Global| Jan 04 2017

Global| Jan 04 2017Euro Area Manufacturing and Services PMIs Spurt as Inflation Lights Up

Summary

Note how clearly the 'blue line' leads... The way down; the way up; the mini-cycles... Be careful what you wish for... The euro area PMIs for manufacturing and services are heating up. The region no longer looks so growth-challenged, [...]

Note how clearly the 'blue line' leads...

Note how clearly the 'blue line' leads...

The way down; the way up; the mini-cycles...

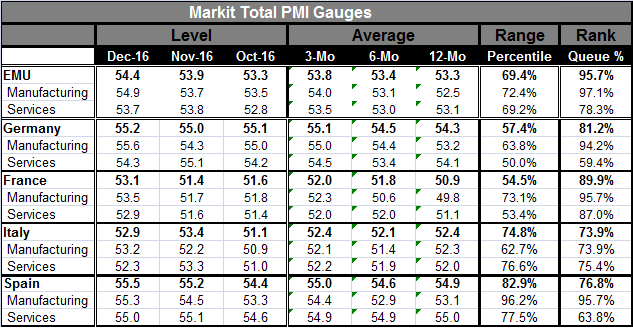

The euro area PMIs for manufacturing and services are heating up. The region no longer looks so growth-challenged, through the eye of the PMIs. Manufacturing is leading the way with percentile standings of this sector arrayed in the top ten percentile of their respective queues of data since January 2011for three of the four largest economies. Italy's standing is a respectable 73rd percentile on this measure. The services sector is bit more circumspect with an EMU-wide standing in its 78th percentile (which is firm) and on percentile standings that range from 87% (France) to 75% (Italy) to 63% (Spain) anchored by the lowest reading at 59% (Germany).

Services lag

The service sector has been slower to come around and that sector defines employment conditions for most workers since that's where most jobs are. But manufacturing is the more volatile sector and tends to be directional- it is expanding the fastest. Manufacturing has the best raw diffusion score and the best relative percentile queue standing for the EMU as well as for each of its largest economies with the exception of Italy where the queue standing for services surpasses the standing for manufacturing in December.

Solid but not unimpeachable breadth

The moving averages do not tell a story of uninterrupted building momentum. Except for services in Spain and manufacturing in Italy, the sector indices show a three-month moving average ahead of its 12-month moving average that defines some upward momentum. Manufacturing is moving up exceptionally sharply (except in Italy) and generally from a reduced position in recent months. The current month's observation (December) is ahead of the 12-month average in each big four economy sectors except Spain where services are only tied with their 12-month average in December. Comparing the current month's value to a 12-month average is a low hurdle.

Upward momentum...yes, but

The trappings of upward momentum are there for the most part, but momentum is not as impressive when we view it country by country and make comparisons using averages instead of the most recent monthly observation. Charts show an impressive upward path for the EMU as a whole, but the speed-up itself is still nascent.

Inflation: ho!

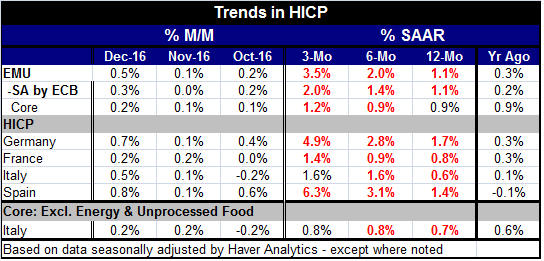

On the inflation front, we see increases in the EMU rate of 0.5% in December with big four economy results ranging from 0.2% in France to 0.8% in Spain. We can expect to hear from Jens Weidmann on these trends. For the EMU as a whole, the inflation rate is up at a 3.5% pace over three months, a lesser 2.0% pace over six months and a weaker 1.1% pace over 12 months. Inflation is not a wolf howling at the ECB's door threatening to breach the Maginot line at 2%. But the inflation pace over the shorter horizons puts policy on notice that the days of endless monetary stimulus are drawing to a close. And while PMI data are looking (much) better, other economic data are more listless in their respective recoveries. Europe still has banking sector problems to mend. Policy paradoxes are going to emerge.

The unusual becomes commonplace and uncomfortable

On a country by country basis, there is something unusual in the mix of inflation. The German inflation rate is rising faster than it is in other EMU economies. That is not surprising because Germany has had the relative strongest economy in the EMU with the lowest rate of unemployment in both relative and absolute terms. An economy this 'tight' is bound to generate more inflation than economies with the slack of France, Spain or Italy. So while Germany's situation is quite understandable in macroeconomic terms, it is also unusual for the EMU. Germany, atypically, now has the highest inflation rate among the big four economies and the EMU as a whole. Since January 1997, Germany has only had the highest year-on-year inflation rate among the big four economies and the EMU 13% of the time. And all but three of those occasions have come since July 2013 when austerity programs were put in place in the EMU, helping to drive inflation down as a remedial action in the wake of countries having run an excessive inflation pace. Germany, for a time, became a relatively high inflation country in the EMU under these conditions but with inflation running at a very low pace or with the EMU price level actually falling.

The 'new' commonplace becomes uncomfortable

In fact, since July 2013, Germany has been the high inflation country in this grouping 66% of the time. Before austerity, Germany had the lowest rate of inflation in this grouping all by 2% of the time. But conditions and circumstances change. Now prices, with austerity rules still in place, are being stoked by growth and by fast rising oil prices. Germany continues to have a higher inflation rate than the EMU and the highest rate among the big four economies. What will make this more painful for Germany will be that it will not just be the high inflation country, but it will be a 'relatively' high inflation country with its own inflation rate above that key 2% mark that separates 'good' from 'bad' ECB policy. Meanwhile, the EMU, Italy, France and Spain will run (for the most part) lower rates of inflation. The EMU rate will be below 2% not prompting the ECB into immediate tightening action despite Germany's own discomfort. Having inflation above 2% in Germany will make the Bundesbank very uncomfortable, much more so than when it had the highest inflation rate in this group with German inflation running at 0.5% while other countries experienced some degree of deflation. The worm of discomfort is turning.

Interesting times...

I expect this reality to be a difficult one for all parties involved. It will be a made more difficult by the fact the inflation is going to be driven by rising oil prices and concentrated in the oil sector, transportation and utilities rather than being a true inflation rate supported by increases in all prices. The relative price effect for oil will play out through its inelastic demand and work its way into Europe's inflation profile. It will create inflation angst in Germany while other countries will not be experiencing the warm glow of the growth that might have generated such inflation. Policy-making in Europe is about to get more interesting.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief