Global| Aug 29 2014

Global| Aug 29 2014Europe Is Beset with High Unemployment and Disinflation

Summary

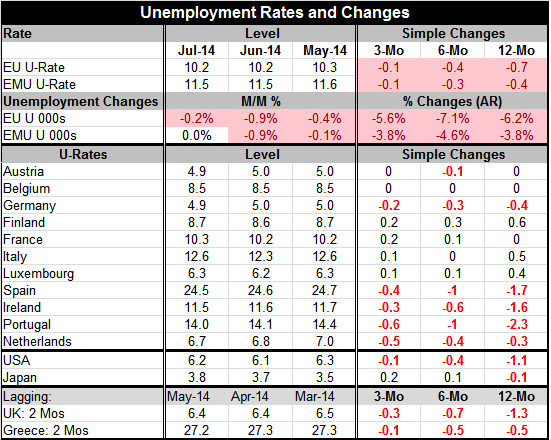

Today's data underscore the difficulty faced by the European Monetary Union. The unemployment rate remains high and declines are being posted generally only in the peripheral countries (the Netherlands, an exception to this) that have [...]

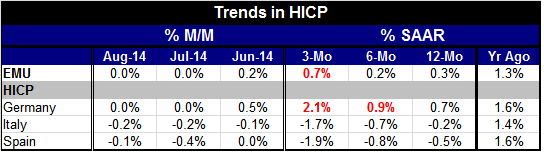

Today's data underscore the difficulty faced by the European Monetary Union. The unemployment rate remains high and declines are being posted generally only in the peripheral countries (the Netherlands, an exception to this) that have the highest rates of unemployment. High unemployment core members, Italy and France, have a rising unemployment trend as inflation drops. Meanwhile, the euro area inflation rate has continued to drop with the year-over-year rate at 0.3%, close to its all-time lowest pace. The European Central Bank is focused on stopping disinflation and trying to convince us all that deflation is not a threat. But this downshift in inflation clearly is not good news for the ECB or for its no deflation-risk argument. Credibility is especially shaken as the euro-economy continues to be buffeted by external shocks from geopolitical forces largely beyond anyone's control.

Today's data underscore the difficulty faced by the European Monetary Union. The unemployment rate remains high and declines are being posted generally only in the peripheral countries (the Netherlands, an exception to this) that have the highest rates of unemployment. High unemployment core members, Italy and France, have a rising unemployment trend as inflation drops. Meanwhile, the euro area inflation rate has continued to drop with the year-over-year rate at 0.3%, close to its all-time lowest pace. The European Central Bank is focused on stopping disinflation and trying to convince us all that deflation is not a threat. But this downshift in inflation clearly is not good news for the ECB or for its no deflation-risk argument. Credibility is especially shaken as the euro-economy continues to be buffeted by external shocks from geopolitical forces largely beyond anyone's control.

Germany's Finance Minister Wolfgang Schaeuble has said that the ECB has run out of ways to help the euro area. He emphasizes the point made by ECB President Mario Draghi at the Kansas City Fed symposium in Jackson Hole, Wyoming just a week ago. There Draghi said that the burden is on governments to speed growth and to find a way to do it without running excessive deficits. Schaeuble claims that monetary policy can only buy time.

Today the EU has announced that there will be more help for dairy producers because of damage created by the sanctions on Russia and its backlash. That is something to help ease the blow from the geopolitical chaos enveloping Europe, but it's a small something.

There is plenty of weakness in the euro area; it's clear that is not going away soon. Italy reported a record price decline. Spain's retail sales that started to rise are falling again. The euro-coin indicator that takes the pulse of the euro-economy sees more weakness ahead for the euro area.

While U.S. data have also been somewhat touch and go, Japan has reported some weak economic data: its household spending has fallen, housing starts have declined more than expected, and industrial production has turned out to be more listless than expected.

The global economy shows a great deal of weakness and there are disinflationary forces in many countries around the world. The U.S. is one place where inflation shows signs of having bottomed and having some moderate upward momentum.

Still, Europe has to deal with the cards it's been dealt and just as its recovery was gaining some momentum it ran into a flat spot and that flat spot in its trend has been pressured and turned into a downtrend by a collision with a recalcitrant Russia and sanctions that have come with some significant blowback effects for euro area members.

The geopolitical front appears to be as hot as ever although today troops described as pro-Russian separatists are allowing an encircled group of Ukrainian soldiers safe passage back home. NATO has declared that there are more than 1,000 Russian troops in Ukraine and calls it a blatant violation of Ukraine sovereignty. Yet, NATO has yet to take any action. Ukraine is not a NATO member.

As we can see, the economy's difficulties are not going away. The sole bit of good news from Europe today was from the U.K. which reports strong consumer confidence. That difference in monetary policy in the U.K and in the EMU is boosting sterling vs. the euro. Speculation is mounting that the Bank of England soon will raise interest rates and leave its policy of special accommodation behind it. On the other hand, it is clear that the ECB's hands are tied and policy in the EMU will remain accommodative; this effect will operate on other exchange rate pairs too. Market forces will push the euro lower and will help to spur growth in the euro area. As we saw with Japan, its accommodative monetary policy began to have impact when the exchange rate moved lower. This could be the ECB's most powerful weapon against weakness, especially with Russian markets now off limits.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief