Global| Oct 16 2014

Global| Oct 16 2014Euro Area Trade Surplus Gets Bigger as EA Gets Weaker

Summary

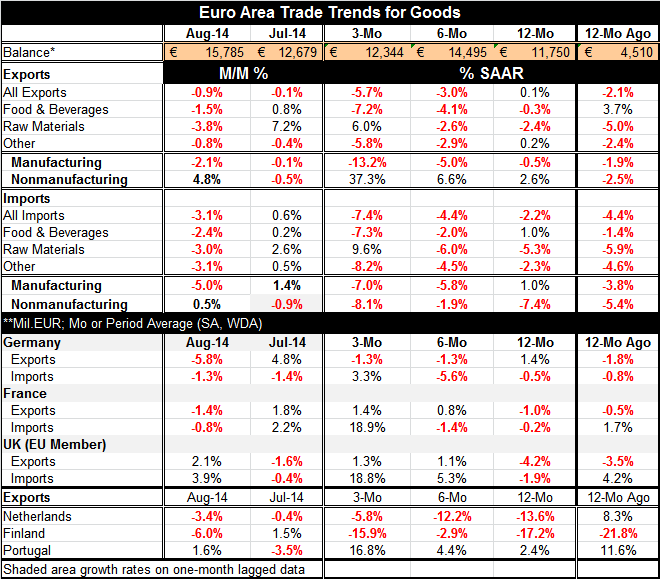

The trade surplus in the European Monetary Union moved sharply higher in August at 15.8 billion euros compared to 12.7 billion euros in July. Imports won the race to the bottom as they fell by 3.1% in August, outpacing exports that [...]

The trade surplus in the European Monetary Union moved sharply higher in August at 15.8 billion euros compared to 12.7 billion euros in July. Imports won the race to the bottom as they fell by 3.1% in August, outpacing exports that fell by only 0.9%. The concerns about growth that are alive and well in financial markets will not find such weakness in European imports as a good sign. Of course, the larger surplus will add to GDP growth. But this is the paradox of the trade account. A bigger surplus does augment GDP. However, such weak imports suggest that underlying GDP is extremely weak. It may be that focusing on the impact of the trade surplus on GDP is the wrong way to go. Imports may be telling us that the underlying trend for GDP has worsened and that the trade surplus will only be a mitigating factor to a bad result.

The trade surplus in the European Monetary Union moved sharply higher in August at 15.8 billion euros compared to 12.7 billion euros in July. Imports won the race to the bottom as they fell by 3.1% in August, outpacing exports that fell by only 0.9%. The concerns about growth that are alive and well in financial markets will not find such weakness in European imports as a good sign. Of course, the larger surplus will add to GDP growth. But this is the paradox of the trade account. A bigger surplus does augment GDP. However, such weak imports suggest that underlying GDP is extremely weak. It may be that focusing on the impact of the trade surplus on GDP is the wrong way to go. Imports may be telling us that the underlying trend for GDP has worsened and that the trade surplus will only be a mitigating factor to a bad result.

We see this in the trend for imports that are down by 2.2% over 12 months, falling at a 4.4% pace over six months and falling at a 7.4% pace over three months. Imports are getting progressively weaker.

Exports are getting progressively weaker as well. And that's not a good sign, either. Exports are up by 0.1% over 12 months, falling at a 3% annual rate over six months and falling at a 5.7% pace over three months.

Turning back to imports, we see substantial weakness in both manufacturing and nonmanufacturing imports. While in August the patterns are somewhat mixed as manufacturing imports are falling by 5% and nonmanufacturing imports are rising by 0.5%. Over three months, we have both of these flows falling at a substantial pace; manufacturing imports are falling at a 7% pace and nonmanufacturing imports are falling at 8.1% pace. Manufacturing imports show progressively weaker growth rates. For nonmanufacturing, the pattern isn't clear but the current three-month growth rates are weaker than they are over either six months or 12 months.

Looking at exports, we see that manufacturing exports fell by 2.1% in August while nonmanufacturing exports rose by 4.8%. And that's in August alone. We have very different patterns for exports as between manufactured and nonmanufacturing flows. Nonmanufacturing exports are actually exploding, rising at a 37% annual rate over three months, up from 6.6% over six months and 2.6% over 12 months. But manufacturing exports are showing substantial and progressively deeper declines, falling at a 13.2% annual rate over three months; that's deeper substantially from -5% over six months and -0.5% over 12 months.

Neither export nor import flows are looking healthy for the European Monetary Union.

Looking at some separate country reporters in the bottom part of the table, we see that Germany showed a sharp drop in exports and imports in August although German imports picked up to grow to 3.3% rate over three months while exports fell at a 1.3% pace. The rise in German imports breaks off the deteriorating trend; but with declines for two months in a row for imports, it's hard to take that 3.3% gain over three months very seriously as something that will continue.

France shows declines for both exports and imports in August. However, over three months, French exports are up by 1.4% and imports are up at an 18.9% annual rate. The rise in French imports is a bit hard to understand since the economy has been weak and the three-month growth rate offsets minor declines over six months and 12 months. This may just be the result of volatility because nothing in France causes us to think its imports are rising that rapidly or that they will be able to continue to do so.

The U.K. is not in the single currency area, but its exports rose by 2.1% and its imports rose by 3.9% in August. Its export trends are showing progressively stronger growth as are U.K. import trends culminating in an 18.8% annual rate rise over three months. However, over the past week, U.K. officials have been warning that the slowdown in Europe is going to take some toll on the U.K. as well. The U.K. is not big enough to be a locomotive effect for Europe and it's much more likely that European weakness is going to help slowdown the U.K. It's just not present in the data yet.

We look at exports for the Netherlands, Finland in Portugal and find declines for two of these three countries in August and declines for two of three countries in July as well. Over three months, the Netherlands is showing a decline in exports at a 5.8% annual rate. Finland's exports are falling at a 15.9% annual rate, while Portugal is showing an increase of a 16.8% annual rate, which is part of an ongoing acceleration in exports. That certainly is good news for Portugal. But it's hard to see how it can keep that up, given the environment in the rest of the euro area. Finland shows negative export growth on all three horizons, but it's not getting progressively worse. The same is true for the Netherlands where its declines actually are getting progressively better even though they still are declines.

On balance, what we see in the euro area is probably the counterbalancing effect of trade on a weak economy. When an economy gets weak, its imports fall. The imports decline tends to push its current account and trade account into surplus and that surplus tends to mitigate the decline in GDP. We don't know yet if Europe is going to have decline in GDP in the third quarter, but we can see that the trade account in August is contributing to some muffling of economic weakness. The three-month averages - as they stand show- there is a weakening in the surplus over three months compared to six months. However, we are not yet on the right time horizon to have a full-quarter comparison.

European trade data seem to reinforce the view that we have from industrial data and from the recent German activity reports that activity in Europe is winding down. The view from the German report from the ZEW financial experts is that the German economy is on the verge of recession. Certainly, that is not contradicted in any way by the data in this trade report.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief