Global| Mar 14 2016

Global| Mar 14 2016European IP Jumps; But Can It Hold the New Pace?

Summary

After falling for two straight months, industrial production (IP) suddenly is stronger in the euro area. That by itself is suspicious amid conditions of ongoing struggle. Consumer goods and capital goods output are rising strongly in [...]

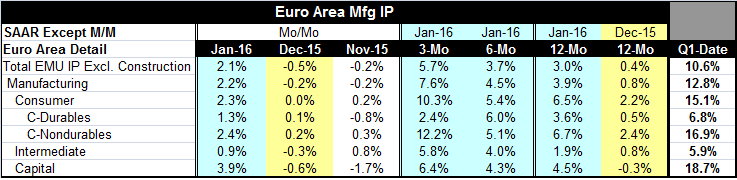

After falling for two straight months, industrial production (IP) suddenly is stronger in the euro area. That by itself is suspicious amid conditions of ongoing struggle. Consumer goods and capital goods output are rising strongly in January, followed by a quite solid gain in the output of intermediate products. The rebounds are apparent in all output categories. Only consumer durable goods output is not showing growth accelerate from 12-month to six-month to three-month. But for durables, its three-month growth rate still exceeds its 12-month rate of growth. The pace of growth in January is not only impressive, but it seems out of line with both the reported January and February manufacturing PMI reports already released as well as some already reported national-level gauges. This is a quandary.

After falling for two straight months, industrial production (IP) suddenly is stronger in the euro area. That by itself is suspicious amid conditions of ongoing struggle. Consumer goods and capital goods output are rising strongly in January, followed by a quite solid gain in the output of intermediate products. The rebounds are apparent in all output categories. Only consumer durable goods output is not showing growth accelerate from 12-month to six-month to three-month. But for durables, its three-month growth rate still exceeds its 12-month rate of growth. The pace of growth in January is not only impressive, but it seems out of line with both the reported January and February manufacturing PMI reports already released as well as some already reported national-level gauges. This is a quandary.

But it is perhaps not quite the quandary it appears to be. Economic growth has been weak and a growth rate for manufacturing production of 2.2% on the month is excellent and 3.9% year-on-year seems relatively too strong. However, if we rank the year-on-year growth in manufacturing IP since early 2008, it has an 80 percentile standing among all those growth rates. Over that period, manufacturing growth (y/y) has been higher only 20% of the time. The manufacturing PMI for that same period is in its 75th percentile, higher just 25% of the time. So through January, the two gauges (one based on a year-on-year growth rate, the other on a PMI index) are roughly compatible. However, in February, the manufacturing PMI stepped down and to a much weaker 53rd percentile standing. That would be consistent with a drop in the year-on-year IP pace to the neighborhood of 1.5% and that would imply monthly drop in EMU output of about 2.3%, an unwinding of this past month's gains. Output is a volatile series, but even back to August 2014, the largest months drop has been only -1.4%. It seems likely that the IP report is going to overshoot the ISM gauge for a while or that IP will weaken suddenly. For the record, in the past large IP spikes like this have tended to be preceded or followed by a drop that is at least 50% the size of the gain or larger. This suggests that the acceleration signal at least will be blunted.

Country level data show still strong growth in the three largest EMU economies (Germany, France and Italy), but with Spain, the fourth largest, having IP gains dead flat over three-month and six-month. Outright declines in output persist in Finland, Malta and Portugal. For the rest of the euro area, real manufacturing output growth right now is solid. But as the chart makes clear, that is because we measure all these growth rates from an elevated January level. What is not clear is whether the January level or growth pace will be sustained.

As the first month of a new quarter January output shows a huge 10% annualized gain for headline output over its Q4 average level. That is another way of saying that January is marked departure from the numbers reported in earlier months. So does that point to further acceleration or to this report being a fluke? Manufacturing output is up at 12.8% annualize rate in the nascent quarter led-oddly- by the output of capital goods and of consumer nondurables. That is not right as nondurable goods are not usually a leading volatile sector. Capital goods output is up at a huge nearly 19% annualized rate in the quarter. The monthly gain of 3.9% for manufacturing was last greater in December 2009 and September 2005 before that (barely higher in both cases). And in neither case did the spike signal an ongoing speed up.

As much as it is encouraging to see a strong IP headline, these headlines turn out not to be reliable indicators of growth. The PMI framework tends to be steadier and more trend-driven in its moves and therefore is more believable as a trend indicator. The manufacturing and services PMIs for the EMU have been losing momentum.

So this may be a bit of a false signal from the industrial output report where seasonal adjustment, working day variations and weather can create false outsized gains. And weather has already been cited as the reason for the IP spike in Germany for January. It may have been factor elsewhere in Europe which is geographically concentrated. World trade flows continue to ratchet to a slower pace. There simply are not enough supporting signals to make this spike in IP seem reliable although there is no denying that it is broad-based. On balance, we have to judge the January signal as a likely false positive signal for acceleration. But as always until a few companion observations confirm or deny a new trend, the jury will remain out.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief