Global| Oct 01 2014

Global| Oct 01 2014Europe's Manufacturing Stays One Half-step ahead of Stagnation; But Is It Losing the Race?

Summary

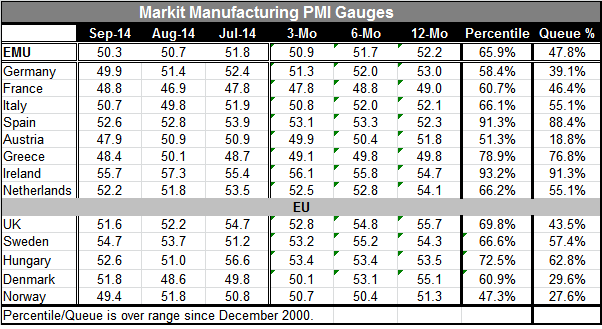

The manufacturing PMI for the European Monetary Union edged lower to 50.3 in September from its already weak 50.7 reading in August. The September reading of 50.3 stayed just ahead of the reading of 50.0, which would indicate [...]

The manufacturing PMI for the European Monetary Union edged lower to 50.3 in September from its already weak 50.7 reading in August. The September reading of 50.3 stayed just ahead of the reading of 50.0, which would indicate stagnation in the manufacturing sector. That's a thin lead on stagnation.

The manufacturing PMI for the European Monetary Union edged lower to 50.3 in September from its already weak 50.7 reading in August. The September reading of 50.3 stayed just ahead of the reading of 50.0, which would indicate stagnation in the manufacturing sector. That's a thin lead on stagnation.

Germany's manufacturing indicator dipped below 50, at 49.9 in September. As Europe's largest economy, it helped to lead the way lower.

Of the countries in the table reporting national manufacturing indices, four have readings below 50. Standings below 50 are found in Germany, France, Austria and Greece. This list includes the two largest European economies. Five countries saw their manufacturing PMI fall in September compared to August. The overall EMU reading fell. In August six of eight countries reported weaker PMI readings, and once again the EMU overall reading fell.

Over three months, six of eight countries have weaker manufacturing PMI readings. Over six months, seven of the countries have weaker manufacturing PMI readings. Over 12 months, five of the countries have weaker PMI readings.

The above comments have to do with the levels of the PMI readings and their changes over various horizons (momentum). However, we can also assess the level of the PMI relative to its historic performance. On that basis, the queue percentile standing for the overall EMU manufacturing sector stands in its 47.8 percentile. On this basis, the 50 percentile represents an indicator's historic median. While the EMU PMI is above 50, at 50.3, it indicates some very modest expansion indeed. This level is below the median value for the EMU PMI.

EMU's largest economy: Germany tends to have a strong economy. For this reason, its PMI reading of 49.9 has an extremely weak standing, in its 39.1 percentile. Germany's current PMI value does not look that weak, compared other countries even though it's below 50. However, on a percentile standing basis, it is extraordinarily weak since the German economy is used to being strong.

The rest of the Big Four: France, with its PMI reading of 48.8, has a standing in its 46th percentile. Italy, with its PMI at the 50.7 level, has its PMI standing in the 55th percentile. Spain, with a reading of 52.6, has its PMI at an 88 percentile standing. Spain is unaccustomed to high manufacturing PMI standings. Its PMI reading of 52.6 corresponds to a very high percentile standing.

Austria, like Germany, is accustomed to a strong manufacturing sector. Its PMI reading of 47.9 in September leaves it in the lower 18.8% of its historic queue, the weakest relative reading in the table. Greece, with its 48.4 PMI reading, has a standing in its 76.8 percentile. Greece, of course, is a country unaccustomed to manufacturing strength so moderate contraction is historically a good result for the country. Ireland, with the PMI reading of 55.7, has a queue standing in the 91st percentile. The Netherlands, at 52.2 for its September PMI, has a standing in its 55th percentile.

At the bottom of the table, we have readings for assorted EU members. The readings are, for the most part, middling to weak. The U.K., which had been posting some very strong numbers, has been slipping and now has a manufacturing standing in only its 43rd percentile. Sweden's standing is in its 57th percentile, having advanced in each of the last two months. Hungary is amid a partial bounce-back in September after falling relatively sharply in August and has the 62nd percentile standing. Both Denmark and Norway have been weak. Denmark showed an increase in September, while Norway posted a decline. Denmark's queue standing is in its 29th percentile, while Norway's is in its 27th percentile, different paths but similar results.

Weakness in Europe is widespread. The PMI readings, for the most part, are low, even though for some countries those levels represent relatively strong readings. For others, like Germany and Austria, these sub 50 readings are quite weak compared to what they are used to historically. We can think of the PMI values as representing their absolute strength and the queue standings as relative strength. On both measures, Europe is weak. In addition, its momentum is still deteriorating. Three strikes and you're out.

Today the European Union announced it would keep it sanctions on Russia in place. The European Central Bank has no new stimulus program in place, but we're still waiting to see if its past actions are going to bear fruit. So far, there is not much evidence of that.

Today France announced budget numbers showing that it will be continuing to miss its deficit targets for the next couple of years. While such weak numbers may be putting more pressure on the back of the ECB, it's unclear to me exactly what the ECB could do that has a strong chance of being successful. The ECB seems to be pretty stretched right now with the Germans unwilling to bend the ECB's charter any further.

All this reliance -globally- on central banks seems to be misplaced. Europe's economies still generally have high debt-to-GDP ratios from past indiscretions. While this is not helpful now, it should be a strong reminder in the future as to why, when times are good, budget deficits need to be reined in. If they are not reined in, when the times get bad, fiscal policy may be off the agenda, which seems to be the case in Europe right now. Perhaps the take away for the U.S. from all this is that it should rethink its current reliance on such an expansive monetary policy while its economy is still growing lest it does not have any options when its growth falls short and needs some help.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief