Global| May 31 2016

Global| May 31 2016Euro Area Money and Credit Growth Slow

Summary

Central bank bond purchases and negative interest are still not pumping up money growth in the EMU. The year-over-year growth rates for money and credit have backed off, leaving the stimulus policies without a solid backing from the [...]

Central bank bond purchases and negative interest are still not pumping up money growth in the EMU. The year-over-year growth rates for money and credit have backed off, leaving the stimulus policies without a solid backing from the main monetary metrics. Negative interest rates may have more mixed impact than monetary authorities want to admit as negative rates do not inspire confidence in the general public.

Central bank bond purchases and negative interest are still not pumping up money growth in the EMU. The year-over-year growth rates for money and credit have backed off, leaving the stimulus policies without a solid backing from the main monetary metrics. Negative interest rates may have more mixed impact than monetary authorities want to admit as negative rates do not inspire confidence in the general public.

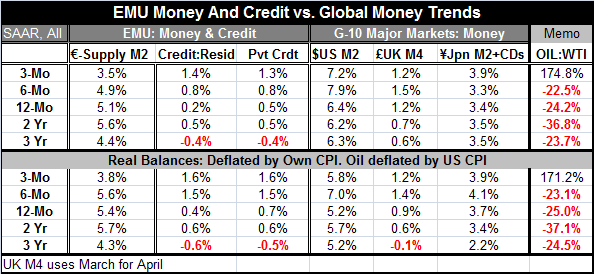

However, sequential growth rates for 12-month to six-month to three-month show that money growth and credit growth rates are picking up but only within the last year.

Outside of the EMU, nominal money growth rates and real money growth rates also show that sequential rates are moving higher.

On the real side of things, the EU Commission sentiment index for the EMU (released yesterday) has now advanced for two months in a row but stands only in the 61st percentile of its historic queue of values. Of the 16 early-reporting countries, only six of them actually posted gains for their respective country-level indices. This echoes what we found in the Markit PMI survey earlier. The three largest EMU members (Germany, France and Italy) posted gains along with Austria, Belgium, and Estonia with all the rest showing month-to-month declines. Five EMU members still have queue standings of their EU Commission sentiment gauges that are below the midpoints of their respective country level gauges. Retailing and consumer confidence continue to be the areas in which the EMU economy is performing the best. On that score, the backtracking in German retail sales reported in March and again in April is something to be watched. The industrial sector is lagging but still has a result above its historic median. The services sector is firm. Construction across the EMU barely sits above its historic median reading.

While the EMU region clearly is growing, there is not much going on to generate price pressure. The ECB remains behind the eight ball as far as hitting its inflation objective and does not even show much progress toward that goal. The weak euro exchange rate might be some help. But global growth remains weak. As the table shows, oil prices have been falling sharply over recent periods. The new reading on EMU-wide inflation shows that prices dropped again in May.

Meanwhile, unemployment rates are still largely being trimmed across the EMU. But on a region-wide basis, the rate is stuck at 10.2% for the second month in a row. Among the original 11 EMU members, only Germany and Ireland have unemployment rates that are below their historic medians. Germany's rate is exceptionally low, at a reunification low. Ireland's rate stands in the 42nd percentile of its historic queue below its median which occurs at the 50th percentile. After that, the closest to its median rate is Finland with a 57th percentile standing followed by France at a 66th percentile standing. Three of these members still have unemployment rates stuck in the top 10% of their historic queues of unemployment rates. That reflects very little progress.

The sequential growth in money and credit offers some hope that the ECB policies will get traction. Globally oil prices have rebounded and are up very strongly over the last three months. But it is not clear where oil is going next after it has gotten back to $50 a barrel. At this level, a lot of U.S. alternate energy production makes sense again and supply could begin to increase re-establishing the glut.

There is also the impact of U.S. monetary policy to consider. If the Fed really goes on a rate hike spree to achieve normalization, that would carry the dollar higher and could push commodity prices lower and rekindle the problems associated with that.

On balance, the global economy is pretty well interconnected. For every action, there is a reaction. In Europe, the ECB's aggressive actions have been off-putting in Germany and have unsettled others who are simply not reassured by negative interest rates. In the U.S., policy is focused on getting the Fed funds rate back to normal, but that will also relaunch a strong dollar and could be a policy that undermines itself. Most policies have secondary effects associated with them. Usually we see the primary policy effect as the operative one and tend to downplay adverse repercussions. But in this cycle, monetary policy has simply not been as effective in delivering stimulus and in this environment the secondary effects of policies have become more significant. That is especially true when the secondary effects are unconventional and not well understood. For Europe this has been the policy of negative interest rates and for the U.S. it has been the impact of rate hikes on the dollar. In both cases, central banks have some significant negative repercussions policy has to account for and does not seem to have done so far.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief