Global| Jan 13 2016

Global| Jan 13 2016Euro Area IP Drops for Third Time in Four Months

Summary

EMU industrial production fell sharply in November, dropping for the third time in four months. Still, the year-over-year growth rate stands above 1% but the sequential path shows that IP growth is steadily decelerating in more recent [...]

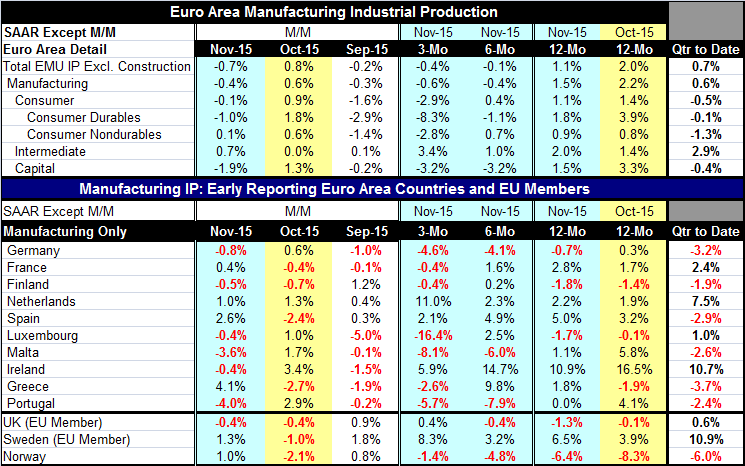

EMU industrial production fell sharply in November, dropping for the third time in four months. Still, the year-over-year growth rate stands above 1% but the sequential path shows that IP growth is steadily decelerating in more recent periods. Three-month growth is at -0.4% and six-month growth is only at -0.1%, compared to +1.1% over 12 months.

EMU industrial production fell sharply in November, dropping for the third time in four months. Still, the year-over-year growth rate stands above 1% but the sequential path shows that IP growth is steadily decelerating in more recent periods. Three-month growth is at -0.4% and six-month growth is only at -0.1%, compared to +1.1% over 12 months.

Manufacturing output is lower in two of the last three months and it also is decelerating.

Consumer goods output is falling in two of the last three months and it is decelerating. Both consumer durable goods and nondurable goods output are lower in two of the last three months and both show output trends that are decelerating. Finally, capital goods output is lower in two of the last three months and its path shows deceleration as well. Intermediate goods output shows no declines in the last three months and its trends show growth.

Sector trends in the EMU show a great deal of weakness. There has been some talk of stabilizing conditions in Europe, but the manufacturing sector clearly is not yet on board for that.

Among the ten reporting EMU members in the table, half show output declines in November. This compares to four with declines in October and seven with declines in August. Seven of these EMU members still have output falling on balance over three months. That compares to three with declines over six months and over 12 months.

Clearly, there is no evidence of output stabilization here. These data draw from November and all the volatility of the New Year have yet to wash over the sector. It is never clear how much this sort of financial turbulence will affect the real economy especially a sector like industrial production. But we know that some of the financial disruptions stem from real world events like plunging commodity and oil prices. These sorts of events will cut back on investment in those sectors and will affect the growth of output. Moreover, two months into this fourth quarter, the quarter-to-date shows output declines in six of ten of these countries. Europe not only is not out of the woods, it is still under attack by the bears.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief