Global| Apr 06 2009

Global| Apr 06 2009Euro Area Inflation Is StillDropping Fast

Summary

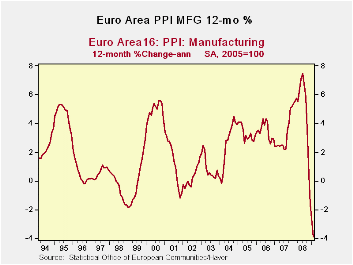

EMU inflation drops at record pace in February. EMU inflation dropped in February after a very sharp drop in January. Over three-months the annual pace of decline is at -12% compared to -11% over six-months. This is a strong pace to [...]

EMU inflation drops at record pace in February. EMU

inflation dropped in February after a very sharp drop in January. Over

three-months the annual pace of decline is at -12% compared to -11%

over six-months. This is a strong pace to stay in force over these two

periods. Over 12-months, inflation is off by 1.8% compared to being up

by 5.3% Yr/Yr one year ago. Thus average inflation over the past two

years is quite tame, under two percent.

A job well done…but. Central banks can be

content that despite all the angst, they handled the energy price spurt

well and did manage to keep inflation at bay. Still, inflation is well

under control and last week ahead of the G-20 meeting, the ECB gave the

markets a smaller rate cut than they had anticipated. Now with the

inflation numbers still showing declines the ECB is expected to be

cutting rates again.

Widespread drops, too. Inflation is falling

in Germany and in Italy at about the same pace as in EMU over the last

3 and 6 months. The UK has inflation falling fast over six months but

the pace of decline has let up over the past three-months.

| Euro Area and UK PPI Trends | ||||||

|---|---|---|---|---|---|---|

| M/M | Saar | |||||

| Euro Area | Feb-09 | Jan-09 | 3-Mo | 6-MO | Yr/Yr | Y/Y Yr Ago |

| Total ex Construction | -0.6% | -1.5% | -12.0% | -11.2% | -1.8% | 5.3% |

| Capital Goods | 0.0% | -0.2% | -0.6% | 0.6% | 1.7% | 1.6% |

| Consumer Goods | -0.2% | -0.8% | -5.0% | -3.6% | -0.5% | 4.7% |

| Intermediate & Capital Goods | -1.1% | -1.9% | -15.4% | -11.9% | -3.1% | 4.2% |

| MFG | -0.5% | -1.0% | -11.7% | -12.9% | -3.9% | 5.5% |

| Germany | -0.7% | -1.4% | -12.5% | -5.9% | 2.1% | 2.7% |

| Gy Ex Energy | -0.6% | -0.6% | -6.6% | -5.1% | -0.7% | 2.2% |

| Italy | -0.8% | -0.9% | -12.0% | -13.1% | -3.3% | 6.3% |

| UK | 0.4% | 0.7% | -5.2% | -14.7% | 2.1% | 13.1% |

by Louise Curley April 6, 2009

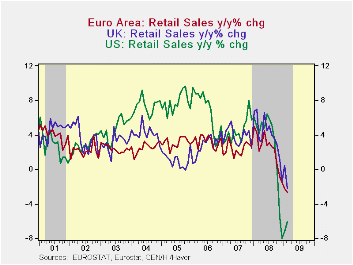

The value of retail sales excluding motor vehicles and

motorcycles in the Euro Area had risen each month since the series

began in 1995 until September of last year. (In the Euro Area, retail

sales, excluding motor vehicles and motorcycles, are reported in index

form with a base of 2005=100.) Since then, they have declined in four

of the five subsequent months. By February 2009, they were 2.7% below

February 2008

In general, retail sales tend to show increases in year to year growth reflecting the growing demands of an increasing population. Even in mild recessions, retail sales tend to increase. The growth in retail sales in the Euro Area has tended to be lower than that in either the UK or the US, as can be seen in the first chart. In the last four months retail sales in the Euro Area show much smaller declines in sales relative to the US but slightly larger declines than the UK. (The chart shows recession shading for the US.)

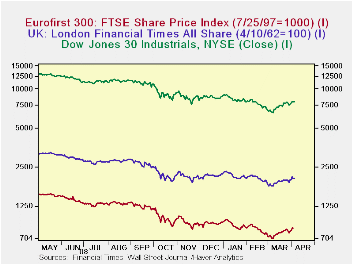

Good data for retail sales, like data on employment, production and such, take time to compile and by the time they are published, then current conditions may well have changed. Measures of consumer and business confidence help in judging current sentiment and they have recently shown some slight improvement. The stock markets also reflect economic sentiment and markets around the world have improved in the very recent past.. The second chart plots the daily price of stocks in the Euro Area, the UK and the US on a log scale.

| Retail sales ex motor vehicles and motor cycles (2005=100) | Feb 09 | Jan 09 | Dec 08 | Nov 08 | Oct 08 | Sep 08 | Feb 09/Feb 08 |

|---|---|---|---|---|---|---|---|

| EURO AREA | 105.97 | 106.38 | 106.10 | 106.59 | 107.36 | 108.70 | -2.66 |

| United Kingdom | 109.57 | 110.64 | 106.91 | 109.98 | 110.71 | 116.41 | -2.14 |

| United States | 107.72 | 106.76 | 105.12 | 108.94 | 112.42 | 116.16 | -6.04 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief