Global| Mar 24 2010

Global| Mar 24 2010Euro-Area PMIs Rise Sharply Other Things Unravel…

Summary

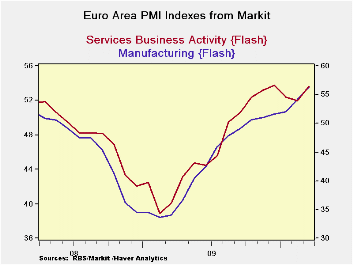

TheEuro-Area PMIs rose sharply in March. For MFG the index reached a new post recession high, it s strongest level since January 2007. For services, the 1.68 point rise to 53.65 brings it close to its cycle high reading of 53.71 and [...]

TheEuro-Area PMIs rose sharply in March. For MFG the index reached a

new

post recession high, it s strongest level since January 2007. For

services, the 1.68 point rise to 53.65 brings it close to its cycle

high reading of 53.71 and it stops a string of two months of

declines.

TheEuro-Area PMIs rose sharply in March. For MFG the index reached a

new

post recession high, it s strongest level since January 2007. For

services, the 1.68 point rise to 53.65 brings it close to its cycle

high reading of 53.71 and it stops a string of two months of

declines.

The services index is in the 62nd percentile of its 136 month range; the MFG index is in the 84th percentile of it range.

In addition to all this good news, separately, the German IFO index moved sharply higher, confirming goods news in Germany. The European economy is giving off signals of real strength and brushing off notions that the recovery there was falling on hard times. Still the euro is falling.

The bad news on the day that has dragged down the euro, was the downgrade to Portugal by Fitch. Meanwhile, France and Germany seem to have to come to some agreement about letting the IMF assist Greece in some way. We are all waiting to hear more on this.

With the geopolitics of Europe seemingly dry tinder and sparks flying everywhere, the news of better growth in the Zone is like news of a refreshing spring shower that will damp the risks of spontaneous combustion. There is still a long way to go to get Europe back to where it needs to be. And the problems in Greece and the knock-on effects there have exposed some animosities within the Zone that may have long term effects on it. They could affect not only the Zone’s appetite for expansion but also the perception of the attractiveness of membership in the Zone by potential EMU candidate countries.

| FLASH Readings | ||

|---|---|---|

| Markit PMI's for the Euro-Area | ||

| MFG | Services | |

| Mar-10 | 56.34 | 53.65 |

| Feb-10 | 54.23 | 51.81 |

| Jan-10 | 52.39 | 52.50 |

| Dec-09 | 51.59 | 53.63 |

| Segment Averages | ||

| 3-Mo | 52.74 | 52.65 |

| 6-Mo | 51.57 | 52.86 |

| 12-Mo | 46.50 | 49.60 |

| 136-Mo-Range | ||

| High | 60.47 | 62.36 |

| Low | 33.55 | 39.24 |

| % Range | 84.7% | 62.3% |

| Range | 26.92 | 23.12 |

| Average | 51.13 | 53.64 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief