Global| Aug 09 2005

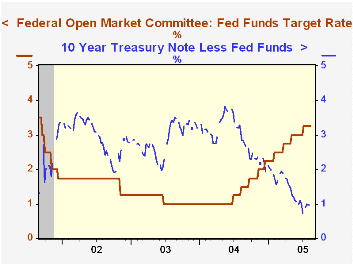

Global| Aug 09 2005Fed Funds Rate Increased to 3.50%

by:Tom Moeller

|in:Economy in Brief

Summary

The Federal Open Market Committee increased the target rate for federal funds an expected 25 basis points to 3.50%. The discount rate also was raised 25 basis points to 4.50%. This latest increase is the tenth since last June. The [...]

The Federal Open Market Committee increased the target rate for federal funds an expected 25 basis points to 3.50%. The discount rate also was raised 25 basis points to 4.50%. This latest increase is the tenth since last June.

The decision was unanimous.

Today's press release from the Fed continued to contain a comment suggesting that rates could be raised again. "The Committee believes that, even after this action, the stance of monetary policy remains accommodative ..."

The statement added that "Aggregate spending, despite high energy prices, appears to have strengthened since late winter, and labor market conditions continue to improve gradually."

Constantly vigilant, the Committee succinctly stated that "... pressures on inflation have stayed elevated."

For the complete text of the Fed's latest press release please click here.

Trends in Federal Funds Rate Volatility from the Federal Reserve Bank of New York is available here.

Additional Slack in the Economy: The Poor Recovery in Labor Force Participation During This Business Cycle from the Federal Reserve Bank of Boston can be found here.

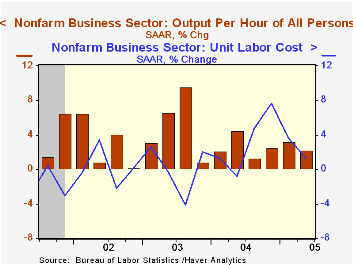

2Q U.S. Productivity As-Expected, Revisions Downby Tom Moeller August 9, 2005

Non-farm labor productivity increased 2.2% last quarter and about matched Consensus expectations for a 2.0% rise. Downward revisions to output growth from 2002 to 2004 (mostly due to upwardly revised estimates of inflation) lowered average growth in productivity during the period to 3.7% from 4.2%.

Unit labor costs slowed in 2Q to 1.3% from a 3.6% rate of growth in 1Q. The average rate of growth during the prior three years was revised up to 0.3% from -0.2%. Compensation costs decelerated to 3.5% from 6.9% growth in 1Q and the average during the prior three years was unchanged at a 4.0% rate of growth.

In the factory sector, productivity held steady at 4.1% (4.7% y/y) versus 4.2% growth in 1Q. The average rate of growth during the prior three years was unrevised at 6.0%.

Unit Labor costs in manufacturing rose 2.3% (3.7% y/y) following 2.8% growth in 1Q. The average of the prior three years was lowered to -0.1% from 0.7% mostly due to a much sharper decline during 2004 of 2.9% versus a 0.5% decline estimated earlier.

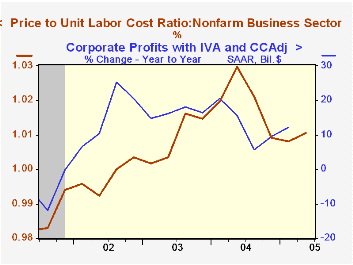

The implicit price deflator for nonfarm business rose 2.3% (2.3% y/y) and raised the ratio of prices to unit labor costs to the highest level since 3Q04, suggesting higher profit margins. During the last ten years there has been a 59% correlation between the ratio and the y/y growth in operating corporate profits.

Long-Term Yields Fall as Industrial Output Decelerates from the Federal Reserve Bank of Dallas is available here.

| Non-farm Business Sector (SAAR) | 2Q '05 | 1Q '05 | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Output per Hour | 2.2% | 3.2% | 2.3% | 3.4% | 3.8% | 4.0% |

| Compensation | 3.5% | 6.9% | 6.7% | 4.5% | 4.0% | 3.5% |

| Unit Labor Costs | 1.3% | 3.6% | 4.3% | 1.1% | 0.2% | -0.5% |

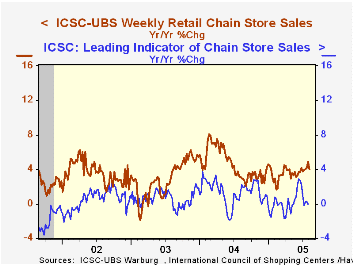

by Tom Moeller August 9, 2005

Chain store sales stuttered during the opening week of August according to the International Council of Shopping Centers (ICSC)-UBS survey. The 0.8% w/w decline retraced virtually all of the prior week's strong gain and left sales just 0.2% ahead of the July average.

During the last ten years there has been a 56% correlation between the y/y change in chain store sales and the change in non-auto retail sales less gasoline, as published by the US Census Department. Chain store sales correspond directly with roughly 14% of non-auto retail sales less gasoline.

The leading indicator of chain store sales from ICSC slid 0.8% (0.0% y/y), the third decline in the last four weeks.

The ICSC-UBS retail chain-store sales index is constructed using the same-store sales (stores open for one year) reported by 78 stores of seven retailers: Dayton Hudson, Federated, Kmart, May, J.C. Penney, Sears and Wal-Mart.

| ICSC-UBS (SA, 1977=100) | 08/06/05 | 07/30/05 | Y/Y | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| Total Weekly Chain Store Sales | 458.9 | 462.8 | 4.0% | 4.6% | 2.9% | 3.6% |

by Louise Curley August 9, 2005

Germany released preliminary June data on the balance of payments and data on the trade in goods. The preliminary balance of payments data for June are: the total current account, the balance on goods, supplementary trade items, the balance on services, the balance on factor income and current transfers. These items are available only on seasonally unadjusted basis. No June data on the financial account are yet available. While June exports and imports of goods are not shown in the preliminary balance of payments, they are included in the report on trade in goods where they are shown on a seasonally adjusted and unadjusted basis.

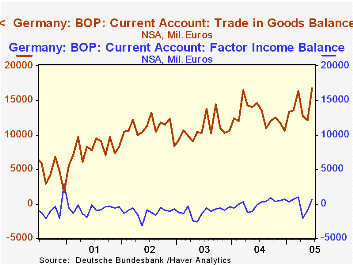

The current account surplus on a seasonally unadjusted basis increased 2.3 billion euros to 10,4 billion euros in June 2005 from 8.1 billion in June 2004. Since late 2001, Germany has had a positive balance on current account. Typically, a large positive balance on trade in goods outweighs negative balances on services and factor incomes and supplementary trade items and transfer payments that also result in an outflow of funds. This pattern has changed slightly as the factor income balance became positive in 2004. The balance turned negative in April and May of this year but has become positive again in June. The balance on factor income is the difference between receipts of investment income and wages from foreign countries and German payments of these factors to foreign countries. The first chart shows the factor income balance together with the balance on goods. The shift to a positive balance on factor income in 2004 may be due in part to the increase in Germany's direct investment abroad.

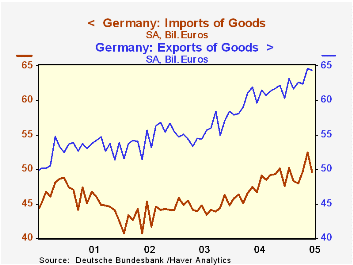

The seasonally adjusted data show a trade in goods balance of 14.79 billion euros an increase of 2.63 billion euros from a year ago. While exports declined 0.4% from May, they were over 8% above June, 2004. Imports were down sharply in June--5.5%--but they were 6,3% above June 2004. The second chart shows exports and imports on a seasonally adjusted basis.

| Germany Balance of Payments and Trade in Goods (Billions of Euros) |

Jun 05 | May 05 | Jun 04 | M/M Dif | Y/Y Dif | 2004 Mo. Avg | 2003 Mo. Avg | 2002 Mo. Avg |

|---|---|---|---|---|---|---|---|---|

| Not Seasonally Adjusted | ||||||||

| Current Account | 10.4 | 5.5 | 8.1 | 4.9 | 2.3 | 7.0 | 3.9 | 4.0 |

| Balance on Goods | 16.8 | 12.1 | 14.6 | 4.7 | 2.2 | 13.0 | 10.8 | 11.1 |

| Exports | 68.8 | 63.5 | 62.6 | 5.3 | 6.2 | 60.9 | 55.3 | 54.2 |

| Imports | 51.9 | 51.5 | 48.0 | -0.4 | 2.9 | 48.0 | 44.6 | 43.2 |

| Supplementary Trade Items | -1.3 | -1.0 | -1.1 | -0.3 | -2.0 | -1.0 | -0.7 | -0.5 |

| Balance on Services | -2.9 | -2.5 | -2.3 | -0.4 | -0.6 | -2.6 | -2.8 | -3.0 |

| Balance on Factor Income | 0.7 | -1.0 | -0.1 | 1.7 | 0.8 | 6.4 | -1.2 | -1.2 |

| Transfer Payments | -3.0 | -2.1 | -3.0 | -0.9 | 0.0 | -2.4 | -2.4 | -2.3 |

| Seasonally Adjusted | ||||||||

| Balance on Goods | 14.79 | 12.16 | 12.98 | 2.63 | 1.81 | 12.8 | 10.9 | 11.2 |

| M/M % | Y/Y % | |||||||

| Exports | 64.39 | 64.63 | 59.63 | -0.37 | 7.98 | 60.47 | 55.57 | 54.54 |

| Imports | 49.60 | 52.47 | 46.65 | -5.47 | 6.32 | 47.65 | 44.66 | 43.85 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief