Global| Mar 28 2014

Global| Mar 28 2014Europe Continues to Make Progress

Summary

The European Union continues to make smart gains in March with its overall index of sentiment up by 1.2 percentage points. For the broader EU, the overall sentiment index has risen to 105.3 in March from 105 in February. EU industrial [...]

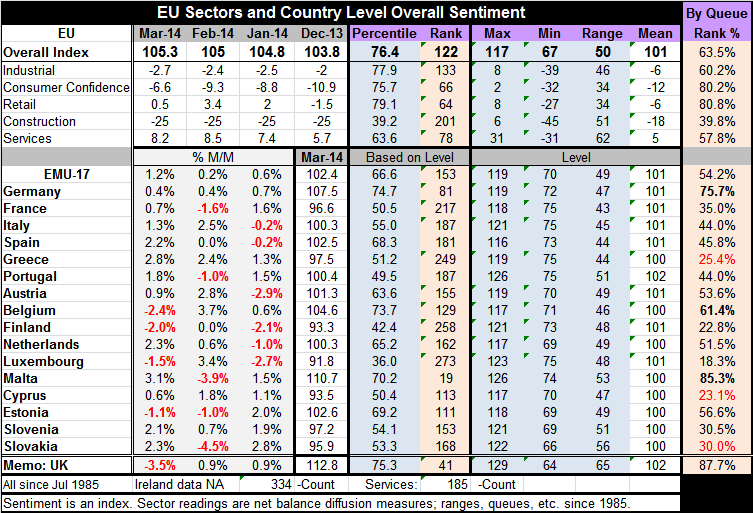

The European Union continues to make smart gains in March with its overall index of sentiment up by 1.2 percentage points. For the broader EU, the overall sentiment index has risen to 105.3 in March from 105 in February.

The European Union continues to make smart gains in March with its overall index of sentiment up by 1.2 percentage points. For the broader EU, the overall sentiment index has risen to 105.3 in March from 105 in February.

EU industrial confidence continues to churn out a raw negative reading that slipped slightly to -2.7 in March from -2.4 in February. Consumer sentiment also has a negative reading of -6.6; nonetheless, improving from -9.3 in February. Retailing that had a stronger positive reading of February at a +3.4, a stepped back to a positive reading of +0.5. Construction has stayed steady at a -25 reading in both February and March. The services sector has also backed off with the reading of +8.2, down slightly from its 8.5 reading in February.

Across the 16 members of the European Monetary Union that reported the data for February, only four show declines in their sentiment indices for March. That list includes Belgium and Finland, followed by Luxembourg and Estonia. There were five such declines in February and six such declines in January.

The EMU is making some clear and steady gains; however, it's important to recognize that there is still a long way to go and a great deal of variation within the Community. I will repeat that several times in different ways in this essay. For example, Germany and Malta have the highest standings of their sentiment indices, Malta's being in the 85th percentile of its historic queue and Germany's being in the 75th percentile of its historic queue. The EMU-wide number is in the 54th percentile of its historic queue. On the low side we have Portugal in its 25th percentile, Cyprus in its 23rd percentile, Slovakia in its 30th percentile, Slovenia in its 30th percentile, Luxembourg in its 18th percentile, and so on. Among large countries, France lags sitting in its 35th percentile with Italy in its 44th percentile and Spain in its 45th percentile. The second third and fourth largest economies in EMU have percentile standings that are leagues away from the percentile standing of the largest economy, Germany. How is that working? Lest you think Germany is a locomotive pulling in imports, Germany has the largest current account surplus in the world. That's how that is working: not at all.

If we assess Europe by using the sentiment standings for this group of countries, we find that the current divergence among the sentiment indicators is relatively large. Divergence has been greater than it is right now, only about 40% of the time. While there is some small movement toward convergence over the last year or so (from some very divergent levels), the current standing is showing above normal divergence. This is going to be a problem, not just for policymaking at the European Central Bank but also because the political pressures are going to arise within the EMU as countries that are doing poorly are going to want to grow faster but these are generally countries that have developed competitiveness issues and are going to need to retain austerity, fiscal discipline and to continue to feel pain and to lag behind the other more prosperous countries. They will not get much assistance because there is no fiscal union within the EMU.

Looking at just the large countries, there is a considerable difference in the performance of industry with Germany's sector residing in the 76th percentile of its queue compared with the 48th percentile standing for France, the 45th percentile for Italy and the 38th percentile standing for Spain. The German industrial sector is clearly in the best shape of the EMU; that's no surprise.

Consumer confidence also shows some substantial differences within the EMU. Germany leads with a percentile standing for confidence in the 87th percentile followed by Spain despite its unemployment problems; Spain stands in the 73rd percentile of tis queue. Italy is in the 55th percentile and France in the 37th percentile. By comparison, countries like Greece and Portugal are in the 18th and 43rd percentiles, respectively. There is a great deal of variation within this measure across countries. Progress, however, is occurring on a broad front. From December of last year to March, all of the largest economies are showing improvement. Germany's confidence index has increased by five points on the scale, but Italy, Spain, and Portugal have seen increases at just as big or bigger. France is also showing progress, but has seen its confidence indicator increase by only two points on this timeframe even though its level is lagging the rest of the union quite badly.

Spain's retail confidence is the highest among large countries, standing the top 2% of its historic queue. Germany's confidence is in the top 6% of its historic queue, but that's followed by Italy which is only in the top 42% and by France which is in the bottom 36% of its historic queue.

There seems to be bit more consistency and less of identity crisis in Europe's services sector. Services confidence is not truly high in any of the large EMU members. Germany's services confidence is a 60th percentile standing; that's followed by Portugal at the 56th percentile, Greece in the 46 percentile, and Italy in the 43rd percentile. Spain trails in the 40th percentile while France, as has been the case for a number of indicators, lags of the standing in the 21st percentile. However, unlike other categories, none of these readings is particularly good. As is the case with the US services sector, in Europe services just are not getting in gear. Since the services sector is where most of the jobs are since it is a low productivity sector, job growth has continued to lag in Europe as well as in the United States. In part because we are all in the same world war, we all experienced the same sort of baby-boom and so we're all experiencing the same sort of demographic draft that's having some impact on job growth and on labor force growth. However, the services sector is a special case in finding that recovery in the wake of recession is more difficult to attain than in the past.

Warning: Europe continues to make progress. Reports on Europe are very clear on this, but I would urge as I do with the US statistics not to be complacent about the fact that growth is in hand and has been so for some time. In the US, growth has been entrenched for much longer. Consumer confidence, for example, is weaker relative than to its history in the US than it is in most places in Europe. The economies simply are little more fragile than they used to be because unemployment rates are high and the services sectors are churning out less growth than they used to in the past. The outsourcing of jobs to cheaper wage countries in Asia, largely China, has taken a toll, not only only by absorbing manufacturing jobs, but by commandeering and redirecting the multiplier effect it would have created across the services sector. In addition, the development of computers and specialized software has helped to eliminate the need for labor and for lower-skilled labor on a broad front.

I would not say that our dislocation is as severe as it was in the industrial revolution, but there is substantial dislocation in train and it's creating, political instabilities and challenging political identities. As is often the case when economic times get bad, countries will sometimes seek international distractions to take people's minds off of the depressing conditions at home. I won't claim that's the whole reason for the expansionist actions in China and in Russia, but it's certainly part of the explanation. In turn these sorts of destabilizing geopolitical events have great negative blowback to the real economy. In this case, since the real economy is not strong, this sort of repercussion is more dangerous. And it can become even more dangerous if the tensions escalate.

So while growth is picking up, let's not lose sight of the fact that globally consumer confidence is still impaired. Within Europe, there is a great deal of variation in the performance of countries that are locked into a single currency union without an agreement to smooth out the effects of the business cycle on internal conditions even when they fall differentially across the union. Let's remember that the banking sectors are still weak and may actually be weakened further as regulators try to impose new rules on them to make them stronger in the future. And at the same time, let's try not to be too depressed and let's increase growth! The latter, of course, is a pretty tall order given all of the former. Europe, it seems, is going to try to stick to its metrics on fiscal prudence as it tries to post recovery. This will probably increase tensions within the economic union. In the US, there is a great deal of pressure to make some progress on the out year fiscal deficits that are projected. Even though US fiscal drag is expected to be relieved over the next year or so, there is a longer-term need to corral the deficits implied by current government promises and programs. Fiscal activity is not likely to be really pro-growth because it has already overshot its prudent mark by so much.

And central bankers' worries are... Amid all of these trends in facts and concerns we have central bankers worried about what has been extra stimulative action that has been taken during, and in the wake of, the financial crisis. I can understand being worried about the blowing up the balance sheets of the central banks. I understand the concern that someday this may come back to haunt us. However, the current circumstances, it seems to me, to argue that "someday" is a long ways away. The continuing low level of inflation is a hallmark of this continuing downward pressure on prices form weak growth and weak demand. Stubbornly high unemployment is another trapping of this circumstance as is the slowdown in job growth. People will continue to argue about the impact of labor market dynamics including falling labor force participation rates, but it seems to me that conditions of `scarce labor' are hardly upon us, especially if you take a global view and look at how multinational corporations have been developing labor resources around the world.

Having said that, let me return to my initial theme, which is that Europe is recovering but its recovery is uneven and has its risks. This is not just a phrase that I repeat over and over again when different reports show themselves. This is a theme that continues to emerge as economic data reveal themselves. And if nothing else the continued low levels of consumer confidence should convince you that substantial risk is still right around the corner.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.