Global| Sep 18 2013

Global| Sep 18 2013Euro Area Orders Recovery Is Not Uniform

Summary

Industrial orders trends for the Eurozone continue to come in country by country. Of the five early reporting countries in EMU, industrial orders are down in July for three of them, namely Germany Portugal and Finland. In July orders [...]

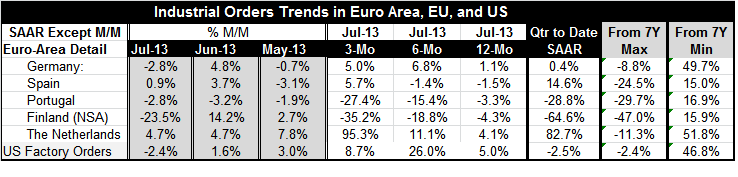

Industrial orders trends for the Eurozone continue to come in country by country. Of the five early reporting countries in EMU, industrial orders are down in July for three of them, namely Germany Portugal and Finland. In July orders rose in Spain and in the Netherlands. In contrast US orders fell by 2.4% in July, roughly in line with the German performance.

Industrial orders trends for the Eurozone continue to come in country by country. Of the five early reporting countries in EMU, industrial orders are down in July for three of them, namely Germany Portugal and Finland. In July orders rose in Spain and in the Netherlands. In contrast US orders fell by 2.4% in July, roughly in line with the German performance.

Turning to trends over three months we have declines in two of the five early reporting EMU nations and a 27% annual rate of decline in Portugal and a 35% annual rate of decline in Finland. Orders in Spain are up by 5.7% at an annual rate. In Germany orders are up at 5% at an annual rate. The Netherlands has suddenly come to life with orders spurting at a 95% annual rate. By comparison factory orders in the US are up at an 8.7% annual rate.

We also see different trends in this table. For Germany and Spain orders are showing either modest growth or declines over 12 months, then improving over six months to three months, positing annual rate gains of 5% or more over three months. In Portugal and Finland we are looking at countries that have year-over-year declines in orders that are getting worse over six months and even worse over three months. The Netherlands of course shows this incredible pattern of exploding growth moving from a year-over-year growth rate of about 4% to this enormous annualized growth rate of 95% over three months. Over the same period US trends are less clear with 5% order growth over 12 months moving up to a 26% at an annual rate over six months and then edging back down to a pace of 8.7% over three months. It's hard to draw comparisons between the US and European trends because the European trends are so varied and because some of the key European countries like France and Italy have yet to report order figures.

Turning to the specific trends for the quarter in progress (Q3), orders are declining in the quarter to date at a very sharp pace once again for Portugal and Finland. Germany has a small increase and Spain a more sizable 14.6% growth rate in July over the second quarter base. We see another stupendous growth rate for the Netherlands with orders rising at an 82% annual rate early in Q3. These figures compare to some weakening in the US, as orders are falling at a 2.5% July over the second quarter base.

All the countries in the table show some amount of rebound from their seven-year minimum level of orders. The statistic is an attempt to try to look at the rebound by recognizing that countries may have hit peaks and troughs at different points in this business cycle.

The current level of orders is up from its cycle low by about 15% to 17% in Spain, Portugal and in Finland. Germany, the Netherlands and the United States, show increases from order low points that range from roughly 47% to 52%. In a sense we seem to have approximately 2 groups of countries, some that have made barely any progress from their cycle lows and others that have made substantial progress. We don't changes results very much by looking at the current level of orders compared to their past cycle peaks. On that basis once again we have Spain, Portugal and Finland with orders that are 24 to 47% below their cycle peak. Finland becomes a bit of an outlier as Spain and Portugal are off between 25% and 30% from their respective cycle peaks while Finland is down 47% from its cycle peak. Orders in the Netherlands are down by 11% from their cycle peak followed by Germany which is down 8.8% from its cycle peak and the US which is only down by 2.4% from its cycle peak.

So we see the ongoing economic recovery through several different lenses using these metrics. We see the recent momentum and we are able to evaluate orders performance relative to its recent history. Both ways of looking at things produces roughly the same result which is that Spain, Portugal and Finland are economies are still struggling. While Germany- along with the United States- appears to be an economy that is making what looks to be a more normal economic recovery with the Netherlands as at Johnny-come-lately to the good news club.

Of course, when we compare this economic recovery with the past recoveries even for those countries that are performing well, the results are weak. That's just another way to point out how very weak conditions remain in the countries that are lagging in this already lethargic economic recovery. While there has been some optimism in Europe recently about some of the better economic numbers, it also appears that some of this progress continues to be concentrated in Germany, other broad measures of European economic activity and demand such as auto sales continue to lag when you look at statistics for EMU beyond the borders of Deutschland.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief