Global| Sep 14 2016

Global| Sep 14 2016Euro Area IP Falls Sharply in Step with Bond Prices...How Curious

Summary

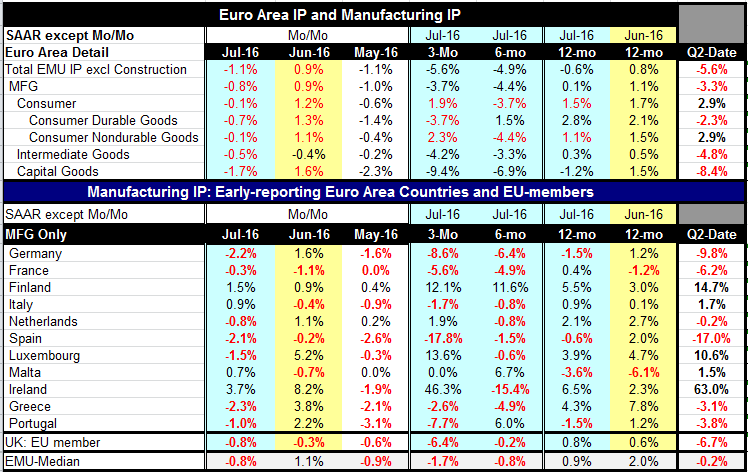

Euro Area IP has fallen relatively sharply in July. The 1.1% drop matches the 1.1% drop in May with a 0.9% gain for June sandwiched in-between. Output has been see-sawing in the Euro-Area over the last five months. Still, it is lower [...]

Euro Area IP has fallen relatively sharply in July. The 1.1% drop matches the 1.1% drop in May with a 0.9% gain for June sandwiched in-between. Output has been see-sawing in the Euro-Area over the last five months. Still, it is lower month to month in five of the last seven months and manufacturing IP is lower in seven of the last 10-months. And on trend it is weakening not just fluctuating. Oh, don't worry. BE HAPPY! There is a bond market sell off that smart market must know something. Right?

Euro Area IP has fallen relatively sharply in July. The 1.1% drop matches the 1.1% drop in May with a 0.9% gain for June sandwiched in-between. Output has been see-sawing in the Euro-Area over the last five months. Still, it is lower month to month in five of the last seven months and manufacturing IP is lower in seven of the last 10-months. And on trend it is weakening not just fluctuating. Oh, don't worry. BE HAPPY! There is a bond market sell off that smart market must know something. Right?

Bad breadth...no breadth mint

Over 12-months EMU Area IP excluding construction is falling by 0.6% with manufacturing eking out a 0.1% gain. But manufacturing output, as well as overall output, has lost momentum and sharply. Manufacturing IP was growing as fast as 3.6% year-on year in August of last year. But that faded fast to a gain of 2.6% in November, to under 2% in February and April of this year and to the 1% to 0.5% range for May and June and now to just 0.1% in July. Momentum is clearly being lost and the loss is across sectors as well as across member countries. Look at the trends across member countries.

Bonds like the cheese stand alone

Despite the peculiar bond market sell-off we see in markets, there is no basis for that in real economic trends. The notion that bonds are selling off because central banks have lost control or are ineffective suggests even weaker growth might lie ahead as well, making that argument a non sequitur. Weakness in stocks for such reasons makes more sense and has even greater validity with rising bond yields as a back drop (ignoring the fact that rising yields are unexplained or explained poorly). But the rise in bond yields is peculiar as it has no basis in economic performance because of exchange market developments of because of commodity markets activity. The bond market has come unglued from economic fundamentals of all sorts.

Events and events as signals

In Europe alone Total IP less construction trends are showing accelerating weakness from 12-months to 6-months to 3-months. Manufacturing declines are not quite accelerating on that time line but IP is still weak and weakening- just not getting progressively worse. Consumer durable goods output, intermediate goods output and capital goods output all are decelerating on that time line and all are getting progressively worse. Capital goods sector weakness is perhaps the most disturbing of these sector trends. Capital goods output is falling at a 9.4% annual rate over 3-months. It's 1.2% year-on-year drop is its weakest since August of 2014. But that drop came amid volatility with strength in IP in the adjacent months. This time around capital goods output is falling hard and it is part of an ongoing slippage. That is not good news or a good economic signal at all.

Not your typical biz-cycle and a bad sign to boot

Globally capacity use is low and in such circumstances the need for capital investment and spending would typically be reduced. But we are at an extended point (at least theoretically) of a business expansion and this is not what we are supposed to be seeing. The weakness in the capital goods sector is for the moment very troubling and it could be an advance signal of a more pronounced round of economic weakening yet to come...

Could this destabilize growth?

For the moment consumer spending is supporting growth. The consumer sector is the relative strongest in the Euro-Area, for example. In the US consumer spending has been steady and spending on autos has been strong but spending on autos may be set to glide into a weaker phase. If we run into a weaker phase of consumer spending matched by weakening in the demand for capital investment, that could become a problem for sustaining growth. An economy has to be running on some cylinders that are firing normally or better and the construction sector is just not enough to drive growth. Moreover, if interest rates are going to move up that will also weaken construction.

Perfect storm?

I am not ready to call this a perfect storm yet. But there is some highly disturbing weakening here and there is an overall loss in industrial sector momentum. We have seen the global PMI data for August and from that we can tell that this is not one-month's weakness that is going to go away. It seems to be something to worry about.

Is it time to worry again? About growth? And what about that bond market?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief