Global| Feb 26 2016

Global| Feb 26 2016Europe Shows Widespread Weakness

Summary

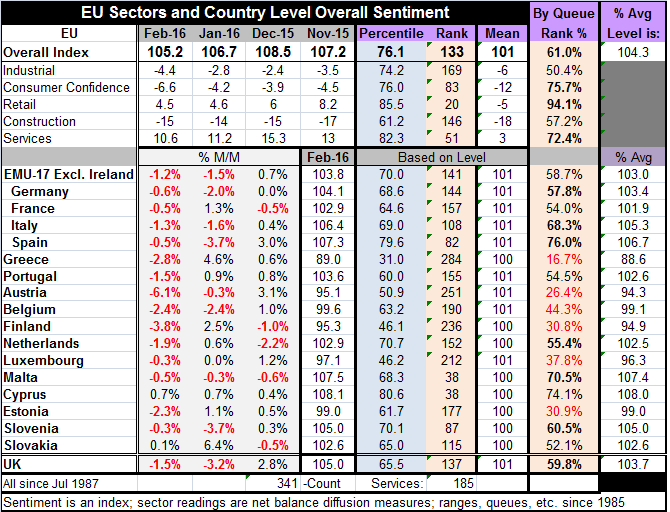

Of the 25 reporting EU members for February, the comprehensive EU Commission indices deteriorated in all but three countries. Those three were Cyprus, Poland and Slovakia. Sector indices also weakened across the board with significant [...]

Of the 25 reporting EU members for February, the comprehensive EU Commission indices deteriorated in all but three countries. Those three were Cyprus, Poland and Slovakia. Sector indices also weakened across the board with significant setbacks in the industrial sector, to consumer confidence and for services. Retailing barely edged lower while the construction sector lost one point on the month.

Of the 25 reporting EU members for February, the comprehensive EU Commission indices deteriorated in all but three countries. Those three were Cyprus, Poland and Slovakia. Sector indices also weakened across the board with significant setbacks in the industrial sector, to consumer confidence and for services. Retailing barely edged lower while the construction sector lost one point on the month.

The sector `queue standings,' which position the topical sector diffusion readings in a queue of historic data, show the industrial sector barley above its median on a reading in its 50.4 percentile. The construction sector resides in its 57th percentile. Services have a 72nd percentile standing and consumer confidence has a 75th percentile standing. Retailing, with a small setback this month, continues to be the relative backbone of growth with a 94th percentile standing - stronger historically only 6% of the time.

Still, in raw terms, the industrial measure, consumer confidence and construction post net negative diffusion readings even though they all are above their historic medians.

By country, the large EMU economies are not faring very well with Germany having an overall sentiment standing in its 57th percentile, France in its 54th percentile, Italy in its 68th percentile, and Spain in its 76th percentile. Spain's reading is firm. The rest are quite moderate readings. Spain, in fact, has the highest queue standing of any country in the table. And that is not impressive.

There are six countries with queue standings below their historic medians (less than 50). Six others sit somewhere in their 50th to 59.99th percentile range. Two sit in their respective 60th to 69.99th percentile with three in their 70th percentile range. It is a set of observations skewed to mediocrity or worse.

EMU members are still waiting for the ECB to take further action. All are watching the news regarding Brexit. As the G20 meets, the IMF is warning of further forecast downgrades even though it just downgraded its forecast. The IMF is pushing for more stimulus and many are trying to urge fiscal stimulus. In the euro area, few countries could afford to engage in any fiscal stimulus because they are up against Maastricht guidelines. For its part, in Germany, a German official noted today that there was little more good that monetary policy could do. Germans also have consistently been opposed to action that would violate the Maastricht fiscal criteria as well. On that view, Europe is simply up against the wall.

At the G-20 meeting, China tried reassure on the renminbi exchange rate claiming there was no reason to look for the exchange rate to fall continuously and claiming that the central bank still had tools and options. But China's main impact was to jawbone instead of to act.

Meanwhile, the geopolitical backdrop is difficult. Russia was bombing the bejeebers out of the Syrian rebels of its choice ahead of a possible but dubious ceasefire. Iran is having its first elections since sanctions were lifted by the West. The U.S. and China came to terms over sanctions on North Korea for its recent violations. But China continues to be accusatory of the U.S. over its actions in the South China Sea and is opposed to the U.S. putting a missile shield in South Korea and to the presence of long range radar installations there. China is now asserting its right to place missiles on what it calls `its soil' instead of denying what it is doing in the South China Sea Islands it has annexed or built.

And so life goes on and it is increasingly complicated. Global economic and geopolitical relations are intertwined in increasingly complex ways. There are both alliances and loggerheads among the same pairs of countries or groups of them. Economic options are running down; that is for sure. And if fiscal policy is off the table, there may be no viable options left for stimulus. We are, however, left to ponder how in such a weak environment U.S. inflation is going to take root and grow, or how the U.S. economy will respond if the Fed really takes out the weed-killer and applies it liberally. As the IMF pointed out, there are many more questions than there are answers at the moment. And increasingly the revisions to the outlook are on the downside in an entangled global scene where one man's feast is another's famine. And one man's policy option is another's nonstarter.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief