Global| Sep 30 2016

Global| Sep 30 2016Euro Area Unemployment Rate Is Locked at 10.1%; Meanwhile, Inflation Is Starting to Percolate and Other Issues Are [...]

Summary

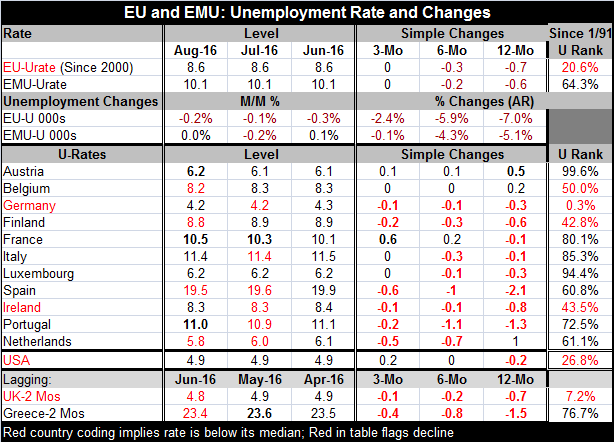

Fresh unemployment and inflation data are out for the EMU area. Inflation is starting to creep up as the impact of stable then rising oil prices is taking a toll. But the unemployment rate has been stuck for both the EU and the EMU [...]

Fresh unemployment and inflation data are out for the EMU area. Inflation is starting to creep up as the impact of stable then rising oil prices is taking a toll. But the unemployment rate has been stuck for both the EU and the EMU for the last few months (four for the EU, five for the EMU).

Fresh unemployment and inflation data are out for the EMU area. Inflation is starting to creep up as the impact of stable then rising oil prices is taking a toll. But the unemployment rate has been stuck for both the EU and the EMU for the last few months (four for the EU, five for the EMU).

No Phillips Curve

Since 2009, the Phillips curve relationship has been nonexistent. That curve plots the tradeoff between inflation and unemployment. It is widely believed by economists to be a valid short-term tradeoff but not to be a tradeoff at all in the long run. However, for the EMU even in the short runs, there has been no evidence of any unemployment/inflation tradeoff. Unemployment and inflation rates both have fluctuated in about a 3.5 percentage point range with little or no evidence of correlation since January 2009.

Internal disconnections

There have been pronounced differences in the behavior of unemployment rates within the EMU even though all the EMU countries (and we are looking only at the original members plus Greece here) are in the same currency union and face the exact same monetary policies. They also have the same rule structure. Yet, the behavior of national unemployment rates and to a lesser degree, inflation rates, has been very different across countries. That is pretty clear evidence that even after all this time European integration has not been working very well. At the same time, other issues have arisen that have driven a wedge between EU and EMU members. We are hearing much less talk these days about how 'we are all European.'

Germany wins at the expense of other members

During this period of EMU development, Germany's unemployment rate has fallen and reached a post-unification low. This is not news- it has been so for a while. The German unemployment rate is at 4.2% for the last two months and was at 4.3% for the previous five months. When we compare Germany to the other original EMU members, we find that the German unemployment rate is negatively correlated with every other original member of the EMU except Belgium. Calculated on data since 2003, Germany has generally seen its unemployment rate move contrarily to other members. As the German economy has improved, the rest of the EMU has generally deteriorated in relative terms at least in terms of labor market performance.

Recently (and fortunately), that has changed.

The current state of heterogeneity

The standard deviation of unemployment rates across the original EMU members peaked in May 2013 and it has gradually been coming down as smaller differences are now generally being recorded. Previously, unemployment rate differences were dissipating steadily from at least 1993 through late-2007 until the global recession and financial crisis struck. Then from late-2007 through May 2013, the EMU saw massive differences erupt between the unemployment rates of its various members. Currently, the level of unevenness is only back to where it was in August 2011, a time when cross country differences were still getting wider at a rapid rate. The degree of divergence among the original EMU members' unemployment rates has been higher than it is today only about one-third of the time since January 2009.

Unemployment reduction progress

Still, there is plenty of progress afoot on unemployment rate reduction. Of the 11 countries listed in the table, all but two have unemployment rates lower over 12-months; nine have unemployment rates lower over six-months with one having its unemployment rate unchanged. Over three-months, six nations post lower rates of unemployment, three post rates that are unchanged, and one, Austria, logs an increase.

Unemployment rate levels are still stuck at a high level...for most

However, to assess the state of unemployment, we also rank the levels of the respective unemployment rates for members since 1991. On this basis, only Germany has a really low rate, the lowest since German reunification. Beside Germany, only Finland and Ireland have unemployment rates below their respective medians for the period. Belgium is on top of its historic median. For the remaining seven nations, the average queue ranking of their respective rates of national unemployment resides at the 79th percentile. That is, for the rest of euro area's original members, the unemployment rate today has only been higher historically only about 21% of the time (the median rate calculation is similar at the 80th percentile).

Inflation stopped falling

Meanwhile, inflation in the EMU has stopped falling. As of August, inflation is only negative year-over-year for Italy, Luxembourg, and Spain. Year-on-year inflation is highest in Belgium and Portugal. Still, the community has been much more successful in attacking inflation on a monetary union wide basis than in reducing or harmonizing unemployment rates. Ranked since the year 2000, the standard deviation among the various country area HICPs has been smaller only about 2% of the time.

The revealed preference of policy

Obviously, we can conclude that inflation and inflation harmonization has been much more of a priority in the EMU than has been unemployment rate reduction and unemployment harmonization. And the costs of inflation reduction and harmonization have fallen very unevenly across the euro area.

Backlash

It should not be surprising that this sort of choice and its associated costs have produced a backlash. As much as economists like to see inflation harmonization, and as much as it gives the central bank a clearer decision on what monetary policy should do, the EMU, at the same time, has achieved those goals at the cost of deviating from the objective that the people would place the greater weight on, reducing unemployment.

Brexit was another 'cost'

While the U.K. has never part of the common currency area as EU rules became more binding and stifling, it opted out of the EU with its now famous Brexit vote. For the U.K., the final straw was related to the migrant crisis and its loss of control over its own borders. But there are different issues that bind most for different member nations.

What's next?

Banking problems in Cyprus caused the EU to adopt a bank bail-in law that caught the entire Italian banking system on the wrong side of the fence. Much earlier with problems in Greece, France and Germany had eased the pain of their national banks with public funds, but Italy has had a worse deficit problem and had not had the where-with-all to fix its banks. So when the 'Cyprus rules' were adopted, Italy was left on the outside with an undercapitalized banking system that could no longer be 'bailed out' with government monies under the new rules (not that Italy had those funds to expend). But now Germany's Deutsche Bank is under pressure. The U.S. is threatening a huge fine for its mis-selling of mortgages. And it is feared that this fine would be just too crippling for the bank at a time banks are being forced to carry more capital. Customers, especially hedge funds, are reducing exposure to Deutsche Bank. Germany is left with a dilemma and basically this puts it in the same position vis-a-vis Deutsche Bank that Italy is in with its banking system. Angela Merkel has tried to stay distant from the problem, but overnight the Asian stock markets were in turmoil over the condition of Deutsche Bank whose share value fell at one point by 8%.

An exception for the goose is an exception for the gander

If Germany breaks the 'Cyprus rule' on banking bailouts, it will free Italy to do the same and maybe even mobilize more funds to help Italian banks and possibly set new precedents across the euro area ( to say nothing of the fact that it would rile Cyprus). It is inconceivable that Germany would let Deutsche Bank fail (suffer a 'bail-in'). Of course, the Deutsche Bank CEO claims that these fears are exaggerated. Yet, the market pressures on Deutsche Bank are real and must be dealt with.

EMU at the crossroads?

This will be an interesting case study for the EMU. It is clear that Germany has been able to commandeer the EMU and mold it into a situation in which Germany could prosper. From the very beginning, Germany understood the rules and how they would work as the rest of the EMU largely did not. Once crisis hit, Germany made members in violation of debt rules to toe the line, and despite deteriorated economic conditions, several were forced to adopt formal austerity programs or to limit public sector activity even during weak economic times. The upshot has been that Germany has been running one of the largest current account surpluses relative to GDP in the world (by itself an objectionable act under EU principles) and doing nothing to remedy it. Germany has cherry-picked the rules it wants to obey and fore obedience on fellow members. Germany is also growing more solidly than any other member country with the best fiscal position and is the most competitive economy in the EMU. Its unemployment rate has fallen lower than anyone else's and is lower relative to its historic standards than any other country in the EMU by a long shot. The euro area rules clearly were optimized for Germans. And this success is now becoming a problem for Germany. Angela Merkel's insistence on letting migrants in has proved to be one step too much of German leadership. It has created lots of internal tensions and reactions and it, more than anything else, is responsible for the U.K. Brexit. It will become a bigger problem when Germany is forced to lead in the EU without the counter weight of the U.K. when the Brexit is completed. All of this makes Germany's response to the Deutsche Bank issue more and more interesting. It is right now the most interesting and dangerous thing going on in Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief