Global| Oct 03 2016

Global| Oct 03 2016Euro Area Manufacturing PMI Shows Some Lift

Summary

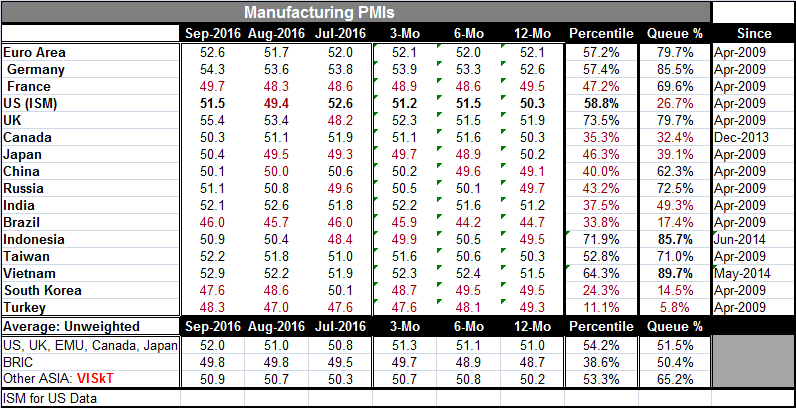

While the global manufacturing PMI data are still disappointing in September, they are for the most part better than they have been. The unweighted average of values in the table show the actual reading is above its six-month average [...]

While the global manufacturing PMI data are still disappointing in September, they are for the most part better than they have been. The unweighted average of values in the table show the actual reading is above its six-month average for four consecutive months. From April 2014 to November 2015 ( a period of 20 months), the actual reading was consistently lower than the six-month average. This relationship only started to prevaricate as of December of last year. The current four-month stretch of improvement is the first such stretch since March 2014 which concluded a run of eight months in which the current reading stood above the six-month average.

While the global manufacturing PMI data are still disappointing in September, they are for the most part better than they have been. The unweighted average of values in the table show the actual reading is above its six-month average for four consecutive months. From April 2014 to November 2015 ( a period of 20 months), the actual reading was consistently lower than the six-month average. This relationship only started to prevaricate as of December of last year. The current four-month stretch of improvement is the first such stretch since March 2014 which concluded a run of eight months in which the current reading stood above the six-month average.

Still, manufacturing PMI readings are not strong and we have yet to finalize service sector readings where there has been evidence of creeping weakness.

The Euro Area

In the euro area, manufacturing PMIs are relatively strong by recent relative standards with a near 80th percentile queue standing over the last five and one-half years of data. Germany's manufacturing sector with a PMI gauge at 54.3 has an 85th percentile standing over the past five and one-half years of monthly readings. France, at 49.7, has a 69th percentile standing. Italy, with diffusion reading at 51.0, has a 50th percentile standing. With these metrics, the EMU, Germany and even France stand in September above their respective manufacturing 12-month averages, but not by much.

More Broadly

On revised data, China posts a reading above 50 at 50.1 in September, up from 50.0 in August. Its moving average of its manufacturing PMI shows progress but very begrudging progress. Still, China has been so weak that its 50.1% manufacturing reading -which barely registers any growth at all- has a 62nd percentile standing: it has been even weaker 62% of the time over the last five and one-half years. We see contracting readings on the month from France, Brazil South Korea and Turkey. That's a relatively short list. Only Canada, India and South Korea weakened month-to-month on the manufacturing metric. The unweighted average of the readings in this table has a 57th percentile standing as they move solidly into the top one-half of all observations over the past five and one-half years. Still, the momentum is poor and very slow-moving although in the upward direction.

Beyond Simple Economics

The U.K. Prime Minister has just announced her intention to begin the U.K.'s formal Brexit filing in March 2017. Sterling is weaker on that reminder. PMI data dominated today's reports, but several other bits of news remind us of fragile global conditions. Deutsche Bank is still in the news and is reported to be pressing hard to conclude a deal with the U.S. Justice Department hoping to lessen the pressures it faces in markets. On an altogether different note, in Russia, Vladimir Putin has put a halt to a project to clean up and dispose of plutonium that Russia and the U.S. had previously agreed to. Old 'Cold War' concerns begin to resurface. The conflict in Syria is not going well for U.S.-Russian relations. To make matters worse, Russia is clearly feeling the economic pinch from the ongoing weakness in oil prices. It is no surprise that with those forces in train Russia seeks to move the U.S. out of its comfort zone as well. While geopolitics is not economics, we can see at time like this how they become reconnected. The Russian manufacturing PMI did take a step higher in September but still signals weak growth.

On balance, there is some evidence of global manufacturing PMIs rebounding. Outright contractions are less common in September and even deterioration month-to-month is less common. The pace of improvement is slow, but there is evidence of ongoing improvement. It's not a great month for economic signals, but given the way things have been, it's an improvement and a step in the right direction.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.