Global| Aug 12 2016

Global| Aug 12 2016Euro Area, U.K. and U.S. GDP Trends Muddle Through

Summary

While U.S. GDP growth has dropped off a cliff, growth in the EMU and the U.K. is more or less mid-range since end-2009. In 2016 Q2 quarterly growth is decelerating in the EMU and in five of nine of the original EMU member GDP [...]

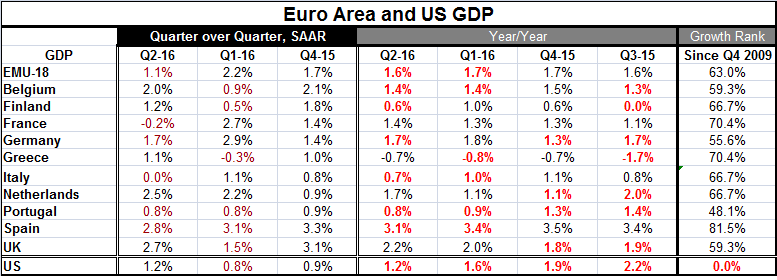

While U.S. GDP growth has dropped off a cliff, growth in the EMU and the U.K. is more or less mid-range since end-2009. In 2016 Q2 quarterly growth is decelerating in the EMU and in five of nine of the original EMU member GDP reporters in the table. Year-over-year EMU GDP growth is decelerating and GDP is decelerating in 6 of the 10 reporting EMU members in the table.

While U.S. GDP growth has dropped off a cliff, growth in the EMU and the U.K. is more or less mid-range since end-2009. In 2016 Q2 quarterly growth is decelerating in the EMU and in five of nine of the original EMU member GDP reporters in the table. Year-over-year EMU GDP growth is decelerating and GDP is decelerating in 6 of the 10 reporting EMU members in the table.

Growth in a word: moderation; in two words: moderation and deceleration

For the EMU as a whole, the Q2 year-on-year GDP growth rate ranks in the 63rd percentile over the last 27 quarters back to Q4 2009. Greece and France have growth rates of GDP that rank in their respective 70th percentiles. Spain's growth ranks in its 81st percentile. Portugal's growth ranks in its 48th percentile and Germany's ranks in its 55th percentile. Growth across the euro zone is overwhelmingly moderate by recent standards. At 2.2%, the second highest year-on-year growth rate in the table for Q2, U.K. growth stands weakly in its 59th percentile. At a 1.2% year-on-year pace, the U.S. is logging its weakest pace since at least Q4 2009.

European IP rebounds in June but logs Q2 swoon

Although industrial output ended Q2 with a bang rising by 0.6% in June after shedding 1.1% in May, IP on balance contracted in Q2 across the EMU. By sector, there were quarterly contractions in output for consumer goods, intermediate goods, and capital goods.

For the same group of countries minus Belgium (that has not reported June IP yet, and adding Luxemburg and Ireland), production is lower in Q2 for Germany, France, Italy, Luxembourg and Ireland. In June alone, IP fell in four of these 10 reporting countries with IP drops in France, Italy, Spain and Luxembourg. The U.K. has gone its own way with IP up at a strong 7.4% annual rate in Q2 but with declines in output in each of the last two months.

China update is no encouraging

China reported out economic data today and its results are disappointing. Chinese industrial output grew by just 6% year-on-year in July, even weaker than June's 6.2% pace. Retail sales grew at a 10.2% pace, less than June's 10.6% pace and less than expected. Fixed asset investment also lagged, growing at an 8.1% pace compared to a 9% pace from January to June. China is not signaling that the coast is clear from its ongoing slowdown- far from it.

Just like the Starship Enterprise...

While the U.S. stock markets' major averages were poking up to all-time highs yesterday, we clearly have an environment where the investment markets are detaching from the real sector. Like when the disc of the Starship Enterprise detaches from the rest of the ship, the result is something that is rather off putting. While we are accustomed to looking at markets and making judgements about the economy from their performance (and vice versa), in this case the strange days for investment markets are no longer clearly attached to an underlying economic framework. Monetary authorities are using interest rates as levers to try to pry growth from the real economy; so far it has not really worked. Low interest rates and bond yields are so unrewarding- negative yields in many cases- that investors have been pushing more aggressively into riskier asset classes, like stocks, pressuring prices.

Jurassic World

But at this level of interest rates, who is to say which asset class is now more risky? We can easily conclude that markets no longer give us valid signals about the economy. So don't get excites about growth prospects after seeing stock market performance. The markets and the economies are no longer very closely connected. It's a new world out there and in some ways it makes Jurassic World look safe. Whether you are hybridizing dinosaurs, mortgage securities or engaged in heretofore unseen monetary tactics, you are traveling on an unworn path. Beware.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief