Global| Sep 29 2016

Global| Sep 29 2016Euro Area Indices Put Bad Month Behind Them

Summary

The plotted EU indices show some stabilization and pick up in the most recent data. The overall EU index bumped up to 105.6 in September from 103.8 in August. The August reading is the weakest since December 2014- quite a stretch. But [...]

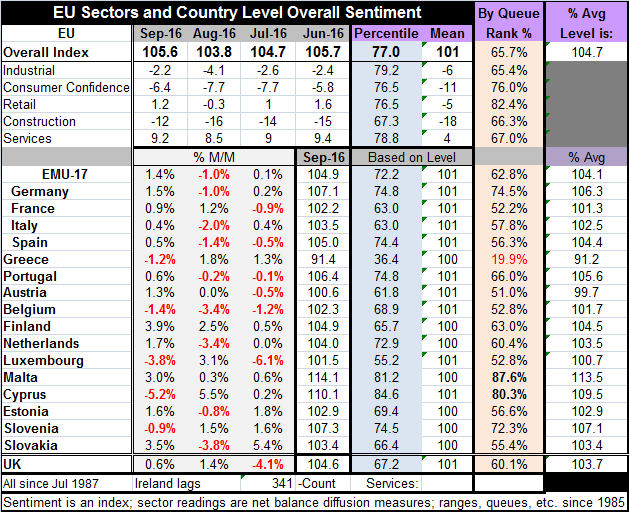

The plotted EU indices show some stabilization and pick up in the most recent data. The overall EU index bumped up to 105.6 in September from 103.8 in August. The August reading is the weakest since December 2014- quite a stretch. But the rise in September out of that crater only leaves the sentiment index as the strongest level since June.

The plotted EU indices show some stabilization and pick up in the most recent data. The overall EU index bumped up to 105.6 in September from 103.8 in August. The August reading is the weakest since December 2014- quite a stretch. But the rise in September out of that crater only leaves the sentiment index as the strongest level since June.

For the EMU indices, some of the descriptions of the monthly numbers sound more impressive than they really are. The EMU index rose to 104.9 in September from 103.5 in August. The September reading is the year's second highest (highest since January 2016). The August reading was the lowest since March 2016. And while the September reading is an eight month high, its 'bounce' is exaggerated by the weak reading in August; the index level is only marginally higher than the readings from 104.4 to 104.6 of May through July of this year. I suppose that the positive reaction to the September report is also a sigh of relief that the weak reading for August does not stand in September.

All five EU sector indices improved in September. The EU industrial index at -2.2 is at its strongest since October. Consumer confidence is at its best since May. Retailing was last stronger in June. Construction has been the impressive sector; the strongest reading since June 2008. Services are at their strongest since June. Except for construction a sector that has been making very steady - relentless - gains for some time now, we are looking at a four-month high for the sectors with the industrial measure on a more exceptional 12-month high. Despite a 12-month high for the industrial sector, that sector's readings have really been trapped in a very narrow range since October 2013. That takes some of the meaning from the observation that it is on a 12-month high. The index plot is still very flat. The Markit manufacturing gauge for the EMU is in general agreement with the EMU industrial gauge from the EU Commission as it has been flat on that same timeline without much variation.

For the EMU, only five of 17 reporting countries saw their economic sentiment gauge drop in September. This compares to eight dropping in August and six dropping in July. Ranked on their historic timeline, only Greece's sentiment gauge stands below its historic median. The EMU gauge stands at its 62nd percentile. Only tiny Malta and Cyprus have readings in their respective 80th percentiles; part of that is due to the fact that they have been reporting these indices on a shorter timeline than everyone else. Among the Big Four EMU economies, Germany with a 74th percentile standing leads the pack with Spain, France, and Italy all clustering in their respective 50th percentile.

Conditions in the EMU are decidedly modest. There is little upward momentum despite the pop of the headline index this month. One other thing to notice is that among the large countries how similar their readings are. For all of the EMU over three months, the member country's average is for two thirds of them to show a month-to-month rise. This is just slightly better than the median result since 2005. The average monthly sentiment index gain is 0.5% which is a 60th percentile standing on that same timeline. These are positive metrics but not dynamic metrics.

The EU Commission indices do help to dispel the doubt that might have accumulated since last month's very weak reading. But none of the metrics here do anything more than to keep the EMU and EU readings on their same weak sideways path. There is no sense of growth failing nor of monetary policy finally taking hold and moving things ahead faster. There is just sideways movement with a slight tendency for an uptrend. Since 2013, the sentiment ranking differences among members have been in the bottom 30% of the queue of such calculations for countries that have data going back to 1988. This is to say that the circumstances of the various members have come to be much less heterogeneous as the clustering in the large country readings also demonstrates. Still, the ECB is having hard time getting traction from monetary excess.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief