Global| Jun 02 2016

Global| Jun 02 2016Euro Area PPI Is Falling Again But Not Decelerating As ECB Is Willing But Still Waiting

Summary

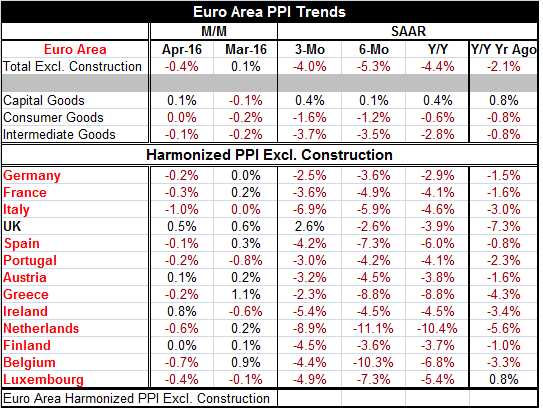

The PPI is still falling The EMU-wide PPI gained in March but is falling again in April. After a 0.1% gain in March, the PPI is lower by 0.4% month-to-month in April. It is still falling year-over-year and by 4.4% (excluding [...]

The PPI is still falling

The PPI is still falling

The EMU-wide PPI gained in March but is falling again in April. After a 0.1% gain in March, the PPI is lower by 0.4% month-to-month in April. It is still falling year-over-year and by 4.4% (excluding construction- as always).

Sector trends are still weak

PPI month-to-month sector trends show that the PPI remains weak as the headline fell by 0.4% in April from March. For capital goods, the PPI rose in April by 0.1%. For consumer goods, it was flat. The PPI for intermediate goods fell by 0.1%. The overall sequential growth rates find the PPI lower by 4.4% over 12 months, falling at a 5.3% annual rate over six months, and falling (only) at a 4% pace over three months breaking the trend to persistently faster price declines (deceleration). By sector, the chain of persistent deceleration is broken only for capital goods and there it is broken weakly. Capital goods prices rise by 0.4% over 12 months; they rise at just a 0.1% annualized pace over six months. However, over three months, they accelerate, rising at a 0.4% pace, faster than over six months but still only at their 12-month pace of 0.4%. Consumer goods prices still are decelerating: falling at a 0.6% pace over 12 months, at a 1.2% pace over six months and at a faster 1.6% pace over three months. Similarly intermediate goods prices are decelerating with a -2.8% year-on-year drop, a -3.5% pace over six months and a -3.7% pace over three months. There is still a lot of downward price pressure in train component by component with capital goods being the main resisting sector (and the one with the most independent value added).

Price are still falling `everywhere all the time'

We can also look at trends across countries. In the table, we chronicle the results for the first 12-EMU members plus the U.K.: We calculate sequential growth rates over three-month six-month and 12-month. For the 36 calculations for EMU members over these horizons, all 36 show declines in prices- a rather grim and clearly uniform result. The U.K. (with its own exchange rate) shows PPI prices contrarily up at a 2.6% pace over three months.

Still...Cross-country trends show less weakness in train

On the issue of deceleration, we see a marked departure from the sector results we chronicle above. Here we see that for all EMU members, while prices fall year-over-year, when we compare that price fall to each nation's six-month trend, we find that prices fall faster over six months-or at the same pace- for all EMU members except Finland. Non-member the U.K. is also an exception. But over three months, we find the biggest difference. Here we see deceleration is in train compared to six-month for only three members with nine members showing PPIs accelerating. In this instance, that means PPIs are falling more slowly over three months than over six months for 9 of 12 members. However, inflation is still decelerating in Italy, Ireland and Finland.

Monthly patterns show a shift

As to monthly patterns, prices rose in seven of 12-member countries in March. But they only rose month-to-month in April in two members: Austria and Ireland. Prices rose back-to-back in March and April only in Austria and in nonmember U.K., but prices did rise in Finland in March and were flat month-to-month in April. The monthly evidence over the past two months lays the foundation for price drops to diminish in magnitude.

Underlying trends are changing despite headlines

This extreme parsing of the data by sector and by country is meant to identify what trends are and where they are headed. Prices largely are still falling. But the speed of their descent is braking. The deflationary trend is being broken by first reducing price acceleration in the downward direction. It will take some time to actually push prices up year-on-year. The overall 4.4% price drop will take time to unwind. At the country level, the Netherlands have the fastest 12-month drop at -10.4% over 12 months and Germany has the smallest at -2.9% over 12 months.

Complicated trends in prospect

Globally trends are changing slowly, but in the EMU the acceleration of deflation is now being set aside. The fact of deflation is still present. But with oil prices having risen, there is the blunting of one force that has been driving deflation trends. The more recent run-up in oil prices can't help but flow through to provide some upward impetus to overall price trends. Still, OPEC is meeting and there is still an oil glut. I am still not willing to call oil prices at $50/barrel `stable.' OPEC still has challenges. If prices do stay at this level, more U.S. energy output will come on stream. Meanwhile, global growth is still at a relative crawl; thus, demand is not picking up very fast. If some of the special factors that have hit oil production reverse, we could easily find the glut is back and hammering prices lower again (these special factors are a strike in France, wildfires in Canada and instability in Nigeria). Iran is still planning to ramp up output and is not giving any ground going into the OPEC meeting- nor do we expect it to do so.

ECB met and kept more or less on track

The ECB held its policy steady at today's meeting. Mario Draghi warned about stabilizing inflation at too low a level. Of course, the ECB has its eye on the HICP price index not on the PPI, but the problems to which Draghi refers are clear-at least to all but the Germans who are quite content with too-low inflation. Imagine the story of Goldilocks and the three bears in which the three bears each taste a single bowl of porridge and one finds it too cold, one finds it too hot and one finds it just right. That just about sums up how the various EMU national banks see EMU-wide inflation. Each has different views on what's right or acceptable. It is not about the `fact' as much as the perception. Of course, the ECB also has a stet inflation objective, but that too is read differently by different members.

ECB `willing to do more' but wants `patience'

Draghi also announced that the ECB was willing to take further action if inflation did not pick up- but modified that by saying there was a need for patience to see if past efforts would bear fruit. Despite oil prices rising from their lows, the ECB's economists did not shift their outlook for inflation much for 2016 and left their 2017 and 2018 views unchanged. That means that the ECB, on those projections, is still not meeting its promises on inflation and there will be more work to do but apparently no more for now.

Growth outlook is better but tempered

As to growth, Draghi warned that growth would slow from its first quarter pace and that weaker demand from developing countries for EMU exports would continue to be a restraining consideration. ECB economists did hike the growth outlook for 2016 to 1.6% from 1.4% and held their 2017 view at 1.7%. The OECD had raised its outlook in its release of yesterday because of better-than-expected Q1 growth. The OECD and the ECB economists now have the same view of growth in 2016. In his comments Draghi suggested that the X-factor to speed growth would be the faster implementation of economic reforms ignoring the OECD's plea for more fiscal stimulus made just yesterday. Draghi also noted the risk of the outlook to the ultimate Brexit decision.

Today's ECB action

The central bank's main interest rate, which it charges on ordinary loans, remains at a record low of 0%. The deposit rate stays at -0.4%, so that commercial banks continue to pay to place funds with the central bank overnight. The ECB said that it would start its corporate bond purchase program on June 8 and would conduct its first operation in its new series of targeted loans on June 22. Patience.

Other factors: the policy Twilight Zone

Draghi sort of minces words by saying that he is willing to go further then muddying that message by asking for patience. Also the fact that the ECB has an underlying forecast that shows that it is falling short of its policy goal for inflation leaves us somewhat confused as to its intent and overall message. At the BOJ, policymaker Takehiro Sato said today that he thinks that negative interest rates have the effect of monetary tightening. Japanese data show a surge in monetary base and that bank notes in circulation are up by 6.5%. Many Japanese have responded to the negative interest rate environment by hoarding cash; there is a shortage of safes as demand for home security has risen there. When policymakers cannot agree on whether their policy is a positive or negative, monetary policy has really stepped into the Twilight Zone. We see that in play in Japan as well as in the EMU as the Germans stridently disagree with the ECB's recent policy efforts.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief