Global| Aug 31 2016

Global| Aug 31 2016Euro Area Unemployment Rate Is Flat

Summary

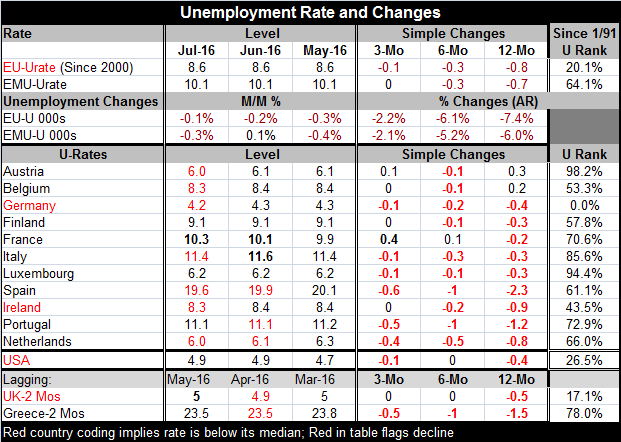

Despite the unchanged rate of unemployment in the EU and EMU in July, there are still a lot of unemployment changes occurring in the member countries. In July, seven of eleven early reporting EMU member countries had declines posted [...]

Despite the unchanged rate of unemployment in the EU and EMU in July, there are still a lot of unemployment changes occurring in the member countries. In July, seven of eleven early reporting EMU member countries had declines posted in their unemployment rate. Only one, France, logged an increase. But that is a problem. As the second largest economy in the euro area, France is moving in the opposite direction to other countries in the EMU and that could become a policy problem for France as well as for euro area policymaking. France saw its unemployment rate climb by 0.2 percentage points in July and it is up by 0.4 percentage points over three months as well (but it is lower year-over-year).

Despite the unchanged rate of unemployment in the EU and EMU in July, there are still a lot of unemployment changes occurring in the member countries. In July, seven of eleven early reporting EMU member countries had declines posted in their unemployment rate. Only one, France, logged an increase. But that is a problem. As the second largest economy in the euro area, France is moving in the opposite direction to other countries in the EMU and that could become a policy problem for France as well as for euro area policymaking. France saw its unemployment rate climb by 0.2 percentage points in July and it is up by 0.4 percentage points over three months as well (but it is lower year-over-year).

There is still great irregularity in the level of the unemployment rates by country in the EMU. Calculated back to 1993, the dispersion of unemployment rates now ranks as having been greater only about 20% of the time. The dispersion is coming down from its peak in May 2013, but it is coming down slowly.

Germany continues to post a reunification low in its unemployment rate while Luxembourg and Austria have unemployment rates which, although being numerically moderate, have been higher since 1991 less than 5% of the time. Greece's (lagging) unemployment rate has been higher only 22% of the time. Portugal's rate has been higher 28% of the time and Italy's has been higher only 15% of the time. In the EMU, only Germany and Ireland have unemployment rates in July that are below their respective medians (calculated back to 1991). The U.S. and the U.K. also have unemployment rates that are below their respective medians and by a good margin.

Unemployment rates in the EMU are lower in nine of eleven countries year-over-year. That is impressive; 10 are lower over six months and six are lower over three months. Progress in the reduction of unemployment still appears to be in train.

However, on a slightly different front, the rate of reduction in the number of persons unemployed in both the EU and EMU regions is slowing down. Over 12 months, the number unemployed fell in the EU by 7.4% and it fell in the EMU by 6%. Over six months, the pace of decline in EU fell to -6.1% while the pace in the EMU fell to -5.2%. Over three months, the annual rate pace of reduction in the ranks of the unemployed has slowed to -2.2% in the EU and to -2.1% in the EMU. While unemployment rates are still falling, the speed of the reduction in unemployment appears to be slowing down.

Also released today was the early reading on EMU inflation. The EMU-wide HICP was flat in August and up by 0.2% over 12 months. The core rate also was flat and it is up by 0.7% over 12 months. Among the largest EMU member economies, inflation was flat in Germany, down by 0.1% in France and up by 0.1% in Italy and in Spain - all on a month-to-month basis. Inflation rates are positive in the Big Four economies over three months with gains under 1% annualized in Germany and France, a rise at a 1.2% annual rate in Italy, and at a 1.8% annual rate in Spain. Over 12 months, the HICP pace is at 0.3% in Germany, at 0.4% in France, flat in Italy, and falling by 0.3% in Spain despite its three-month pick-up.

Inflation is still under wraps in Europe. And policy is still geared for stimulus. Unemployment rates remain unusually high and in need of ongoing repair. Global growth is weak and as the ECB and BOJ in Japan are struggling for stimulus and as China's economy is still in some chaos as it tries to reorient itself and as the Fed is taking steps toward a hike rates. Those steps are pushing the dollar to a one-month high and causing the U.S. 10-year treasury note to have its largest rise in yield in over one month in about one year. Global policy is set to diverge even more in a month or so if the Fed stays on this path. Meanwhile, at least one Fed official (Evans) is talking about how rates are going to stay unusually low (no numbers just that descriptive phrase) and another (Rosengren) is playing the financial stability card and pushing for higher rates. Private sector investor Bill Gross is bashing the Fed for keeping rates so low for long. The Fed is under enormous pressures. Inflation in the U.S. does look much different than in looks in Europe. But the Fed is under scrutiny and there is pressure to get rates moving up despite spotty economic progress.

The international situation seems about to get more interesting in the coming months. But as that happens, we see creeping inflation in the euro area and unemployment progress that is slowing down. These are not altogether signs that are welcome. In Japan, there is tough talk but little sign of any real economic or inflation progress. China also seems to be spinning its wheels and with more problems cropping up by the minute from pollution to a heavier load of debt as the economy continues to underperform.

Sometimes it is hard to understand what central bankers really think they are doing. In Europe, there are hints that fiscal policy help is needed and without it monetary policy may have to go even farther overboard. In the U.S., there is greater likelihood of fiscal spending but not until after the elections. All in all, 2016's roller cost ride may not yet be over. We still may be in the car cranking to go up the big first hill. The most thrilling part of the ride may yet lie ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.