Global| Jun 15 2016

Global| Jun 15 2016Euro Area Trade Surplus Jumps Sharply

Summary

Trade in the EMU remains somewhat enigmatic. Exports and imports (of manufactured goods) are still quite soft over 12 months as well as over six months. But over the recent three months, exports have exploded to life as imports have [...]

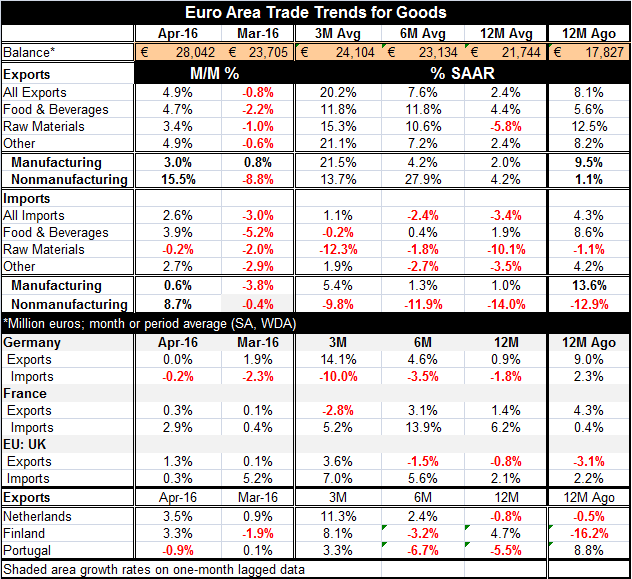

Trade in the EMU remains somewhat enigmatic. Exports and imports (of manufactured goods) are still quite soft over 12 months as well as over six months. But over the recent three months, exports have exploded to life as imports have remained listless. This combination of events has pushed the trade surplus into new record territory as the trade surplus jumped sharply to stand at 28 billion euros in April, up from 23.7 billion euros in March. There have only been four monthly improvements in the trade deficit larger than this one on data back to 1999.

Trade in the EMU remains somewhat enigmatic. Exports and imports (of manufactured goods) are still quite soft over 12 months as well as over six months. But over the recent three months, exports have exploded to life as imports have remained listless. This combination of events has pushed the trade surplus into new record territory as the trade surplus jumped sharply to stand at 28 billion euros in April, up from 23.7 billion euros in March. There have only been four monthly improvements in the trade deficit larger than this one on data back to 1999.

In April, EMU exports gained 4.9% after falling by 0.8% in March. The three-month growth rate of exports (annualized) is up to 20.2%. Much of the export jump in April is in nonmanufacturing where exports jumped by 15.5% in the month as manufacturing exports rose by 3%. Still, over three months, manufacturing exports are up at a 21.5% pace with nonmanufacturing exports up at a 13.7% pace. Manufacturing exports are up by a weak 4.2% over six months and by only 2% over 12 months.

Imports, however, show little sign of life. They rose by 2.6% in April after falling by 3% in March. Imports of manufactured goods gained 0.6% in April after falling by 3.8% in March. Nonmanufacturing imports rose by 8.7% in April after slipping by 0.4% in March. Manufacturing imports are up at an annual rate of 5.4% over three months, compared to 1.3% over six months and 1% over 12 months. Nonmanufacturing imports are contracting on all these horizons. Imports give us a picture of ongoing weak domestic demand in the EMU.

EMU imports continue weak while exports have found some life, possibly because the weak euro is helping. But the notion of strength is a recent one and ongoing lethargy in imports is a disappointment.

Germany, France and the U.K.

Germany shows a similar overall pattern with exports that have accelerated. They are up weakly over 12 months (0.9%) but are advancing over three months at a 14.1% annualized pace. France is contrary with exports slipping at a 2.8% pace over three months and up by only 1.4% over 12 months. French imports are steady or stronger at a 5% pace at least on all horizons. The U.K. shows falling exports over 12 months and six months with a three-month pace showing growth at a 3.6% annual rate. U.K. imports are up by 2.1% over 12 months and gradually increase their pace on shorter horizons. The U.K. shows the presence of some domestic demand.

The Netherlands, Finland and Portugal

The Netherlands, Finland and Portugal are relatively early trade-flow reporters. They show exports weak over 12 months and over six months with at least some acceleration over three months. Dutch exports are up at an 11.3% annual rate over three months.

Soaking up external domestic demand

The EMU is benefitting from a weak euro that improves its competitiveness. It is one thing that the low or negative interest rate policy can do - even though that tact has failed in Japan. The EMU also is benefitting from a huge trade surplus which effectively causes it to benefit from domestic demand in other places in the world as it sells more than it buys. The EMU purchases from abroad (imports) continue to be very weak. We will want to track this pick up in exports to see if it can sustain this sort of life. The Baltic Dry Goods index is still giving off weak signals. It hardly seems as though global trade has turned around, but oil prices have recovered and will help to improve nominal trade flows.

China is living on the edge

China is continuing to ramp up its domestic public works spending and is driving growth with debt. China's debt mountain is getting huge. At some point, this strategy of relying so heavily on debt to sustain investment especially as private investment has not been forthcoming will have a backlash. China may not be a capitalistic country, but that does not repeal the laws of economics for it. An excessive reliance on debt will have consequences.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief