Global| Jul 17 2019

Global| Jul 17 2019European Vehicle Registrations Remain Subdued

Summary

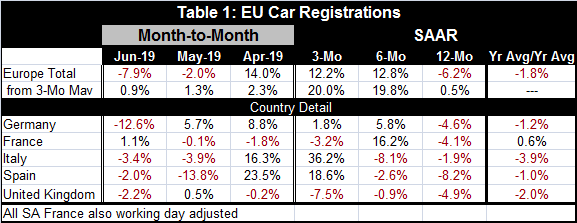

The slowdown in European vehicle registrations continues. June marks the second monthly decline in registrations in a row with a 7.9% drop. While shorter term growth rates are positive, the year-on-year pace is -6.2%. On three-month [...]

The slowdown in European vehicle registrations continues. June marks the second monthly decline in registrations in a row with a 7.9% drop. While shorter term growth rates are positive, the year-on-year pace is -6.2%. On three-month smoothed data, the monthly declines turn to small gains and the three-month and six-month growth rates get larger. But year-on-year, while growth no longer declines, it is quite weak at just a 0.5% gain.

The slowdown in European vehicle registrations continues. June marks the second monthly decline in registrations in a row with a 7.9% drop. While shorter term growth rates are positive, the year-on-year pace is -6.2%. On three-month smoothed data, the monthly declines turn to small gains and the three-month and six-month growth rates get larger. But year-on-year, while growth no longer declines, it is quite weak at just a 0.5% gain.

Unsmoothed trends

Unsmoothed individual country data show broad declines in June and May for vehicle registrations. Over three months and six months, the country trends are mixed and also quite erratic with no sense of ‘trend.’ Year-on-year all country level registrations show declines, ranging from a low of 1.9% in Italy to the greatest decline of 8.2% in Spain.

Smoothed results

Further smoothing of the data shows weakness. For this, we look to the far right column and calculate a broad percentage change. Over the last 12-month average compared to the previous 12-month average, registrations are down by 1.8% overall and falling in four of five countries with France as the exception with a 0.6% increase. The largest year-average decline is in Italy at 3.9% and the smallest is in Spain at 1.0%.

Registration rankings

Registration rankings

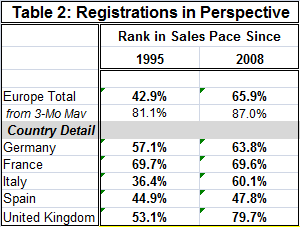

In additions to the battery of statistics in Table 1, I offer Table 2 that ranks the current sales pace on two timelines, one back to January 1995 and the other to January 2008. The overall European ranking since 1995 is 42.9%, below its median (which occurs at 50%). The rank since 2008 is higher with a 65.9 percentile standing. Rankings by country are uniformly higher since 2008 compared to the longer 1995 period (but for a very small exception in France). 2008 includes the recession and the post-recession weakness that lingered especially in Europe accounting for the better ranking when today’s sales are compared to the shorter period since 2008.

Smoothed and ranked

However, the smoothed data do not show such an extreme divide as the three-month average of sales ranks 87th since 2008 and 81st since 1995, a relatively modest difference.

Country level data

The country level rankings show nearly the identical standing for French registrations in both periods. Spain also shows small differences in rankings. Germany’s ranking difference is only 6.7 ranking percentile points. That leaves Italy and the U.K. as the two countries with the most significantly different rankings on these two timelines; both are - much stronger in 2019 relative to 2008 than since 1995. For Italy where the economy has been the second most severely impacted in all of EMU since the recession/financial crisis (surpassed only by Greece in that regard), Italy’s level of real GDP is still below its pre-recessionary level. Even so vehicle sales had outperformed the economy and consumer spending in recovery until 2018. Of course, vehicle registrations are stronger in comparison with the post 2008 period than the earlier period when the economy was stronger overall including registrations. For the U.K., the last few years have taken a toll on the vehicle sector with the fate of British-sourced manufacturing quite unclear with no Brexit deal in hand and lot of talk of a potentially painful hard Brexit.

Summing up

On balance, the 12-month average percent change is a powerful stable result that points to weakness in momentum. The rankings also point to moderate-to-weak levels of sales. It is not surprising that these data also point to France as overachieving relative to other European economies as other French data have been relatively firm or strong. Still, the overwhelming message here is that registrations are slowing down. In fact, they made a pretty clear break with trend in October 2018 and have been lagging ever since.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief