Global| May 02 2013

Global| May 02 2013Europe's Manufacturing Sector Flounders

Summary

The manufacturing PMI for the euro area contracted a bit more slowly than in its preliminary estimate. The PMI indicator fell to 46.69 from 46.75, a marginal creep lower in April. Although France continues to be under a lot of [...]

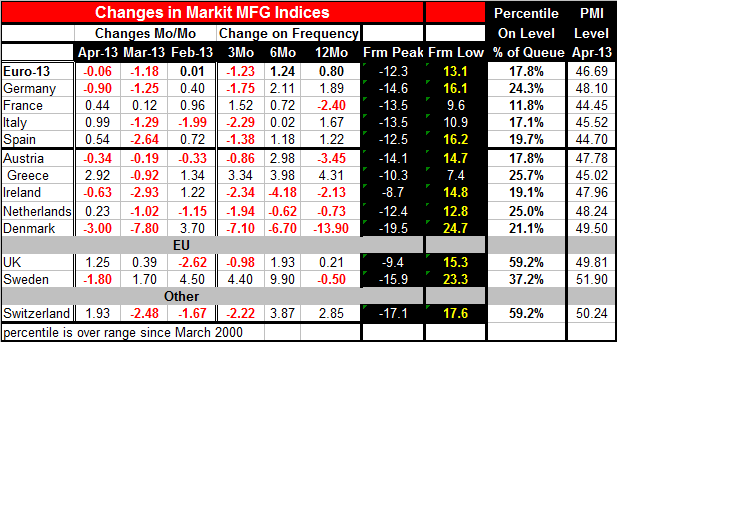

The manufacturing PMI for the euro area contracted a bit more slowly than in its preliminary estimate. The PMI indicator fell to 46.69 from 46.75, a marginal creep lower in April.

The manufacturing PMI for the euro area contracted a bit more slowly than in its preliminary estimate. The PMI indicator fell to 46.69 from 46.75, a marginal creep lower in April.

Although France continues to be under a lot of pressure France is the only country in the table that has mounted three straight months of increases in its manufacturing PMI. Having said that, France also has the lowest standing of its PMI in its historic range among these reporting EMU members. The French PMI has been weaker than its April value only about 12% of the time. And two of those episodes are from the two previous months.

Denmark appears to be getting sucked into the vortex of weakness. It's PMI fell by an outsized 7.8 points in March and followed that up with a 3 point drop in April. However, Denmark is only garden-variety weak standing in the 21st percentile of its historic queue, above the level for the Eurozone as a whole as the Eurozone stands in the 17.8 percentile of its historic range. Denmark is a curious case. Denmark is the country in the table with the largest drop from its peak in this cycle: it is still off 19.5 points from its cycle peak. However, Denmark is also the country with the largest rise from its cycle low: it's up by 24.7 points from its cycle low. Denmark has been subjected to great deal of volatility during this period. It has, despite its recent declines, the strongest raw PMI reading among European Monetary Union members in the table, although it's percentile ranking remains moderate as it ranks below the Netherlands which is in the 25th percentile of its queue, Greece which is in the 25.7 percentile of its queue in Germany which is in the 24.3 percentile of its queue, rnaking it as fourth among these nine fellow Zone members.

The PMI readings for April, despite being somewhat mixed, are still quite weak because we are coming off of the month of March in which PMIs declined across all the EMU countries (in many cases, sharply) except France. Of the nine EMU member countries in the table, all except France and Greece also show net declines over three-months. Over six-months, however, only three EMU countries are declining; in two of them the declines are rather sharp. The weak reporters are Denmark followed by Ireland with minor erosion and the Netherlands. Over 12-months five of the nine members are weaker: Denmark which has slipped by over 13 points, Austria which has slipped by nearly three and a half points, France which has slipped by nearly two and a half points, Ireland that has slipped by two points and The Netherlands that has slipped by about three quarters of a point.

The European Central Bank did cut rates today, as expected, for the first time in 10 months and lowered its main interest-rate by one quarter of a point to stand at a record low rate for that bank at 0.50 percent. While there was rather intense speculation about the ECB, at the same time there are few thinking that this rate changes will have much impact on the euro-Zone. I would expect little impact on economic variables or on markets because one of the main reasons that central banks affect market rates when they make rate changes is that they can create the expectation that there's more to come. In this case as a euro-Zone approaches the zero bound everyone can see that there is not more to come, in fact, there is less to come.

What's likely to happen next, is that speculation will begin to generate about what else Europe can do. The Germans and the Bundesbank have made it pretty clear that they are going to try to enforce the rules that govern ECB's behavior to the letter of the law. That will make unlikely that the ECB will be able to engage in any of these quantitative excesses (QE) that we see in Japan, in the UK and in the US. With the Zone floundering, the next thing that we would expect is that that intense pressure would develop on fiscal policy... except in the euro-Zone there is no common fiscal policy. This cut will, nonetheless, begin to create pressures and expectations for the euro-Zone managers, central bankers, politicians and others to pull some sort of rabbit out of their hat.

Good luck with that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief