Global| Dec 15 2016

Global| Dec 15 2016Euro Area PMI Holds 11-month High

Summary

Divergence strikes the Euro-Areas sector indices. While the EMU PMI headline is unchanged at an 11-month high the means to stay up is propped on some substantial divergence. The EMU-wide manufacturing index is on its highest level [...]

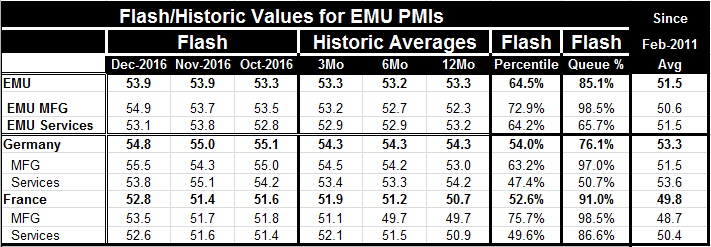

Divergence strikes the Euro-Areas sector indices. While the EMU PMI headline is unchanged at an 11-month high the means to stay up is propped on some substantial divergence. The EMU-wide manufacturing index is on its highest level since April of 2011. Meanwhile services have stepped back to a pace last stronger in September of this year. The manufacturing reading has an out-of-body sort of reading at its 98.5th percentile on data back to January 2011 - exceptionally strong. The service sector PMI has a 65th percentile standing.

Divergence strikes the Euro-Areas sector indices. While the EMU PMI headline is unchanged at an 11-month high the means to stay up is propped on some substantial divergence. The EMU-wide manufacturing index is on its highest level since April of 2011. Meanwhile services have stepped back to a pace last stronger in September of this year. The manufacturing reading has an out-of-body sort of reading at its 98.5th percentile on data back to January 2011 - exceptionally strong. The service sector PMI has a 65th percentile standing.

Germany echoes this divergence. Its overall private sector PMI index backtracked despite a manufacturing index that is up to 55.5 in December, its highest since January 2014. Services meanwhile took a sizeable step back, dragging the headline lower, falling to a diffusion reading of 53.8 from 55.1 in November. The German MFG index has a 97 percentile standing while services stand just a hair above their median value since January of 2011 at a standing of 50.7 percent. Strong output meets mediocre services; it's incongruent.

In France we were spared this path to divergence as the PMI headline rose on increases in both manufacturing and in services. The French manufacturing index is up to its 98th percentile while services stand strongly at their 86th percentile. France, however, has its own divergence: strong PMI relative standings amid what are still weak-to-moderate absolute diffusion readings in each sector.

Manufacturing is the more volatile index so the upswing in manufacturing is an impressive development and a potential trend leader especially with both Germany and France riding this particular gravy train together. However, the German engine is not pulling services up in step and services are stumbling in EMU, taking some of the glow from this report. Recent PMI data globally have been relatively upbeat although other signs of international revival have been less impressive. The recent US and European industrial output reports, for example, were not particularly impressive.

The outlook is still on the chopping block. Both Germany and the Fed in the US have lifted by small margins their outlooks. In the U.S. the Fed did take that step to hike rates and markets are in a dither despite the hike having been well-telegraphed and well-expected. Consumer attitude surveys in the US are in an upswing but recent output and consumer spending reports in the US have vacillated. In Europe it is much the same thing with some recent volatile retail sales results; although today a nice rebound in vehicle registrations was reported in Europe. In Asia Japan's MFG PMI has ticked up in December.

On the geopolitical front China is pushing back at some of the rhetoric of not-yet-President Donald Trump. China has asserted its right to militarize the South China Sea outposts it has built and that the world court has essentially said it has no right to. And China is going after U.S. auto companies doing business in China. The age of confrontation has begun. The age of complacency and of the U.S. simply rolling over and turning the other cheek is over. There will be change. Some of it will be unpleasant. But sticking up for your rights often is that way, isn't it? Today the UK's E.U. ambassador told his countrymen that it could take a decade to finalize a new trade deal with the E.U. post Brexit. Meanwhile we have some interesting trends to watch and to ponder, not the least of which is wondering where this manufacturing revival has come from and if it plans to stay or to leave unexpectedly. In the US there is clear case for inventory-building after what has been a period of some substantial drawdowns even as the pace of sales picked up. But the global story has to be based on something else. We will continue to look for it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief