Global| Mar 03 2006

Global| Mar 03 2006Euro-zone Growth Eases to 0.3% in Q4

Summary

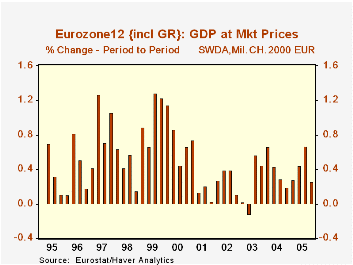

GDP growth in the Euro-Zone slowed in Q4 to 0.3% from 0.7% in Q3, according to the first full breakdown of Q4 data published this morning by Eurostat. These real growth rates are quoted in chained 2000 euros, adopted as the pricing [...]

GDP growth in the Euro-Zone slowed in Q4 to 0.3% from 0.7% in Q3, according to the first full breakdown of Q4 data published this morning by Eurostat. These real growth rates are quoted in chained 2000 euros, adopted as the pricing methodology by Eurostat just three months ago.

Several major expenditure components of GDP contributed to the lower growth; most notably, private consumption fell outright by 0.2% and was up a sluggish 0.8% from a year ago. This was among the smallest year-on-year increases in the 10-year history of the data calculated on this basis. However, as we noted here yesterday, retail trade, at least in Germany, turned up sharply in January; perhaps this is a precursor to a better performance for consumer spending in general this quarter.

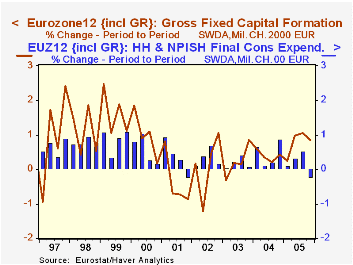

Fixed capital formation moderated to a 0.8% gain in Q4 from 1.1% in Q3. This is still a respectable performance and brought the year to 2.2%, the strongest gain since the tech slowdown began in 2000.

Net exports decreased, encompassing smaller gains in both exports and imports. As with investment, though, the Q4 result followed much stronger outcomes in Q2 and Q3, so can hardly be characterized as "weak" in a broader context. Indeed, observers, including ourselves have noted repeatedly that the export sector is a main support to the European economies at present.

So 2005 ended at a slow pace in Europe. But as mentioned above, retail trade showed some life in Germany already in January, and sentiment surveys have also improved. The Olympics may even give some boost to this quarter's performance. The ECB policymakers must believe gains of that sort will take hold, as they raised their key interest rates yesterday for the second time in three months. M. Trichet's announcement in fact indicated a concern that recently improved economic activity would threaten inflation, which is already hovering above the desired 2% pace.

| EuroZone12: GDP (Chained 2000 Euros) |

Q3 2005 | Q3 2005 | Q2 2005 | Q4 2004 (yr/yr*) | Yearly Totals*|||

|---|---|---|---|---|---|---|---|

| 2005 | 2004 | 2003 | |||||

| GDP | 0.3 | 0.7 | 0.4 | 1.3 | 1.3 | 2.1 | 0.7 |

| Final Private Consumption | -0.2 | 0.5 | 0.3 | 0.8 | 1.3 | 1.5 | 1.0 |

| Gross Fixed Capital Formation | 0.8 | 1.1 | 1.0 | 2.2 | 2.1 | 2.3 | 0.8 |

| Exports | 0.5 | 3.4 | 2.0 | 4.6 | 3.8 | 6.5 | 1.1 |

| -Imports | 0.9 | 3.1 | 2.3 | 4.5 | 4.5 | 6.6 | 2.9 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief