Global| Oct 06 2008

Global| Oct 06 2008Exchange Rates Set the Stage…that Policymakers Play On

Summary

As we sit in the middle of a growing financial crisis exchange rates position countries in specific competitiveness cohorts. Much of what has transpired in the past few years has been framed importantly by those exchange rate [...]

As we sit in the middle of a growing financial crisis exchange rates position countries in specific competitiveness cohorts. Much of what has transpired in the past few years has been framed importantly by those exchange rate movements. This is so true that it would be hard to go back and to decide which caused which to happen: Did high oil hurt the dollar or did a weak dollar push up oil?

The real broad effective dollar index is down by 13.3% over 36 months. That term means that the index is the dollar’s value adjusted for inflation effects against a wide group of currencies in which weights are applied to reflect the importance of these countries in trade. The euro is up by 11% on a similar measure and yen is down by 13% over that same period. Currencies are not a zero sum game unless you include all the world’s currencies in the framework. The dollar can move differently Vs different currencies so it could theoretically fall Vs the euro but rise enough Vs the Canadian dollar (which is more important in terms of the size of bilateral direct trade flows) to push the broad US exchange rate index up.

Right now the world crises catches the dollar in the bottom 1% of its queue of (real) values since 1973. The yen is also low in its range, in the 2.8 percentile. The euro is strong in the top 98 percentile of its range. And… what got currencies into these positions is also partly what got us in trouble.

The EURO shot up and with the ECB focus on its ONE mandate as it cheered too much for that inflation fighting rise in the exchange rate as oil prices spurted. Yet it was the euro’s rise that helped the dollar to fall and with the world’s commodity prices denominated in dollars that helped to stoke up dollar commodity prices. This dynamic continued to help to push commodity prices as a spiral developed that included oil- especially oil!

As a result of such polices and currency shifts we find Europe currently undermined by foreign exchange strength whose lagged effects are finally taking a toll on EMU members. In the US a weakening US economy has seen its drop in domestic activity softened by strong US exports (and weaker imports) due importantly to a weakening and highly competitive dollar.

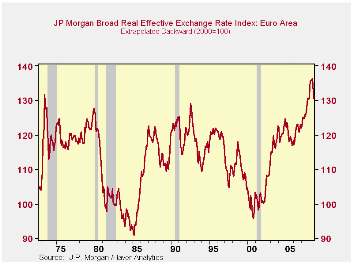

In the top chart we plot the broad real effective EMU exchange rate. Using EMU weights it has been projected backward to before the time that the EMU existed to show just how strong the euro has become. When the individual currencies of EMU member countries existed there was not a time when they collectively were as strong as they got to be in this cycle. This is why I have been warning for so long that Europe was going to slow down. Europe is a trading place. And while much of its trade is intra-Europe that is still not the same as intra-state shipments within the US. Intra EMU trading does eliminate the need for foreign exchange and there is a good deal of product homogenization in Europe but you still are dealing with a foreigner when you ship goods across national lines within EMU. For that reason a strong external exchange rate can undermine intra-EMU regional trade more easily than intra-state trade in the US.

On balance the strong euro is now an added burden for Europe where fiscal policy is off the table due to its Maastricht budget constraints. Coordinated programs for troubled banks are harder to get because of their members’ still-separate fiscal situations. The much vaunted EMU and EU customs trade union and monetary union are showing their Achilles Heels. Europe is not one country. It is no united states of Europe and this fact is one of the main things that has held it back and that continues to impede its operation in this crisis.

| Trade weighted FX Broad Real Range and Movements | ||||

|---|---|---|---|---|

| Aug-08 | US | EMU | Japan | UK |

| Current Index | 77.6 | 132.6 | 68.4 | 87.8 |

| Rank percentile | 1.2% | 98.6% | 2.8% | 30.6% |

| 12-Mo % | -6.3% | 5.7% | 0.4% | -11.8% |

| 24-Mo % | -9.5% | 7.8% | -4.6% | -10.4% |

| 36-Mo% | -13.3% | 11.0% | -13.1% | -9.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief