Global| Jul 27 2016

Global| Jul 27 2016Euro Area Money and Credit Growth Are Still Broadly Stalled; But These Are Not the Paths to a Solution

Summary

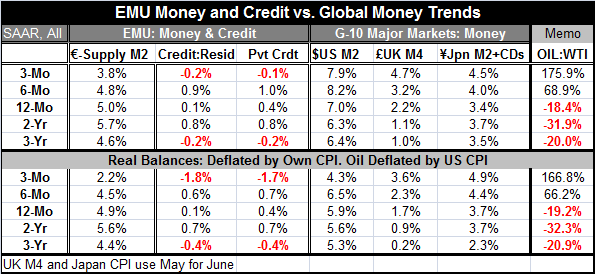

While the monthly money and credit numbers show some small upticks, the broader three-month growth rates for EMU money and credit continue to disappoint and to show deceleration. There is nothing good going on for the ECB to point to. [...]

While the monthly money and credit numbers show some small upticks, the broader three-month growth rates for EMU money and credit continue to disappoint and to show deceleration. There is nothing good going on for the ECB to point to. Japan announced its stimulus policy today without giving us much in the way of details. While Japan's stock market jumped on news of a $265 billion plan (28 trillion yen), Japan's problems remain deep-seated. A bit of fiscal rearrangement of the deck chairs on the Titanic doesn't really look like what the doctor ordered. But that, of course, depends on who is the doctor and if the doctor understands the problem.

While the monthly money and credit numbers show some small upticks, the broader three-month growth rates for EMU money and credit continue to disappoint and to show deceleration. There is nothing good going on for the ECB to point to. Japan announced its stimulus policy today without giving us much in the way of details. While Japan's stock market jumped on news of a $265 billion plan (28 trillion yen), Japan's problems remain deep-seated. A bit of fiscal rearrangement of the deck chairs on the Titanic doesn't really look like what the doctor ordered. But that, of course, depends on who is the doctor and if the doctor understands the problem.

Japan remains in denial of sorts. Does Europe, too?

Countries/regions continue to focus on traditional tools and even to lean heavily on overused tools long after their use has proved to be less than productive. How much longer?

The Tug of war analogy...

My analogy for this predicament is that it is like two sides trying to instigate a tug-of-war. But as they pull on their respective sides of the rope, nothing happens because there is a big unused coil of rope between them. Both sides can pull and transfer yards of rope behind them, but because the coil of unused rope between them is so large, nothing happens. Pulling produces no tension. Imagine being on one of those teams and not knowing about the great coil in the middle. What would you do? Pull ever harder? Pull faster?

Being impotent changes what's important

This analogy refers to the huge excess capacity in the global economy and the inability of stimulus in the West to create economic traction. China and other developing economies are the new standard bearers for competiveness. Jump-starting fiscal spending in the developed world may seem like a solution, but since so much `stuff' is made overseas, the leakages from the domestic spending stream to the overseas suppliers that make the stuff that consumers buy all but ensures that developed-economy stimulus will be less potent. Even when domestic demand is successfully stimulated (to some degree) by some method, domestic supply in the `West' is not forthcoming because suppliers know the cause is artificial. Because of poor competiveness firms are unwilling to build on artificial stimulus.

Can't `prime' a broken pump...

Japan's planned use of Keynesian pump-priming can't work if the pump is broken. Even Bob Dylan knew that the pump wouldn't work `cause the vandals stole the handle. In that environment fiscal spending does not `prime the pump.' It only serves as a temporary prop to demand which fades and when it is gone it leaves the legacy of debt which fostered it.

Some similarities; some differences

Europe and the U.S. have somewhat similar competitiveness issues. Europe also has banking sector problems especially in Italy. News reports today warn that Air France sees France being less selected as a destination because of terrorist concerns. One German politician warns of growing fear in Germany. These sorts of things will make getting growth in gear all the harder.

Hillary grabs Trump by the issues?

We see news reports today that, in the U.S., Hillary Clinton has promised the UAW chief that she would renegotiate NAFTA if elected. This has been a Trump policy pledge, albeit one made in public, not behind the scenes. Is Trump having a real impact on core issues? He seems to be changing the discussion.

Not just any Trade...FREE TRADE!

In my view, TRADE has become a huge IMPEDIMENT to growth. This makes me more a supporter of some of the controversial polices of Donald Trump - who I think has more substance to his positions than most give him credit for. Contrast this to Kenneth Rogoff's criticism of Trump as anti-trade and connecting the dots by critically saying that Trump is pro-growth but wants to slow the fastest growth part of the global economy, trade. Yes! He does! That's right, Ken. Trump wants to slow that fast-growing part that is eating our lunch like Pac Man in an arcade game. We want the benefit of some of that growth; if there is less growth overall, that is better for us.

The very obscured `discourse' over trade

In the `discourse over trade,' let it be lost on NO ONE that conventional Ivy League economists talk as though `trade' is the answer. Trade is not the answer. Economics enshrines FREE TRADE only. When trade is conducted in a less than free environment, the results are distorted. China and others use currency manipulation and mercantilistic methods to boost their trade flows and their growth at our expense. We have every right and DUTY to slow it down. China is using the game of currency depreciation again. China is playing unfair with geopolitics in the South China Sea. China is a great example of what is wrong. And China is so large; it is like a black hole sucking all the air out of the global economy by expanding rapidly using unfair methods and supplying too much output on the margin while offering up too little in demand. China's skewed path to growth has led to a huge global supply/demand imbalance; that is the reason why conventional polices no longer work. Try to prime your pump with domestic demand stimulus and you will wind up priming Chain's pump and stimulating its output.

Instability personified

It is obvious that the source of global demand is in the traditional Western countries while the emerging economies have become the suppliers of output and that this sort of economic `specialization' is not what anyone ever had in mind. You cannot have separate consumer nations and producer nations and expect to have any sort of stability since large and growing current account imbalances will result (in fact have resulted) and will threaten systemic sustainability.

This describes where we are today.

Aspirin or brain surgery?

Why anyone thinks that more monetary stimulus, lower rates, more QE, helicopter money, or fiscal spending will solve these problems is beyond me. If you need brain surgery, is taking aspirin a real `solution?'

Why I'm depressed...

This is why I remain depressed about economic prospects. No, it's not about Brexit. Brexit is a symptom of this broader malaise that U.K. voters have reacted against. China is the very juvenile and very disruptive `Baby Huey' of the intentional economy who wants what it wants when it wants it and does not want to obey any rules or shoulder any responsibility. Meanwhile, countries continue to treat Baby Huey with all too much respect.

Kicks...

There is no surprise about why traditional economics has not worked. Nor is there any reason to be surprised by all the fringe political parties and figures that are rising to prominence globally. Denial is not a viable strategy. Addressing the real problems is more dangerous and is confrontational. So many prefer to stay with the (formerly) tried and true (more aspirin, please). We see that in the U.S. as Trump is considered all but `looney' by some even though he has his finger on the pulse of what is wrong. Traditional politicians want to kick the can down the road. Trump wants to kick someone in the rump.

Pressure-cooker Europe

In Europe, Germany is keeping everyone on its traditional medicine which will be painful for a very long time. It won't cure the problem or won't cure it soon enough. Political pressures already are interfering, welling up. Japan is beset by a huge debt load and a shrinking population with cultural values it wants to protect; it will continue to pay the price for its choice. There is no easy way out for Japan. For Europe, the U.K. may have given us the view of the future. Europe is being torn up from the inside by terrorist threats and a shaky banking system and from the outside by a lack of competitiveness and held together by the iron fist of German determination. Something's got to give...and it will.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.