Global| Sep 12 2019

Global| Sep 12 2019Euro Area IP Falls for the Second Straight Month; IP Declines over 3 Months, 6 Months and 12 Months

Summary

EMU-area industrial output declined in July but fell by less than it did in June. Headline and manufacturing IP trends both show deteriorating trends from 12 months to six months to three months. Intermediate goods show the fastest [...]

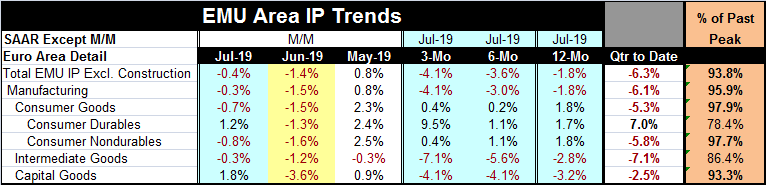

EMU-area industrial output declined in July but fell by less than it did in June. Headline and manufacturing IP trends both show deteriorating trends from 12 months to six months to three months. Intermediate goods show the fastest ongoing sequential sector deterioration. Capital goods output shows the largest decline year-over-year; it is sequentially weakening with the caveat that the three-month and six-month rates of growth both are negative but are identical. But still they are weaker than the 12-month pace. The exception is for consumer goods where output is expanding on all horizons and rising by 1.8% over 12 months. But even there, the growth rate decelerates to an annual rate increase of only 0.2% over six months and then it bucks the declining trend by 'accelerating' to a 0.4% annual rate over three months. Clearly, the consumer sector is part and parcel of the slow down. Its three-month 'acceleration' is a technical joke- the weak growth rate is the real story there. The exception here is for the subsector durable goods. There, the three-month growth rate is at a 9.5% pace. Still, the overall picture is clearly for deceleration and slowing and also for very slow growth... or worse.

EMU-area industrial output declined in July but fell by less than it did in June. Headline and manufacturing IP trends both show deteriorating trends from 12 months to six months to three months. Intermediate goods show the fastest ongoing sequential sector deterioration. Capital goods output shows the largest decline year-over-year; it is sequentially weakening with the caveat that the three-month and six-month rates of growth both are negative but are identical. But still they are weaker than the 12-month pace. The exception is for consumer goods where output is expanding on all horizons and rising by 1.8% over 12 months. But even there, the growth rate decelerates to an annual rate increase of only 0.2% over six months and then it bucks the declining trend by 'accelerating' to a 0.4% annual rate over three months. Clearly, the consumer sector is part and parcel of the slow down. Its three-month 'acceleration' is a technical joke- the weak growth rate is the real story there. The exception here is for the subsector durable goods. There, the three-month growth rate is at a 9.5% pace. Still, the overall picture is clearly for deceleration and slowing and also for very slow growth... or worse.

Early in Q3 (one month into the quarter), output is falling on a broad front across all sectors and in one of the two consumption subsectors. The pace of decline in Q3 is at a stepped up -6.3% annual rate; or at a -6.1% pace for manufacturing.

The manufacturing sector IP index as well as the survey from the Markit PMI, tell much the same story about the sector. Manufacturing peaked late in 2017 and since both indicators have been locked in a trend of erosion. Both show that manufacturing is contracting.

Consumer goods: the only sector with output higher over 12 months

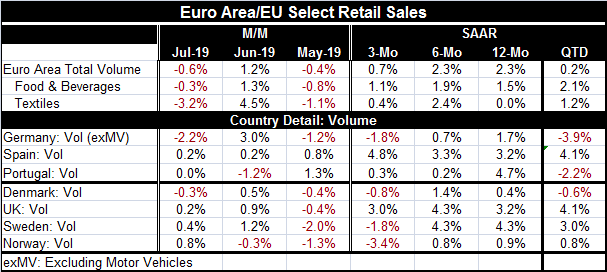

Weakness in European output is the product of two developments: one is the trade war that is slowing global growth and demand. The other, also part of the reaction to the global trade war's impact, is the weakness in retail sales in Europe. EMU retail sales volume fell in July. And while retail sales are still expanding (growing by 2.3% over 12 months and six months), sales also have slowed to a less than 1% annual rate pace over three months.

In addition European retail sales are falling over three months in Germany as well as in the (non-EMU member) Nordic countries. In the quarter-to-date, retail sales are rising at a 0.2% annual rate overall with sales volumes falling only in Germany, Portugal, and Denmark.

The weakness in industrial production at this point seems mostly derived from global weakness since domestic demand still seems to be holding up better. But European retail sales are wakening and are quite weak to start off Q3. In Germany, the IFO is now forecasting a recession to start before the end of the year.

Still, the ECB has today decided on a number of stimulus efforts. It will be doing more lending and even lowering negative rates while increasing central bank securities purchases (quantitative easing). It remains far from clear that these sorts of actions will be successful. But the ECB is pulling out all the stops, including cutting loan rates and introducing a tiered deposit rate scheme. These actions are policy moves that generally are viewed as less potent actions than conventional rate cutting under 'normal' circumstances when rates are higher. For now markets are cheered by the ECBs actions, but there is no assurance of their success. And then there is the trade war. And maybe the news on that front will get better sooner or maybe it will not. But the ECB seems to have done about all that it can do apart form one thing: doing even more.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief