Global| Mar 02 2018

Global| Mar 02 2018Euro Area PPI Year-on-Year Pace Drops to 1.5% from 2.2%

Summary

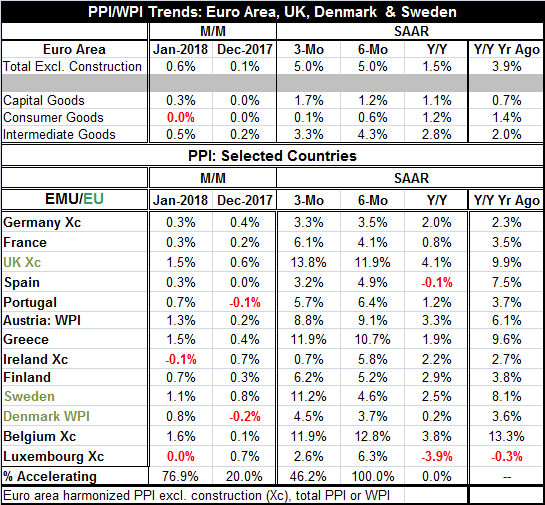

The year-on-year PPI for the EMU was lower in January as the pace dropped to a 1.5% year-over-year gain from 2.2% previously. Compared to the year-on-year pace of one year ago inflation decelerated to a 1.5% gain from 3.9%. And on [...]

The year-on-year PPI for the EMU was lower in January as the pace dropped to a 1.5% year-over-year gain from 2.2% previously. Compared to the year-on-year pace of one year ago inflation decelerated to a 1.5% gain from 3.9%. And on this same basis of comparing current year-on-year inflation to inflation of one year ago, inflation has declined in January for each country in the table. However, for industrial sectors in the PPI on this basis inflation is higher for capital goods and for intermediate goods. Sector inflation is lower compared to one year ago for consumer goods.

The year-on-year PPI for the EMU was lower in January as the pace dropped to a 1.5% year-over-year gain from 2.2% previously. Compared to the year-on-year pace of one year ago inflation decelerated to a 1.5% gain from 3.9%. And on this same basis of comparing current year-on-year inflation to inflation of one year ago, inflation has declined in January for each country in the table. However, for industrial sectors in the PPI on this basis inflation is higher for capital goods and for intermediate goods. Sector inflation is lower compared to one year ago for consumer goods.

The sequential inflation patterns are not so favorable. For example, every country in the table shows inflation higher over six months (annualized) than over 12 months. But over three months results are relatively balanced with inflation accelerating in 46% of the reporters.

Headline (excluding construction) inflation is up from a 1.5% pace over 12 months to a 5% pace over both six months and three months. So while headline inflation has decelerated broadly on year-over-year trends, the near-term news is actually not as good and it offers a more cautionary outlook for the future. And the fact that both three-month and six-month trends show 5% inflation probably makes the situation a bit worse.

Inflation is lower in January because the 0.6% increase in the PPI this year is smaller than the 1.3% gain in the PPI in January 2017. Looking ahead the EMU PPI rose in only one month over the six months from February through July 2017. In that one month (April), it rose month-to-month by 0.1%. The PPI fell in four of those six months and was unchanged in one other month. That means that there is a stretch of months coming up in which if the PPI rises at all that will lead to an acceleration in year-on-year inflation. The PPI seems to be set up for a rough patch over the next six months unless oil prices move lower and help to persistently depress headline prices.

Of course, we offer the usual caveat here that it is the HICP that matters for policy not the PPI. And for now the disinflation pressure are very widespread.

The economic news has been scattershot. German just reported out declines in both wholesale and retail sales for January. These declines were unexpected.

The geopolitical and policy back drop has suddenly soured. Beware! With the Trump administration threatening more seriously to impose tariffs on steel and on aluminum, global markets are not taking the news well --and neither are U.S. trade partners who also are taking of retaliation. Trump oddly is quoted this morning saying that trade wars are good. But good for what is another matter. Russia's announcement that it has developed a new nuclear weapon that can bypass the U.S. air-defense systems has led today to an accusation that Russia has violated the arms limitation treaty. Russia denies this. But if it has done what it claims it has been caught red-handed...so to speak. And there is still all the bad blood over Russia and disruption of elections in the West. China has literally threatened war if the U.S. passes a bill that is in the house of representatives concerned with having closer relations with Taiwan. And NATO has told Russia that its statement about developing an air-defense penetration system is not helpful to peaceful relations.

All in all, it is hard to think that we can separate and isolate these occurrences from economic impact. On top of that, Europe is being slammed by a cold front that has been so severe it has a stepped up death toll associated with it.

While everyone has been optimistic coming into this year that growth was picking and that things would be better, we can now identify any number of events that are interfering with Ms. Rosy Outlook. It may be a good time to take stock again despite the recent testimonies of the new Fed chairman that make a series of rate hikes seem more or less inevitable.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief