Global| Aug 12 2009

Global| Aug 12 2009Euro Area Industrial Output Steps Back In June

Summary

Euro Area industrial output rose in May but is back to its declining ways in June. The negative rates of growth are still diminishing to a decline of 4.8% over three months from -15.1% over six months and from -18% over twelve months. [...]

Euro Area industrial output rose in May but is back to its

declining ways in June. The negative rates of growth are still

diminishing to a decline of 4.8% over three months from -15.1% over six

months and from -18% over twelve months. Trend progress continues

despite the months set-back. And, with this monthly drop, the region

steps back behind the line that says it has turned the corner to

growth. It has not.

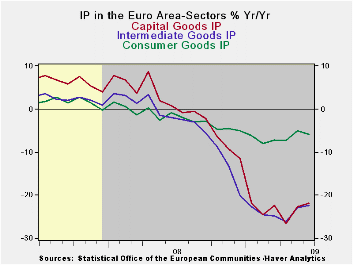

Nondurable output is actually increasing taking some of the

downward pressure of consumer goods output where durable goods trends

are still horrifically negative.

Country level trends have flattened out or show progress to

positive output In Germany, France, Spain and in the UK. Germany,

France and Spain show positive three-month output growth rates for MFG.

But over six- and twelve-months all the large countries are still

showing output declines.

Underling the erratic and slow nature of progress in EMU,

Germany’s July IFO report show some progress is still being made, but

at a snail’s pace. The IFO’s current conditions and expectations

readings edged higher, boosting the German index for business climate

in July. But the IFO’s overall and sector readings on diffusion tell us

that this progress while small is still not very widespread as

diffusion indices remain negative and made their own small progress in

the month. The biggest sector improvement in the current diffusion

index presentation was in retailing. Manufacturing made the biggest

improvement in the expectations section. But services made the turn

from a negative reading to a positive one in the expectations survey- a

significant development even if on a small two-point move.

Some of the luster from retailing’s gain in the current sector

survey is lost as the expectations for retailing made a similar but

opposite large move losing ground and blunting the current message of

improvement in the sector. .

Conditions in Germany and in EMU remain in flux. Trends are in

the right direction but some are still slow-moving. We still see

episodic signs of backtracking. It’s too soon to say it is recovery or

to be sure that we are going there, despite the strong readings from

the OECD leading indicators. Questions remain.

| E-zone MFG IP | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Jun 09 |

May 09 |

Jun 09 |

May 09 |

Jun 09 |

May 09 |

|||

| Euro Area Detail | Jun 09 |

May 09 |

Apr 09 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q-2 |

| MFG | -0.5% | 0.2% | -1.0% | -4.8% | -6.9% | -15.1% | -20.0% | -18.0% | -18.3% | -9.5% |

| Consumer | -0.3% | 0.3% | -0.1% | -0.3% | -0.5% | -4.9% | -5.5% | -5.8% | -5.1% | -3.2% |

| Consumer Durables | -4.2% | -1.8% | -0.7% | -23.7% | -11.5% | -23.8% | -21.5% | -24.4% | -19.9% | |

| Consumer Nondurables | 0.2% | 0.6% | 0.0% | 3.7% | 1.9% | -1.7% | -2.9% | -2.8% | -2.6% | |

| Intermediate Goods | -0.5% | 0.5% | -1.5% | -6.2% | -10.3% | -13.9% | -23.6% | -22.4% | -22.9% | -12.2% |

| Capital Goods | -0.3% | 1.0% | -2.9% | -8.6% | -6.9% | -22.8% | -26.5% | -21.9% | -22.7% | -12.5% |

| Main E-zone Countries and UK IP in MFG | ||||||||||

| Mo/Mo | Jun 09 |

May 09 |

Jun 09 |

May 09 |

Jun 09 |

May 09 |

||||

| MFG Only | Jun 09 |

May 09 |

Apr 09 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q:2 Date |

| Germany | 0.2% | 5.0% | -3.1% | 8.2% | 10.6% | -16.3% | -24.5% | -19.8% | -19.5% | -1.9% |

| France: IP excl Construction | 0.3% | 2.8% | -1.4% | 7.2% | -1.8% | -10.0% | -13.3% | -12.8% | -13.2% | -3.2% |

| Italy | -1.2% | -0.2% | 0.6% | -3.4% | -15.9% | -21.4% | -26.3% | -23.9% | -22.7% | -17.8% |

| Spain | 3.9% | -6.9% | 5.9% | 10.1% | -22.2% | -17.7% | -21.6% | -14.4% | -22.4% | -2.3% |

| UK: EU member | 0.5% | -0.6% | 0.0% | -0.5% | -1.8% | -6.4% | -11.2% | -11.7% | -12.8% | -0.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief