Global| Nov 14 2008

Global| Nov 14 2008Europe's GDP and the Auto Sector Woes

Summary

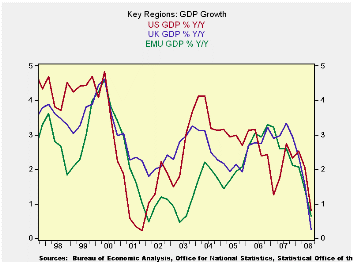

The decline in US, UK and EMU GDP growth is all occurring at once. Yr/Yr GDP growth is in a slowing down mode with the slowing at a rather severe pace. We can see that the degree of slowdown and the low pace of growth are both [...]

The decline in US, UK and EMU GDP growth is all occurring at

once. Yr/Yr GDP growth is in a slowing down mode with the slowing at a

rather severe pace. We can see that the degree of slowdown and the low

pace of growth are both comparable to the decelerations in 2000-2001.

At that time the decelerating came from a higher pace of growth to

start with.

While the US is being made the ‘poster boy of the downturn’ in

terms of being the cause of this recession, the data show us that the

persisting sharp slowing in growth began in EMU as its currency rose

above level that growth in that region could tolerate.. The decline in

the UK growth rate came later and has been synchronous with the decline

in the US growth but UK growth has fallen harder- from a higher initial

pace.

The US suffered worse in the earlier cycle, around the year

2000, as its growth dropped from an above European pace to a below

European pace at the trough. But the US economy subsequently had a

recovery phase that was quite robust pushing US growth above the growth

rates in EMU and the UK from 2003 – 2006. Then US growth began to get

erratic. But the ongoing cyclical weakness in the US did not start

again until nearly four quarters after EMU’s GDP began to make its

ongoing turn for the worse at the of 2006. EMU Yr/Yr growth peaked late

in 2006 at 3.3% and has since then been steadily eroding.

Right now the UK, EMU and the US (Japan, and many others, too)

are engulfed n a synchronous downturn. And it has begun to create

tensions.

In the US, the automakers are in trouble as unit auto sales

slipped to just above a 10mu unit rate last month an extremely low pace

that implies crushing overhead costs from fixed business charges. .

With a huge number of jobs linked to the auto sector, the US is

concerned that GM, Ford and Chrysler are in such straights. And with a

bailout plan that has been used to help financial firms there is now a

clamoring in the US to help the auto makers. But in Europe auto sales

are weak too; there sales have fallen for six months running. The

European Commission warned it would contest any U.S. bailout for the

sector that broke state aid rules. Insurers in Europe have withdrawn

credit protection for auto suppliers that protected them in the event

of bankruptcies of the US auto makers. Asian and European automakers

are feeling the pinch but still are not in the desperate circumstances

that US car makers face.

The EU Threat

"We are in the process of analyzing the <US>

plan. The plan has not yet been presented yet. Of course, if it is

illegal state aid, we will act at a WTO level," Commission President

Jose Manuel Barroso has said. So the lines are drawn. The risk is

protectionism and its ability to create a deep downward spiral since it

is hard to imagine that the US would let a European protest stand in

the way of supporting the automakers. And if the US did that the

Europeans surely would gain some WTO sanctioned recourse to retaliate

and that is how the mess gets out of hand.

So yes, economies are weak. Financial sectors are strained.

Central banks are cutting rates. There have been some assistance plans.

In the US where import penetration is the most freely allowed, the US

automakers are feeling the pinch. As US lawmakers argue about remedies

for the ‘Big Three’ European’s plan a surprise attack of their own

through WTO. If you think the only risk here is the economic downturn

and the financial sector, you are fooling yourself.

| Euro-Area and main G-10 country GDP Results | |||||||

|---|---|---|---|---|---|---|---|

| Quarter over quarter-Saar | Year/Year | ||||||

| GDP | Q3-08 | Q2-08 | Q1-08 | Q3-08 | Q2-08 | Q1-08 | Q4-07 |

| EMU-15 | -0.8% | -0.7% | 2.7% | 0.7% | 1.4% | 2.1% | 2.1% |

| France | 0.6% | -1.1% | 1.6% | 0.6% | 1.2% | 2.0% | 2.2% |

| Germany | -2.1% | -1.7% | 5.7% | 0.8% | 1.9% | 2.7% | 1.7% |

| Italy | -2.0% | -1.8% | 2.1% | -0.9% | -0.2% | 0.4% | 0.1% |

| The Netherlands | 0.1% | 0.0% | 1.3% | 1.6% | 2.9% | 3.7% | 4.1% |

| UK | -2.1% | 0.0% | 1.1% | 0.3% | 1.5% | 2.4% | 2.9% |

| US | -0.3% | 2.8% | 0.9% | 0.8% | 2.1% | 2.5% | 2.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief