

Voting against the otherwise unanimous decision was Mark W. Olson, who preferred no change in rates at this meeting.

Today's press release from the Fed indicated that "While these unfortunate developments have increased uncertainty about near-term economic performance, it is the Committee's view that they do not pose a more persistent threat."

Indicating its concern about price inflation, the FOMC statement indicated "Higher energy and other costs have the potential to add to inflation pressures. However, core inflation has been relatively low in recent months and longer-term inflation expectations remain contained."

For the complete text of the Fed's latest press release please click here.

Has Monetary Policy Been More Accommodative Than Previously Believed? from the Federal Reserve Bank of St. Louis is available here.

Targeting versus Instrument Rules for Monetary Policy from the Federal Reserve Bank of St. Louis can be found here.

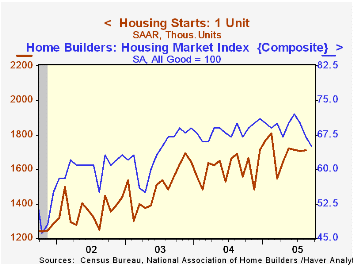

Housing Starts Slipped in Augustby Tom Moeller September 20, 2005

Housing starts slipped 1.3% last month to 2.009M units versus a downwardly revised 2.035M units in July.The drop outpaced Consensus expectations for a decline to 2.025M starts.

Single-family starts inched 0.1% higher in this last report taken before Hurricane Katrina hit the US Gulf Coast. The rise was due to higher single family starts in the Northeast (1.5% y/y) and in the West (6.1% y/y). Single family starts in the South fell m/m (+1.4% y/y) and in the Midwest (-6.5% y/y).

Yesterday's report from the Nat'l Association of Home Builders (NAHB) indicated slippage in their composite September index (-3.0% y/y) due to weaker current sales, weaker sales prospects and sharply lower buyer traffic. During the last twenty years there has been a 76% correlation between the y/y change in the NAHB index and the change in single family housing starts.

Multi family starts fell a sharp 8.5% m/m while building permits fell as well.

Assessing High House Prices: Bubbles, Fundamentals, and Misconceptions from the Federal Reserve Bank of New York can be found here.

| Housing Starts (000s, AR) | Aug | July | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Total | 2,009 | 2,035 | -0.8% | 1,950 | 1,854 | 1,7 10 |

| Single-family | 1,709 | 1,707 | 1.2% | 1,604 | 1,505 | 1,363 |

| Multi-family | 300 | 328 | -10.7% | 345 | 349 | 347 |

| Building Permits | 2,124 | 2,171 | 3.2% | 2,058 | 1,8 88 | 1,749 |

by Tom Moeller September 20, 2005

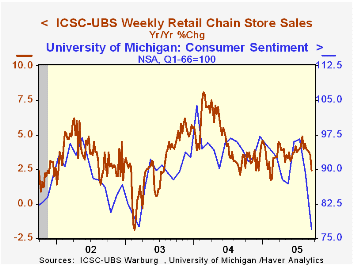

The full effect of Hurricane Katrina pushed chain store sales down 2.1% last week, according to the International Council of Shopping Centers (ICSC)-UBS survey, after a slight 0.2% decline the prior week. So far this month sales are 1.2% below the August average which fell 0.1% from July.

The ICSC suggested that in addition to the Hurricane, higher gasoline prices and a drop in consumer confidence were responsible for the decline.

During the last ten years there has been a 56% correlation between the y/y change in chain store sales and the change in non-auto retail sales less gasoline, as published by the US Census Department. Chain store sales correspond directly with roughly 14% of non-auto retail sales less gasoline. The leading indicator of chain store sales from ICSC cratered 2.0% in the latest week (-2.0% y/y) after a slight gain during the previous week.The ICSC-UBS retail chain-store sales index is constructed using the same-store sales (stores open for one year) reported by 78 stores of seven retailers: Dayton Hudson, Federated, Kmart, May, J.C. Penney, Sears and Wal-Mart.

| ICSC-UBS (SA, 1977=100) | 09/17/05 | 09/10/05 | Y/Y | 2004 | 2003 |

|---|---|---|---|---|---|

| Total Weekly Chain Store Sales | 445.0 | 454.6 | 2.4% | 4.6% | 2.9% |

by Tom Moeller September 20, 2005

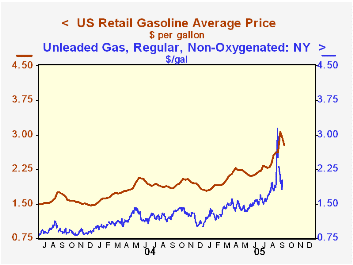

Supply uncertainties have wreaked havoc on prices for crude oil and petroleum products. As of last week, the US average retail gasoline price fell to $2.79 per gallon, down from the weekly high of $3.07 set two weeks earlier and the NY harbor spot price for regular unleaded last Friday was down to $1.82 from a high of $3.13 just before Labor Day.

Demand strength, however, has left even these lower gasoline prices both up 40-50% versus the year ago levels.

Hurricane Katrina caused the initial anxiety over supply. Figures from the Oil & Gas Journal Weekly indicate that in the first two weeks of September, US refining production of gasoline was off 5% versus August. Some of that decline is seasonal, but the threat from Hurricane Rita yesterday caused the spot gasoline price to jump 10% d/d to $2.00 per gallon.

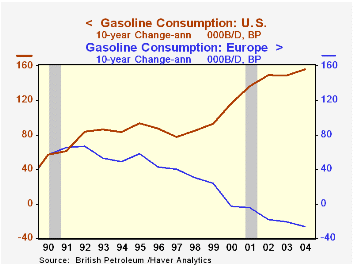

Alternatively, US gasoline demand has been consistent and strong. Through August demand was running 3-4% ahead of last year helped by a 1.5% y/y gain in the number of miles being driven. In September, demand is estimated to have fallen sharply, perhaps 10% m/m, in the wake of Hurricane Katrina, although the decline probably is temporary. Strong gasoline demand is a trademark of the United States. From 1994 to 2004, growth in US gasoline demand averaged 1.8% per year versus a 0.7% annual rate of decline in Europe during that ten year period. Some of that reflects differing economic fortunes, but ...

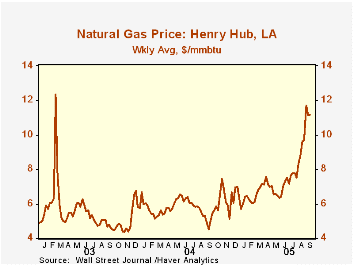

Wholesale natural gas prices at $11.17/mmbtu last week were more than double the prior year's level and very much reflect the recent supply dislocations. Regulation, however, has limited the price increase for residential gas as measured by the Consumer Price Index. For the first eight months of 2005 versus 2004, gas prices rose 11.5% while the gain in household electricity costs also was limited to 4.6%. Further gains are in store if yesterday's gas price rise over $12/mmbtu holds. (Many plants which generate electricity are fired by natural gas.)

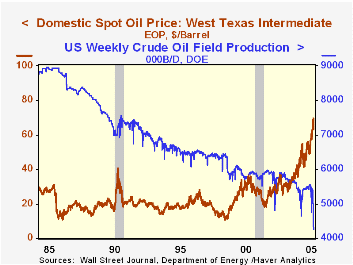

Movement in crude oil prices has been similarly volatile with an upward bent. Yesterday's spot market price for West Texas Intermediate jumped 7% d/d to $67.40 though prices have eased a bit today. Under laying the strength has been a steady decline in US crude oil production, off 2.2% y/y through the first eight months of 2005 and off 38% versus twenty years ago.

For the latest Short Term Energy Outlook from the US Department of Energy click here.

Oil Prices and Consumer Spending from the Federal Reserve Bank of Richmond can be viewed here.

| Energy Prices | 09/19/05 | 12/31/04 | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| US Retail Gasoline, Regular ($/Gal.) | $2.79 | $1.79 | 49.3% | $1.85 | $1.56 | $1.35 |

| Natural Gas, Henry Hub, LA ($/mmbtu) | $11.17 | $6.35 | 123.4% | $5.89 | $5.47 | $3.35 |

| Domestic Spot Market Price: West Texas Intermediate ($/Barrel) | $63.12 | $41.78 | 42.2% | $41.78 | $32.78 | $31.23 |

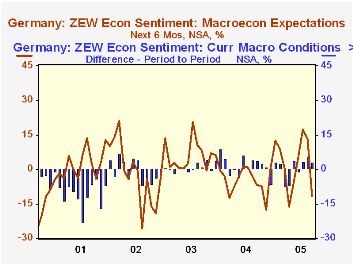

by Louise Curley September 20, 2005

Political considerations apparently weighed heavily on the economic expectations of German institutional investors and analysts in September. The Frankfurt based, Center for European Research (ZEW) reported that the number of those expecting better conditions six months from now over those expecting worse conditions fell from 50% in August to 38.6% in September. Although most of the 309 respondents to the survey reported before the election took place, the 44 replies that were received after the September 18 election showed a significantly lower reading than the overall September results.

Preliminary results of the September 18 election indicate that the CDU/CSU, (The Christian Democratic Union and The Christian Social Union) won 225 seats; the SPD (Social Democratic Party), 222; the FDP (The Free Democratic Party), 61; the Left Party, 54 and the Greens, 51. The Left Party, formerly known as Party for Democratic Socialism consists largely of former communists and former SPD members who disagreed with the party's plans for reform. The inconclusive results of the election will have to be resolved by some sort of a coalition or, if that fails before October 18 when Parliament is set to open, by another election. Political uncertainty is likely to continue to cast a cloud over the economic outlook.

Important as the effects of political uncertainty on confidence may be, the rise in energy prices resulting from hurricane Katrina has also had a depressing effect. In spite of the deterioration in expectations, investors reported a slight improvement in what they judged to be, according to the negative figures, depressing current conditions. In September, there was a three percentage point improvement in the appraisal of current conditions as the excess of pessimists over optimists (noted by a negative) went to -58.1% from -61.1% in August.

The attached chart shows the month-to-month changes in the German investors' appraisal of current conditions and their expectation of conditions six months from now.

| Zew Indicators | Sep 05 | Aug 05 | Sep 04 | M/M DIF | Y/Y DIF | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|---|---|

| Current conditions | -58.1 | -61.1 | -61.5 | 3.0 | 3.4 | -67.7 | -92.6 | -83.3 |

| Expectations 6 mo. ahead | 38.6 | 50.0 | 38.4 | -11.4 | 0.2 | 44.6 | 38.4 | 45.3 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief