Global| Sep 13 2019

Global| Sep 13 2019European Trade and Current Account Surpluses Expand

Summary

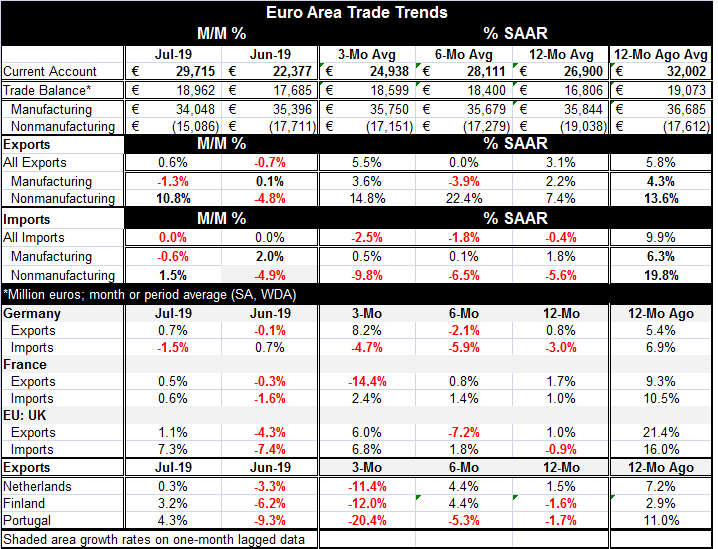

The EMU trade and current account positions shifted to post larger surpluses in July. Exports rose and imports were dead flat on the month. The trade surplus rose to 18.96 billion euros while the current account surplus moved sharply [...]

The EMU trade and current account positions shifted to post larger surpluses in July. Exports rose and imports were dead flat on the month. The trade surplus rose to 18.96 billion euros while the current account surplus moved sharply higher to 29.715 billion euros.

The EMU trade and current account positions shifted to post larger surpluses in July. Exports rose and imports were dead flat on the month. The trade surplus rose to 18.96 billion euros while the current account surplus moved sharply higher to 29.715 billion euros.

However, the balance on the trade account did not improve for manufactures trade where the surplus declined to 34.0 billion euros in July from 35.4 billion euros in June. The improvement in the overall balance came from nonmanufactures. Nonmanufactured exports rose by 10.8% in July as imports gained only 1.5%. But these are nominal flows and the vagaries of oil prices and the prices of other commodities tend to dominate nonmanufacturing in the short run.

Manufacturing exports are up by 2.2% over 12 months, down over six months and up over three months at a 3.6% annual rate all relatively muted trends. Nonmanufactured exports are much more robust, rising by 7.4% over 12 months and at a 22.4% annual rate over six months and at a 14.8% rate over three months. This strength is surprising.

Manufacturing imports are up by 1.8% over 12 months, up at a 0.1% annual rate over six months and up at a 0.5% annual rate over three months. The import flows have come to a near standstill over three months and six months. The imports of nonmanufactures are declining on this timeline, down by 5.6% over 12 months, down by 6.5% over six months and down by 9.8% over three months. The weakness in imports suggests that domestic demand in the EMU is weak. That view is reinforced by both weak manufactures and nonmanufactures imports.

Selected country level details in the lower panel of the table show mixed trends. German imports are falling and decelerating in line with the weak growth Germany has been posting and this weakness is now expected to continue. The IFO has projected recession for this year. French imports are on a slight accelerating path, but all recent growth rates are exceptionally weak at a pace of 2.4% of less. The United Kingdom logs a 0.9% import decline over 12 months, but the pace improves steadily from six-months to three-months. While Brexit is a concern in the U.K., Brexit uncertainty could be a factor boosting imports as firms fill inventories as a hedge against potential Brexit misfortune.

Exports show uneven acceleration for Germany and deceleration for France with a severe decline in French exports over three months. U.K. exports also erratically accelerate. The Netherlands, Finland and Portugal all show export declines over three months. Only Portugal displays clear ongoing deceleration, however.

The message from these trade flows is that trade is weak. There are no significant accelerations, but there is consistent expansion in the nonmanufactured exports of the EMU. Imports weakness confirms suspicions about the weak state of domestic demand in the EMU and serves to endorse the just-adopted program of stimulus launched by the ECB. The weakness in EMU manufactured exports and in the export flows of other countries shows that there is also a much larger global demand problem that is quite out of the reach of the ECB. But there has been at least some positive news on the matter of U.S.-China trade talks and that could yet produce beneficial results down the road. Even so, a substantial period of slack conditions seems to lie ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief