Global| Sep 23 2015

Global| Sep 23 2015European PMIs Take a Step Back; In a Big Picture Sense PMIs Remain Flat

Summary

The private sector PMI headline for EMU stepped back to 53.9 in September from 54.3 in August. This leaves the headline index back at its July level. Both the manufacturing gauge and the services gauge stepped back with manufacturing [...]

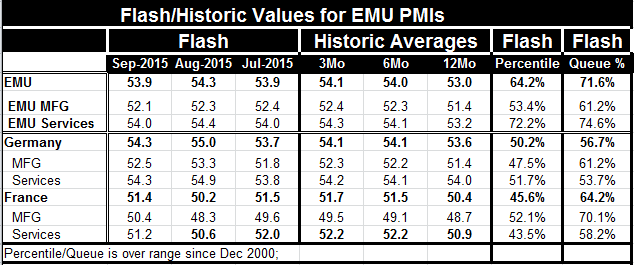

The private sector PMI headline for EMU stepped back to 53.9 in September from 54.3 in August. This leaves the headline index back at its July level. Both the manufacturing gauge and the services gauge stepped back with manufacturing below its July level and the service sector dead-even with its July level. Despite the set-back this month the EMU manufacturing index and the service sector index both show their 12-Mo to 6-Mo to 3-Mo moving averages moving higher even if only by small measures.

The private sector PMI headline for EMU stepped back to 53.9 in September from 54.3 in August. This leaves the headline index back at its July level. Both the manufacturing gauge and the services gauge stepped back with manufacturing below its July level and the service sector dead-even with its July level. Despite the set-back this month the EMU manufacturing index and the service sector index both show their 12-Mo to 6-Mo to 3-Mo moving averages moving higher even if only by small measures.

EMU continues to be led by the service sector. The service sector raw PMI is higher than the index for manufacturing and its percentile standing is greater as well. Services stand in the 74th percentile of their historic queue while manufacturing stands in its 61st percentile.

The German and French private sector PMIs have percentile standings below that of EMU (56.7% for Germany and 64.2% for France). This means that the smaller EMU nations are growing relatively better and are responsible for the higher overall PMI standing.

Germany's manufacturing percentile standing is at the same level as that for EMU as a whole. But the French sector has a higher percentile standing despite having a lower raw diffusion score than Germany. This divergence points out the relative nature of the PMI percentile standings. France's MFG sector is in absolute terms worse off than Germany's, but with each economy's current level compared to its normal status, it is France that is relatively better off.

The German service sector, however, has a much weaker standing than EMU as a whole (53.7% Vs 74.6%) and yet its raw diffusion score is much higher. Germany's raw diffusion score for services is higher than France's too, but France has a higher percentile standing (53.7% for Germany Vs 58.2% for France). Once again both have weaker percentile standings in Germany and in France than in EMU. This underscores the role in the smaller EMU economies' service sectors in advancing EMU growth.

China Today, in addition, the manufacturing PMI for China was released. China's MFG PMI marked a six and one-half year low. China is trying to shift growth over to the service sector but it still has important manufacturing and export sectors. Those sectors are being hammered by weak growth outside of China making it hard for China to export and to sustain manufacturing output. Thus global weakness reinforces more global weakness.

Greece The new Greek government has appointed cabinet positions and, as a result, the new Greek government looks a lot like the old Greek government. For now things in Greece are even keeling but we can expect some tricky times ahead. Greece is on the back burner as other, more pressing, concerns have moved to the top of the list.

The Muslim crisis For Europe job-one is now the migrant crisis. Former communist countries are balking at the number of migrants that the EU wants each of them to take. European leaders are meeting and this will be the hot -very hot- subject of the meeting. The problem does not seem to be the taking in of asylum-seekers per se as much as it is that these asylum-seekers are Muslim. The EU is asking for the injection of these migrants into some countries that have no Muslim population. In the U.S., Republican Presidential candidate Ben Carson has created his own stir by saying that, because of Muslim values, a Muslim could never be President in the U.S. Amid all this religion strife, the Pope is visiting the U.S. This is a curious juxtaposition of events centered on religion and religious tolerance...or the lack thereof.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.