Global| Jan 03 2017

Global| Jan 03 2017Euro Area PMI Rises While Asia Stumbles, Global Risk Rises and Investment Trends Realign

Summary

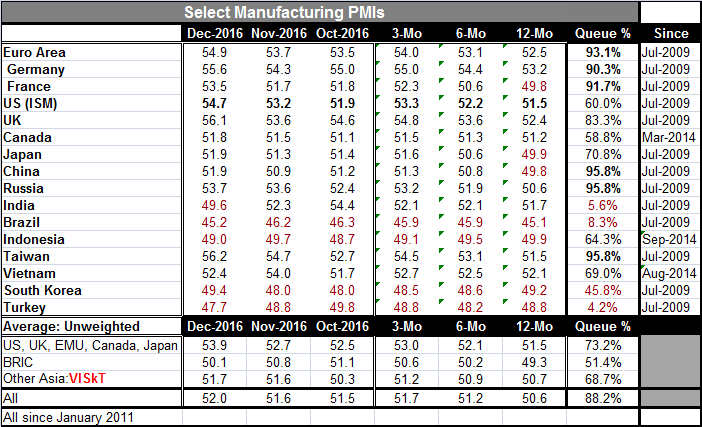

Manufacturing PMI data for the most part show ongoing expansion and improvement. Of the 17 key manufacturing reporters in the table, only five show manufacturing PMI values below 50 indicating sector contraction. Only five have [...]

Manufacturing PMI data for the most part show ongoing expansion and improvement. Of the 17 key manufacturing reporters in the table, only five show manufacturing PMI values below 50 indicating sector contraction. Only five have relative standings below their 50th percentile (below their respective medians calculated back to January 2011) and of those only four have extremely low relative standings: Mexico, Brazil, India and Turkey (and these are extremely low).

Manufacturing PMI data for the most part show ongoing expansion and improvement. Of the 17 key manufacturing reporters in the table, only five show manufacturing PMI values below 50 indicating sector contraction. Only five have relative standings below their 50th percentile (below their respective medians calculated back to January 2011) and of those only four have extremely low relative standings: Mexico, Brazil, India and Turkey (and these are extremely low).

China shows improvement on the Markit manufacturing measure, but its own 'official' PMIs reveal a drop in both the manufacturing and nonmanufacturing gauges in December. Still, the level for the official manufacturing reading is only slightly weaker than in the Markit framework. The Markit gauge is plotted in the chart above and that shows China is engaged in a long slow dig-out from a period of real weakness. The U.S. (on the ISM manufacturing measure) is moving up quite sharply while the EMU shows relatively rapid improvement in gear. U.S. regional manufacturing surveys have been somewhat more equivocal, showing most of their strength not in the current index but in their future indices. The December U.S. ISM manufacturing index, a current manufacturing reading, shows strength pretty much across the board with an increase in employment and strong gains in prices, production and in orders with a relatively high export diffusion score. Despite the strong U.S. gains the ISM on a longer profile than Markit allows has only a 69th percentile queue-standing for its headline, orders have a more robust 79th percentile standing with production at an 83rd percentile standing. Exports, despite their jump, have only a 76th percentile standing while imports have a much lower 26th percentile standing. U.S. domestic demand does appear to have been excited just yet. So why are exports cooking and how can that be the case with such a strong dollar? Sometimes the PMI gauges pose more questions than they answer.

Globally, there is a division of strength in the mix. With the PMIs evaluated only since January 2011. Developing economies are lagging. China is a bit of an enigma with two PMI surveys pointing in different directions in terms of momentum, but both still show some growth in terms of the raw diffusion score. Still, the BRIC index is weaker on the month. A second index combing Taiwan, South Korea, Vietnam, and Indonesia barely ticked higher in December and did so only on the back of a sharp gain in Taiwan and an improvement in South Korea that still left that index below 50.

In Europe quite apart from the EMU index rising, there was strength in the U.K., Ireland and the Netherlands and strong moves in a number of other European nations. Manufacturing is stirring, perhaps stimulated by the dollar's strength (euro weakness).

Over 12-months only five countries have net-weaker manufacturing sectors; they are Turkey, Mexico, South Korea, Japan and Brazil. The strongest gains over 12 months are in the U.S., Russia, the U.K., Taiwan, and Canada, in that order. Turkey is weak in the aftermath of last year's failed attempted coup. India is struggling in the wake of its currency reform which yanked certain high denomination bills out of circulation in that cash oriented society that is still reeling from the shock. Venezuela is simply struggling as its socialist policies have hit a brick wall. Brazil, having also been beset with a corruption trial, is limping. There are countries in this mix with their own special problems. A reference to universally felt macroeconomic forces can no longer adequately describe the global economy.

Still, there may be a pick up growth brewing. The PMI indices are sensitive. But they also can give off false signals. In Europe, domestic monetary and credit measures are still not showing much pick up at all. The revival so far is all on the real side not on the monetary side, and that is somewhat suspicious. The U.K. is surging as the Bank of England implemented a lot of stimulus in the wake of the Brexit vote and since markets failed to collapse the stimulus went to the bottom line and juiced growth instead of buffering a shock. Instead, between the extra easing and impact on the pound sterling, the U.K. is undergoing a new revival. Germany is gaining momentum ever so slowly. France has perked up but still is weakened as its rising PMI variables remain at low levels. The Baltic dry goods index, an indicator of trade volume, is continuing its slow but steady up-creep.

The thing to remember about the PMIs is that formally they are indicators of breadth not of strength. We take improved breadth to be an indicator of improved strength, but that may not always be the case or breadth and strength might improve at unequal speeds. Right now the manufacturing PMIs are simply moving up faster than other economic gauges and that seems out of kilter with reality and it may well be. The PMIs as well as the underlying economic activity data remain important things to watch especially as the U.S. economy reignites growth under a new president. But international markets need to be aware since the new president is trying to generate, concentrate and retain growth in the U.S. This is not going to be a traditional U.S. locomotive growth pull for the rest of the world if President Trump has his way. However, the strong dollar is a fly in the ointment. But even with dollar strength, Mexico, a target for Mr. Trump's trade ire, suddenly is lagging. Some U.S. investment has been diverted from going to Mexico and has chosen to stay in the U.S. Ford just announced that a factory it was planning in Venezuela will be kept in the U.S. Whether that is because of pressure from the incoming president or due to Ford seeing too many problems in Venezuela is not clear. Either way it works in the U.S. favor. And that makes another point. As international relations become more strained, and as the sense of global risk is raised, the return to global investment has to be higher to make the risk worthwhile. Raising the global risk profile actually helps U.S. firms to make the decision to keep production at home. But then, there is that strong dollar to contend with. The world has gotten even more complicated and just when you thought you had figured things out, they are going to shift again. And we have not seen the end of that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief