Global| Jul 13 2016

Global| Jul 13 2016Euro Area IP Drops Like a Rock in May

Summary

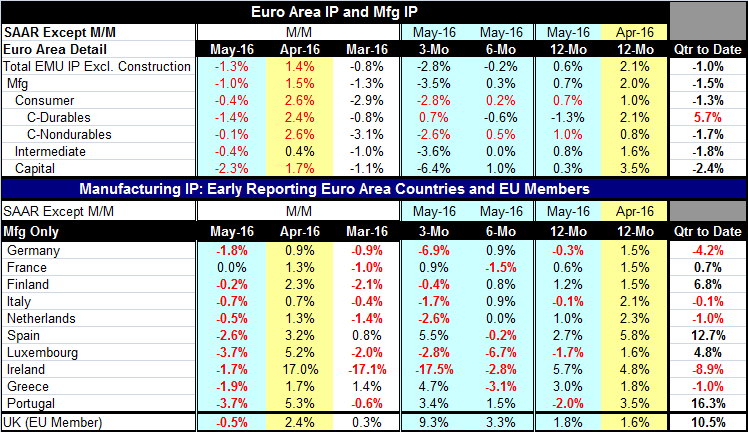

Euro area industrial output fell by 1.3% in May, giving back most of the gains from April's previously impressive 1.4% rise. However, April was preceded by a 0.8% drop so that on balance EMU area IP is lower at a 2.8% annual rate over [...]

Euro area industrial output fell by 1.3% in May, giving back most of the gains from April's previously impressive 1.4% rise. However, April was preceded by a 0.8% drop so that on balance EMU area IP is lower at a 2.8% annual rate over three months. It is lower over six months and up by just 0.6% over 12 months, showing a deteriorating growth profile on the timeline.

Euro area industrial output fell by 1.3% in May, giving back most of the gains from April's previously impressive 1.4% rise. However, April was preceded by a 0.8% drop so that on balance EMU area IP is lower at a 2.8% annual rate over three months. It is lower over six months and up by just 0.6% over 12 months, showing a deteriorating growth profile on the timeline.

IP trends are weak across sectors

IP trends are mostly deteriorating across sectors as well. Overall IP shows decay in its sequential growth rates. Consumer durable goods are an exception and capital goods are an exception in a smaller way. Only consumer durables have a stronger three-month growth rate than a year-over-year growth rate. Every single major sector has output lower in May and in March with a gain in April sandwiched in-between.

The unfolding Q2 pattern is weak

This pattern also leaves the quarter-to-date patterns weak with negative values for all sectors except for consumer durables. Two months into Q2, output is under pressure, and unless there is another sharp reversal in June, output will drop in Q2.

Ride my seesaw

Looking at trends in 10 of the `original' EMU members (we include Greece; Austria and Belgium have not yet reported), we find output lower on a country level in every single one of them except France where it is flat in May. Output is up in every single one of them in April. Output is lower in eight of 10 in March. This seesaw pattern is maddeningly consistent; it makes it likely that some sort of outside disturbance due to weather or bad seasonal factors is operating across Europe.

Longer term weakness country-by-country as well

Whatever the reason for the monthly saw-tooth, the upshot is that IP trends are not only volatile but weak. Six of 10 of these members have output falling over three months. Five of 10 (only two the same members) have output falling over six months. Four of 10 have output lower over 12 months and that group includes Europe's largest economy, Germany, its fourth largest economy, Italy, Portugal and tiny Luxembourg. Quarter-to-date output is falling in five of these countries: Germany, Italy, the Netherlands, Ireland and Greece.

Brexit is more than a toothache

Clearly this has not been the best of times for Europe to brace for the Brexit shock. But the U.K. has acted quickly and already has a new Prime Minister in place, Theresa May. Europe wants the U.K. to act as fast as possible to clarify the uncertainties that hang over the U.K. departure from the European Union, but the U.K. will undoubtedly have a lot of things to negotiate with Europe and its extraction from the EU will come at a measured pace, more like healing a bone than extracting a tooth.

Asia is weak too

Japan posted a deeper drop in its IP today at -2.6%, down from -2.3% reported earlier. And in China exports fell by 4.8%. Asia still shows weakness in its two largest economies; Europe's weakening is not in isolation. Japan's governmental forecast for GDP was cut to 0.9% for this year, down sharply from a 1.7% estimate mooted in January. Yesterday, a weaker inflation outlook was provided. The Abe Administration is expected to launch a new stimulus program of nearly $200 billion. It is expected to be announced soon.

Markets found a new drug

Today seems to be a `bad news' as `good news' day. Markets are reacting to worse-than-expected news out of China as evidence that it too will launch a new stimulus program. Optimism continues to carry the day even though government programs have not provided any solutions in the past and countries' choices are increasingly limited. Fiscal stimulus and monetary excesses have taken us down the path to where we are today. There is even dome denial of the oil market contango which finds future prices higher than spot prices and is generally regarded as a bearish market signal, especially with so much oil currently in storage already. Markets have simply found new way to cope with all the bad news, to deny it. Fiddle dee dee.

Summing up

Because of the sharp oscillations in IP, it is hard to make too much sense of the May IP report from EMU. We can see that these movements are shared across sectors and countries and so have some substance to them even if the reason is not clear. Still, it adds a bit of mystery and uncertainty to the environment at a time when there is already a lot of that in the air. Oil still seems to be in excess and yet oil prices seem to be `precariously' firm. Stocks seem to be in denial of some basic realities but also underpinned by extraordinarily lower bond yields in a market where dividend payouts put bond yields to shame. So the stock-buying machine rolls on and yet not without risk. These remain strange days: play a Doors album.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.