Global| Sep 30 2014

Global| Sep 30 2014Europe Dodges a Bullet; EMU Unemployment Rate Stays Put in August

Summary

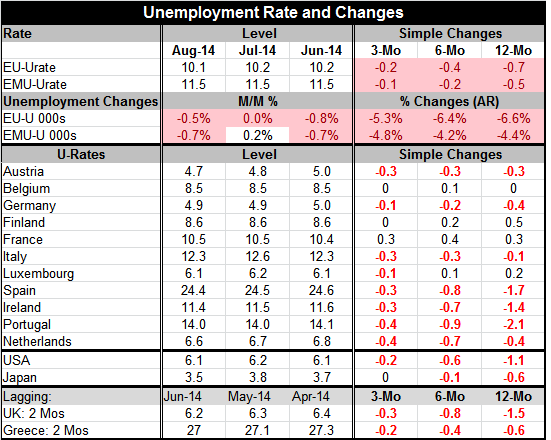

The unemployment rate in the European Monetary Union stayed put at 11.5% in August. The unemployment rate for the broader European Union fell slightly to 10.1% in August from 10.2% in July. Unemployment remains high. As the chart [...]

The unemployment rate in the European Monetary Union stayed put at 11.5% in August. The unemployment rate for the broader European Union fell slightly to 10.1% in August from 10.2% in July. Unemployment remains high. As the chart reminds us, there is a tremendous difference between the unemployment rate for the monetary union as a whole and for its individual members, especially Germany. This is wonderful news against the backdrop of declining economic activity. But can it last?

The unemployment rate in the European Monetary Union stayed put at 11.5% in August. The unemployment rate for the broader European Union fell slightly to 10.1% in August from 10.2% in July. Unemployment remains high. As the chart reminds us, there is a tremendous difference between the unemployment rate for the monetary union as a whole and for its individual members, especially Germany. This is wonderful news against the backdrop of declining economic activity. But can it last?

We can calculate the unemployment differences among European members to get an idea of how disparate conditions are right now compared to history. Back to 1998, the aggregate absolute value differences of member unemployment rates from the zone's average has been larger than this only about 13% of the time. All those episodes were in this cycle. Progress is being made to reduce unemployment rate differences, but it is being made very slowly. And the extreme differences among members' labor market conditions pose a real policy problem for Europe.

The latest data showed the unemployment rate fell for six of the 11 countries in the table, but not by enough to impact the aggregate EMU unemployment rate. Still, the overriding picture that we get is of ongoing labor market improvement, despite the recent spotty and weakening macroeconomic data.

Over three months, of the 11 countries in the table, all but three showed a drop in their respective unemployment rates over three months and only one showed an unemployment rate increase over that period. That one country was France.

Over six months, seven out of 11 countries showed declines in their respective rates of unemployment, while four showed increases. The countries showing increases over six months are Belgium, Finland, France and Luxembourg.

Over 12 months, seven countries show declines in their respective rates of unemployment, while three show increases and one shows no change.

It is both interesting and significant that unemployment rates continue to work lower even in this period when economic data have been mostly disappointing and activity has been eroding. For the EMU as a whole, the unemployment rate has declined by 0.5 percentage points over 12 months, by 0.2 percentage points over six months and by 0.1 percentage points over three months. If you annualize that progress, it has been relatively steady.

Unemployment conditions continue to be difficult and the newest readings on inflation continue to show inflation working down to lower levels. This is not an encouraging development and it indicates that the ECB's policies have not taken hold. We reported earlier with the release of the monetary and credit data that credit growth, a variable directly targeted by the new ECB policy, is not being stimulated by the ECB's special program. The growth of private credit continues to be negative.

As the charts clearly show Germany is in a different world from the rest of the monetary union and its representative to the ECB continues to be opposed to some of the more expansive activities that the ECB has been considering. It is far from clear that monetary policy is the right tool to stimulate Europe, and there is a division of opinion on how to use monetary policy as well.

The ECB's negative interest rates don't seem to be having a big impact and its target on private credit growth has it to bear fruit. In one of his recent messages, Mario Draghi urged countries to find a way to create stimulus within the confines of their budget restrictions. Even when the ECB president tries to urge some kind of fiscal action, he has to be mindful of the constraints on credit that bind actions of European governments.

Europe still faces geopolitical risk and a continuing warzone on its doorstep even as it is running out of macroeconomic policy options. So far, the backtracking in activity has spared the unemployment rate. But unemployment lags. If that rate should start to rise, Europe will find itself between a rock and very hard place and with most of its policy options already played out.

Is there a lesson here for the Fed that has kept its stimulus policies going full tilt even as the economy has grown? If U.S. growth should run into trouble, what would the Fed do?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief