Global| Jul 10 2008

Global| Jul 10 2008Europe is Taking a Turn for the Worse…

Summary

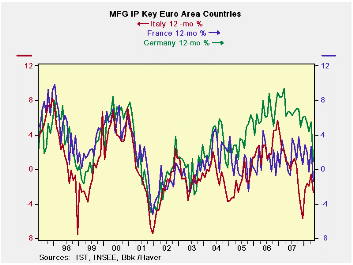

Industrial output in the Euro Area is now in a clear downturn, judging from the trends in the Zone’s main economies. For a while, as the euro rose in value, it seemed as though the Euro Area was bullet-proof. German industrial [...]

Industrial output in the Euro Area is now in a clear downturn, judging from the trends in the Zone’s main economies. For a while, as the euro rose in value, it seemed as though the Euro Area was bullet-proof. German industrial readings remained strong and even had some acceleration has the rest of the Zone and world economies seemed to feel the weight of the pressure of rising oil prices and financial distress. Now that has changed. Italy has been very weak- arguable recessionary – for some time. France has recently given up the pretense of buoyancy and has weakened sharply. In Germany Yr/Yr industrial output growth is now up by just 0.9%.

Good weather was one factor helping Europe to set aside weakness early in the year. But now the wind aided output run is having its true trend laid bare. Output is steadily decelerating in Germany the Euro Areas strongest economy as well as in, France, Italy, Spain and in the EU’s UK. Over the key time horizons for analysis output is unequivocally falling (3-Mo 6-Mo and 12-Mo) with scant exception. Quarter to date growth is weak except for Spain where it’s volatility that is king much more resiliency.

The Euro Area is weakening quickly showing why the ECB felt it only needed to hike rates once as a defense of its honor more than in pursuit of its policy objective: to cap EMU inflation at 2%. It did not feel it needed to act to knock down inflation since I suspect that it agrees with the finance ministers’ unspoken concerns that the various economies are going to do that on their own due to encroaching economic weakness that is now making itself clearly felt.

In time the ECB may undergo criticism for even this small 25bp hike. In its defense it held its hand for a long period trying not to exacerbate all the financial problems as inflation shot over its ceiling. It finally felt that with inflation MORE THAN DOUBLE its inflation ceiling, it had to be seen doing something. It’s hard to argue with that.

| Main E-zone Countries and UK IP in MFG | |||||||

|---|---|---|---|---|---|---|---|

| Mo/Mo | 3-Mo | 6-mo | 12-mo | ||||

| MFG Only | May-08 | Apr-08 | Mar-08 | May-08 | May-08 | May-08 | Q-2-Date |

| Germany: | -2.6% | -0.3% | -0.3% | -12.2% | -1.9% | 0.9% | -8.3% |

| France:IP excl Constructions | -2.6% | 1.5% | -1.1% | -8.8% | -1.7% | -1.2% | -2.0% |

| Italy | -1.5% | 0.3% | -0.2% | -5.3% | 0.9% | -2.7% | -2.6% |

| Spain | -14.6% | 27.5% | -16.9% | -32.9% | -9.5% | -7.4% | 26.7% |

| UK | -0.6% | 0.1% | -0.5% | -3.8% | -0.8% | -0.8% | -1.8% |

| Mo/Mo are simple percent changes others are at saars | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief