Global| Jul 14 2008

Global| Jul 14 2008Euro Area IP Trends Point Lower

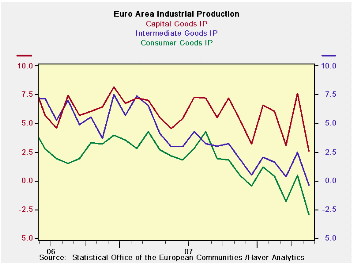

Summary

Even capital goods output trends in Europe are begging to look strained. Manufacturing IP is in its first decline since May of 2005 on a Yr/Yr basis. The month-to-month 1.4% output drop is the largest since Sept 2007. The drop is [...]

Even capital goods output trends in Europe are begging to look strained. Manufacturing IP is in its first decline since May of 2005 on a Yr/Yr basis. The month-to-month 1.4% output drop is the largest since Sept 2007. The drop is spread liberally across EMU members especially large countries including German where output is off for three-months in a row. France, Italy, Spain and the UK each have MFG output lower yr/yr; in Germany it is still up but only by 0.9%.

In the current quarter MFG IP is dropping at a 3.3% annual rate. Consumer goods output is off sharply. Intermediate goods output in falling. Capital goods output is still rising in Q2 at a thin 0.6% annual rate.

The euro currency seems to be doing some backtracking. Not only has the ‘rescue package for Fannie Mae and Freddie Mac, two large US ‘GSEs,’ (Government sponsored enterprises) helped to buoy the dollar but so has this news of encroaching weakness in Europe. Europe has been in denial about its weakness (with a few exceptions) for some time. Part of this has been due to a need to show a common front in backing the ECB. Admitting that the wheels were coming of the economy would have been no way to support the ECB in its plan to hike rates.

But with that done talk has turned quickly to how that hike could be undone. Bill Gross of PIMCO, a long term dollar bear, has changed his mind. Several high profile Wall Street strategists who had recommended US companies with large foreign sales have thrown in the towel as not only did that strategy not work it seems to have fewer prospects to work with going forward. Europe is weakening and reality is dawning slowing on a broad front with today’s report.

| Euro Area Manufacturing IP | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | May 08 |

Apr 08 |

May 08 |

Apr 08 |

May 08 |

Apr 08 |

|||

| Ezone Detail | May 08 |

Apr 08 |

Mar 08 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q-2- Date |

| MFG | -1.4% | 0.5% | -0.7% | -6.4% | -0.7% | -0.7% | 1.0% | -0.2% | 2.9% | -3.3% |

| Consumer | -1.8% | 0.7% | -0.9% | -7.6% | -2.8% | -3.3% | -1.3% | -2.9% | 0.4% | -4.4% |

| Consumer Durables | -3.3% | 1.9% | -2.0% | -12.6% | -0.5% | -3.7% | -1.2% | -5.0% | 1.0% | -- |

| Consumer Non-Durables | -1.2% | 0.0% | -0.6% | -6.9% | -3.8% | -3.2% | -1.4% | -2.5% | -0.1% | -- |

| Intermediate | -1.4% | 0.4% | -0.6% | -6.1% | 0.1% | -0.1% | 0.7% | -0.4% | 2.5% | -2.9% |

| Capital | -2.4% | 2.4% | -1.7% | -6.9% | 4.2% | 0.9% | 5.4% | 2.6% | 7.6% | 0.6% |

| Main Euro Area Countries and UK IP in MFG | ||||||||||

| Mo/Mo | May 08 |

Apr 08 |

May 08 |

Apr 08 |

May 08 |

Apr 08 |

||||

| MFG Only | May 08 |

Apr 08 |

Mar 08 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q-2- Date |

| Germany | -2.6% | -0.3% | -0.3% | -12.2% | -2.2% | -1.9% | 3.0% | 0.9% | 5.5% | -8.3% |

| France: IP excl Construction | -2.6% | 1.5% | -1.1% | -8.8% | 3.5% | -1.7% | 0.4% | -1.2% | 3.1% | -2.0% |

| Italy | -1.5% | 0.3% | -0.2% | -5.3% | 0.4% | 0.9% | 1.0% | -2.7% | -0.5% | -2.6% |

| Spain | -14.6% | 27.5% | -16.9% | -32.9% | 39.8% | -9.5% | 11.8% | -7.4% | 12.0% | 26.7% |

| UK | -0.6% | 0.1% | -0.5% | -3.8% | 0.0% | -0.8% | 0.2% | -0.8% | 0.0% | -1.8% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.