Global| Jun 04 2020

Global| Jun 04 2020Euro Area Retail Sales Fall Again

Summary

Euro area retail sales fell sharply again, dropping by 11.7% in April after a 11.1% decline in March. However, as May ended, European countries were in various stages of reopening their economies after battening down the hatches to [...]

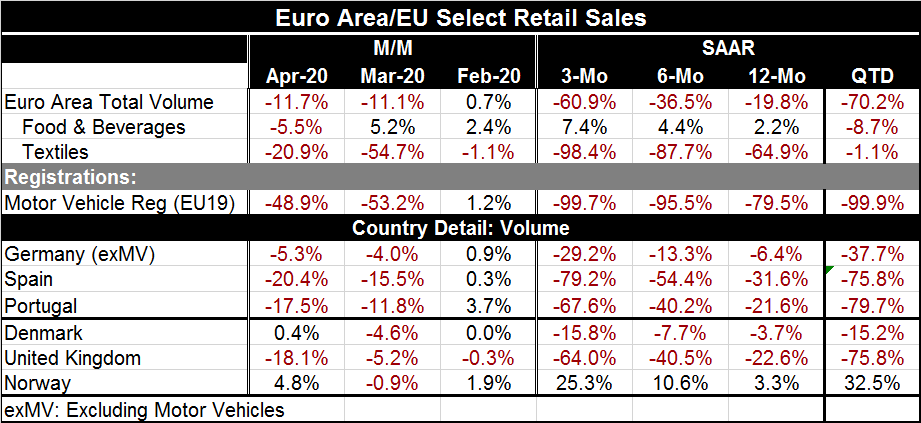

Euro area retail sales fell sharply again, dropping by 11.7% in April after a 11.1% decline in March. However, as May ended, European countries were in various stages of reopening their economies after battening down the hatches to slow the coronavirus spread. May will probably be another weak month of some sort for economic data, but June should show some growth. However, in Q2 at this point with only one month’s worth of data in-hand, retail sales are falling at a 70.2% annual rate. That growth rate is exaggerated by the timing of sales weakness since they fell sharply in the last month of Q1. That fall depresses the Q2 result even more compared to the Q1 average for sales. In Q1 sales fell at a 10.7% annual rate compared to Q4.

Euro area retail sales fell sharply again, dropping by 11.7% in April after a 11.1% decline in March. However, as May ended, European countries were in various stages of reopening their economies after battening down the hatches to slow the coronavirus spread. May will probably be another weak month of some sort for economic data, but June should show some growth. However, in Q2 at this point with only one month’s worth of data in-hand, retail sales are falling at a 70.2% annual rate. That growth rate is exaggerated by the timing of sales weakness since they fell sharply in the last month of Q1. That fall depresses the Q2 result even more compared to the Q1 average for sales. In Q1 sales fell at a 10.7% annual rate compared to Q4.

In April, sales volumes fell for food and beverages as well as for textile purchases. Weakness seems to be across commodities as well as across countries and also across a broad swath of time.

Results for three EMU members are in the table as well as for three other non-EMU-member European nations. Four of the six show declines of a substantial nature. Norway alone has a solid and strong gain with sales up by 4.8% in April. Denmark has a 0.4% gain in April but only after a much larger drop in March. All countries in the table have negative three-month growth rates except Norway, where oil wealth gives the economy added resiliency. Norway shows retail sales on an accelerating pattern from 12-months to six-months to three-months while the other five countries all show negative growth rates throughout and clear sales decelerations in progress.

Quarter-to-date there is weakness and sales declines in each of these countries except Norway, of course.

Policy actions

As European policy officials look at economic trends and ponder the future Germany has just adopted a long awaited supplement (€130bln) to an earlier stimulus plan and now has, or will soon have, stimulus in train the amount of about 30% of GDP. The European Union has proposed a €750 billion joint recovery fund that leaders will discuss later this month; that has been ‘in progress’ for some time. The ECB has just agreed to increases its asset purchases at its meeting just concluded today. It expanded the amount it would spend by €600bln in purchases (€500bln was expected) and it extended duration (to ‘at least’ June 2021). The Italian bond market reacted well to the ECB action. The Bank of England is practicing ‘social distancing’ from negative rates as Bank of England Executive Director for Markets, Andrew Hauser said on Thursday: "Even if you saw it was the right thing to do, it's not going to happen in the near term” (Source here).

Trends and the future

The chart shows how hard retail sales and auto registrations have been hit in Europe. The table gives some specificity to the extent of the weakness and nails down the timing a bit more. While there is a reopening in progress in Europe - and in the U.S. for that matter- no one is quite sure how it will progress because authorities can remove restrictions… but if people remain afraid, they will not take full advantage of the relief being offered. Also this is not a flip-the-switch to ‘business as usual.’ This is a very controlled and truncated return toward business-as-something (instead of as-nothing). It is expected that some people who have been working from home will continue to do so for a while. Not all businesses are opening and some are opening with restrictions of various sorts. That is an argument for the transition to growth to be moderate. But some people are chomping at the bit for more freedom and are ready to go and do not fear the risks. So this is going to play out differently in different countries and regions and even neighborhoods. At the same time, there is a risk of backsliding and of a second wave of infections. There is no guarantee that recovery will build on recovery and things will simply move ahead and gather a head of steam. Policymakers are watching. As of today, they were still offering up new options to try to assure that growth takes hold. We are headed for a period of enhanced growth to some extent and also of enhanced risk.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief