Global| Jan 17 2018

Global| Jan 17 2018Europe's Car Registrations Step Back at Yearend

Summary

Interestingly, now while there has been more optimism expressed about the European recovery, vehicle registrations have stalled. The chart shows that real retail sales volumes are still moving higher. But they also show vehicle [...]

Interestingly, now while there has been more optimism expressed about the European recovery, vehicle registrations have stalled. The chart shows that real retail sales volumes are still moving higher. But they also show vehicle registrations have become extremely erratic and essentially trendless over the past six months or so. Retail sales volumes took about eight years to get back to their pre-crisis levels, but since doing that, they have stayed on a solid up trend as vehicle registrations have sputtered.

Interestingly, now while there has been more optimism expressed about the European recovery, vehicle registrations have stalled. The chart shows that real retail sales volumes are still moving higher. But they also show vehicle registrations have become extremely erratic and essentially trendless over the past six months or so. Retail sales volumes took about eight years to get back to their pre-crisis levels, but since doing that, they have stayed on a solid up trend as vehicle registrations have sputtered.

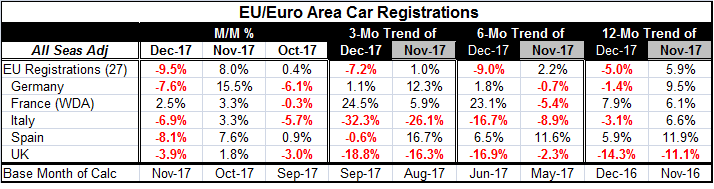

The table shows month-to-month changes as well as changes over three months, six months and 12 months for both November and December to demonstrate the impact of one month's erratic move even on broader growth rates. November saw an 8% jump in 'sales' that led to December's 9.5% drop. In December the year-over-year change in registrations is a drop of 5%; as of November it showed a gain of 5.9%. Registrations have become a very noisy series.

December sales were weak in part because the month lacks one selling day compared to 2016. That also helps to explain why there are registration declines across all the listed countries in December, except France. Broad-based weakness would be expected from such a calendar effect since we are all on the same calendar.

Amid the volatility, two trends still stick out. Both Italy and the U.K. show declines in registrations over three months and six months for both November and December calculations. The U.K. also shows declines year-over-year for both months over a 12-month span. The U.K. shows the weakest trends of all as it is suffering some high-end business drains as its banking sector is in part migrating into the euro area. The loss of high-end jobs will also mean the loss of high-end auto sales.

France has the strongest data. It shows registration gains in December and November as well as over most horizons regardless of having a November endpoint or a December endpoint. French sales are up the strongest over 12 months for calculations ended in December; for November-ending calculations France lies below Spain, Germany and Italy but still logs a rise of 6.1%.

Clearly, auto registrations are difficult to pin down. But just as clearly there has been a loss of trend and an onset of oscillation. Trend gains may still lie ahead for the series, but it is hard to tell from the recent data. Certainly, the ongoing rise in retail sales is encouraging as are the strong manufacturing and services PMI readings and the ongoing drops in European unemployment rates. There is no denying the progress that has been made in Europe. The only question is what happens when the ECB takes off the training wheels?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief